Summary

- Volaris VLRS was the best-performing airline stock in 2021, appreciating by 47% and producing a 36% EBITDAR margin through the 3rd quarter - the highest of 54 airlines reviewed.

- VLRS has emerged as the de facto winner with a 43% domestic market share, up from 30% before the pandemic. Volaris is also rapidly becoming a leading Central American airline.

- As part of the Indigo Partners consortium (Volaris, Wizz Air and Frontier), they now have a multi-year fleet plan finalized with Airbus.

- Volaris is positioned for years of top-line double-digit growth. 2021 revenue will be up more than 25% over 2019, and I forecast 2022 capacity to be up at least 25% over 2021.

- In 2022, VLRS should produce $2.7B to $2.9B of revenue and over $1B of EBITDAR. At these levels, using historical multiples, the Company could see a share price of over $40 by year end, up from the current price of $17.65.

Victor Ambriz/iStock Editorial via Getty Images

Investment Thesis

In spite of the share price increasing by 47% in 2021, Volaris (VLRS) is still significantly undervalued when compared to its peer group.

In April 2020 I began to more closely examine Volaris, which led to my first SA article published in July 2020. In January 2021, I published a subsequent SA article with my 2021 predictions. Since July 2020, the stock has appreciated 173% but is still significantly undervalued. In this article, I review Volaris' performance from 2021, discuss what has changed with the company and make new predictions for 2022.

2021 - A Year of New Records Revenue and Profitability

The forecast in my January 2021 article has proven to be quite accurate. I predicted the Company would produce $2.15B of revenue, and after the first three quarters, the Company is on track to produce to $2.1B to $2.2B for the year. This is a 25% increase over 2019 and a new record for the Company.

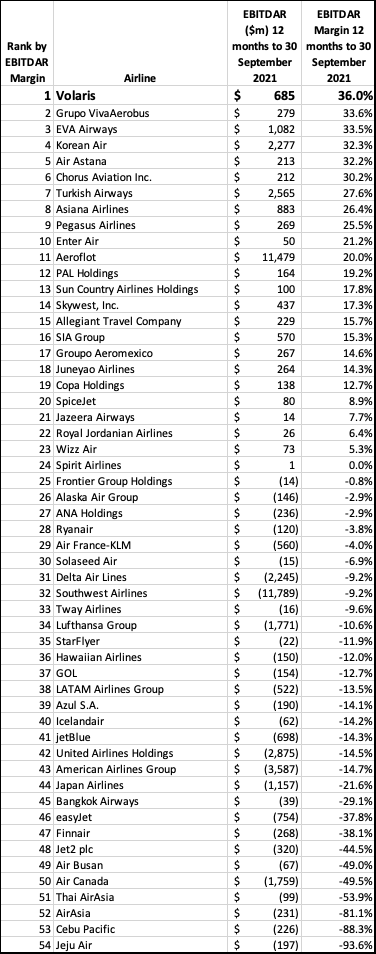

In January 2021, the range of revenue forecast by the analysts that cover the stock was $1.0B-$1.5B. At that time, I predicted the Company would produce $731M of EBITDAR or a 34% margin for 2021. An analysis produced by Airfinance Journal in December 2021 showed Volaris with a Trailing Twelve Month, "TTM" EBITDAR of $685M with a margin of 36%, the highest amongst the 54 airlines covered. It’s also worth noting that Viva finished second and Aeromexico finished in the top third, indicating Mexico has been a strong market overall. I now forecast the Company will produce $798M of EBITDAR for the full year 2021, well above my original estimate and most, if not all, analyst estimates.

Source: Airfinance Journal

A quick and important side note about EBITDA numbers when viewed on public sites that rely on third-party aggregators’ company analyses. Many of these sites have published incorrect numbers. The correct number, verified by the Company is $603M, found here at CNBC.

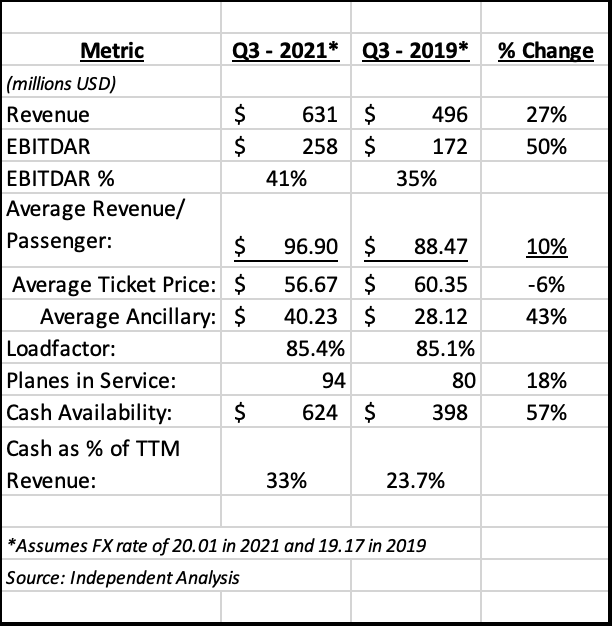

This record revenue and profitability show that a highly experienced and capable management team is pulling all the right levers to make Volaris one of the best-run airlines in the world. Below is information looking at Q3 2021 vs Q3 2019 for comparison purposes. It is also worth noting that Q3 2019 was one of the Company’s best quarters prior to the pandemic.

Note how well the Company has grown its ancillary revenue during the pandemic. The ancillary offerings have grown by 43% over the year, now account for 42% of passenger revenue, and are very profitable for the company which then helps to drive record EBITDAR margins. By keeping the average ticket price low (to stimulate traffic) and implementing more sophisticated ancillary revenue initiatives, the company has been able to increase average revenue per passenger by 10%.

The Stock Price Responds

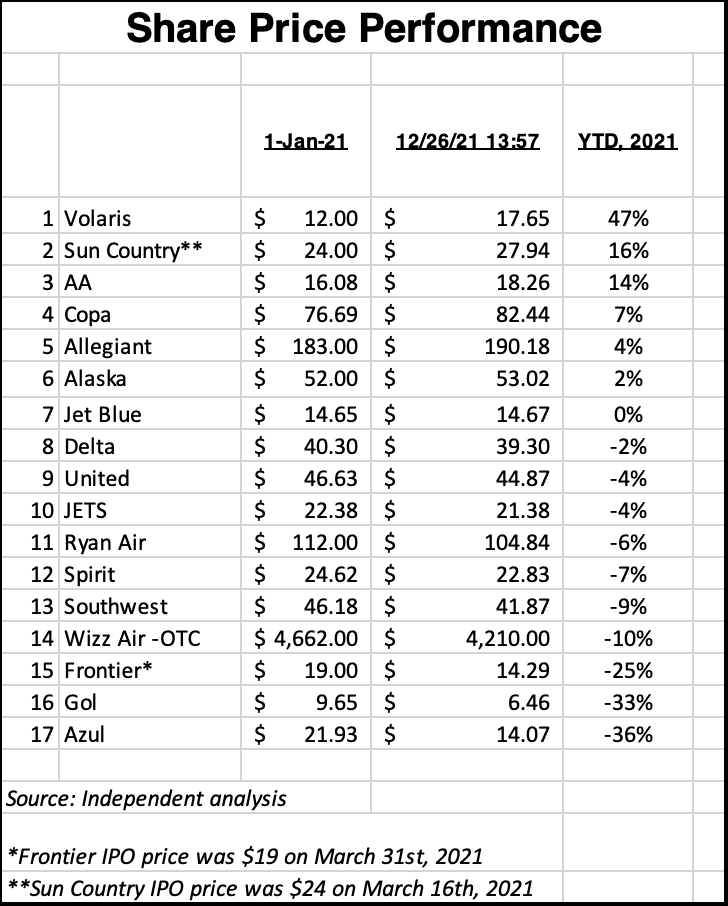

In my January 2021 article, I predicted the Company would realize a share price of $24.39. The stock reached an all-time high of $23.58 before retreating over industrywide concerns of higher oil prices and the resurgence of COVID. Of the airline stocks I track, VLRS still produced the largest gains in share price.

Oil Price Effect on Valuation

It is worth mentioning that the concern over oil prices in my opinion is overstated for several reasons. First, like many US airlines, Volaris has conducted an analysis that showed over time the cost of hedging oil exceeds any benefit that accrues to the Company. The Company will simply pass along the increase in fuel cost to the consumer as oil increases and reduce ticket prices as the price of oil falls. By my analysis, the most recent surge in oil prices would have resulted in a $5 - $7 ticket increase. Because of forward sales of tickets, it would likely take the Company about one quarter to catch up. Second, Volaris has one of the youngest and most fuel-efficient fleets in the world, so any increase will hurt competitors in a more meaningful way. In 2015, the Company produced 86 Available Seat Miles (ASMs) per gallon of fuel consumed. In 2021, the Company is on track to produce 103 ASMs per gallon consumed or an efficiency gain of 20%. This has been achieved through up-gauging and growing with more fuel-efficient planes. Fuel is the single largest cost to the airline and accounts for 32% of all operating expenses, thus making this efficiency gains meaningful. Volaris can use its fuel-efficiency advantage to either directly increase margins or to fund faster growth than is justified for its competitors.

Valuation

Although the stock price has increased nicely, it is still one of the most undervalued airline stocks that is publicly traded on the NYSE. There seems to be a consensus that using EV/EBITDAR multiples is an appropriate way to compare valuations across airlines. Currently, I follow nine analysts that produce research reports on Volaris. The current one-year forward price targets are:

- High: $31

- Mean: $28.74

- Low: $23

- Current Price as of 12/26/21: $17.65

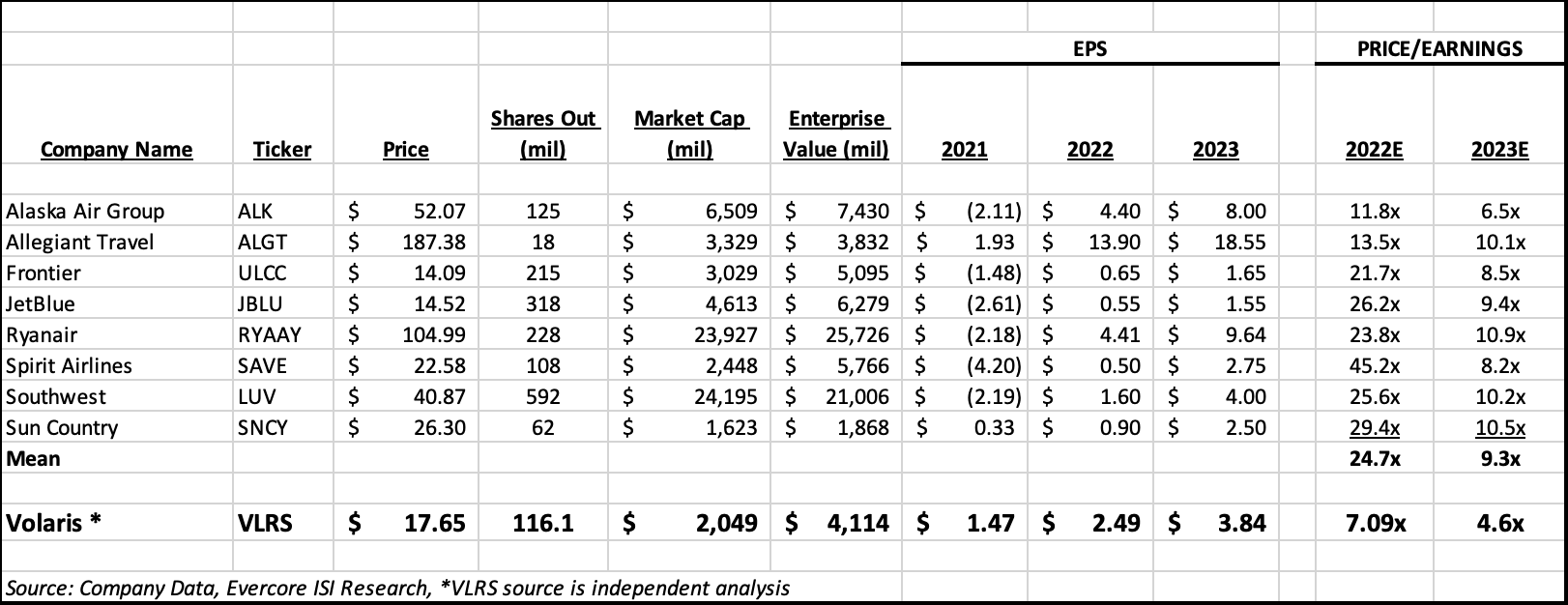

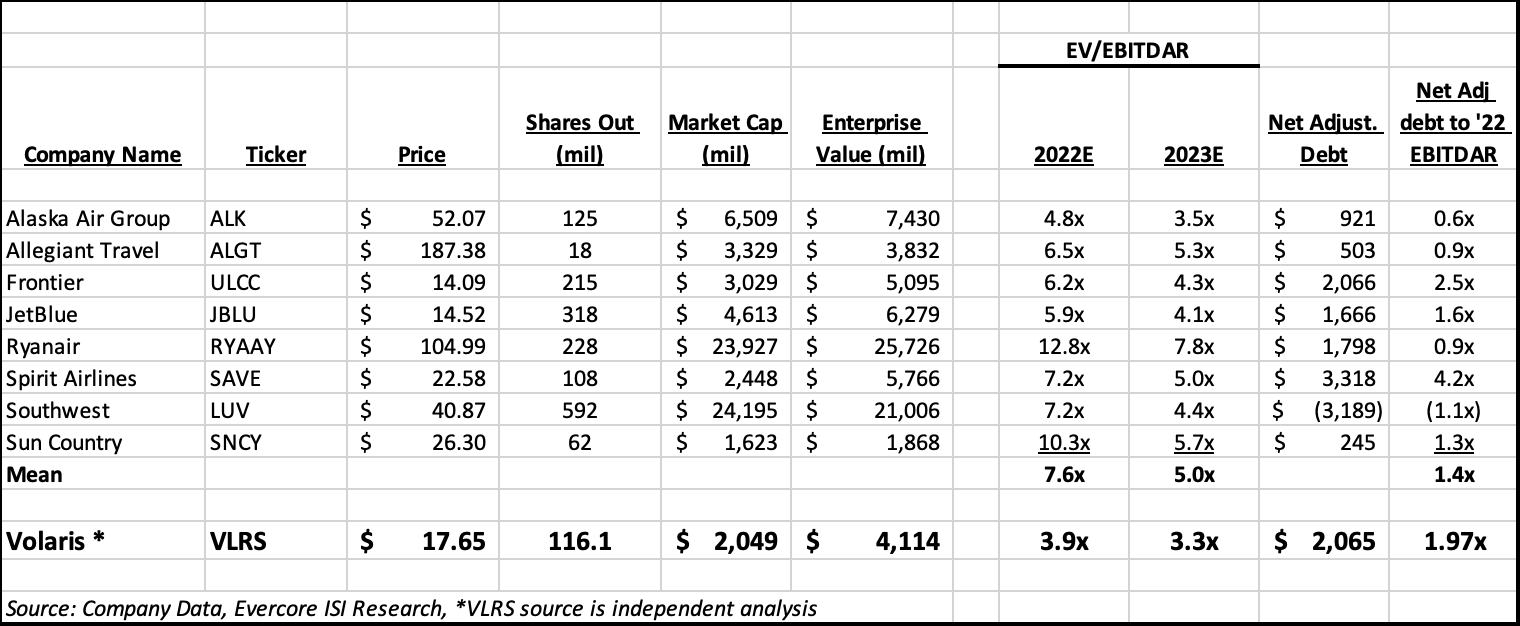

Duane Pfennigwerth of Evercore ISI, one of the more experienced airlines analysts in the industry recently initiated coverage on Sun Country Airlines. In this report, he produced a chart that included airlines I believe would be a good peer group to compare with Volaris. I have reproduced the chart into two separate tables for clarity and added to them my forecast for Volaris.

If we focus on the EV/EBITDAR multiple columns and specifically on 2023 (which is when analysts expect most US airlines to recover), these companies currently have an average multiple of 5.0x. If Volaris was rewarded with this same average multiple, the current share price of Volaris would be $36. An argument could easily be made that Volaris should receive a premium multiple given the following characteristics of the Company:

- #1 in the Domestic market with a market share of 43%.

- Over 41% of their routes have no direct airline competition.

- One of the top three lowest cost airlines in the world on a CASM basis.

- Operating in a Domestic market that prior to the pandemic was growing annually at 9% for the last five years, largely supported by the bus to airline converts. I expect this growth rate to accelerate going forward as more bus customers begin to experience and understand all the benefits of flying vs traveling by bus.

- A fully committed multi-year fleet plan that will support maintaining the lowest cost position for years to come.

- Hundreds of new routes that can be added that will support double-digit top-line growth for years as the USA returns to Category I and Central America is basically untapped.

Source: SCT, Volaris Corporate Presentation

No airline in the peer set provided above can boast this combination of merits.

So why is the valuation below its peers?

- Historically, the airline has produced inconsistent financial results. This inconsistency can be summed up in two words – “irrational competition.” As described in my earlier article, Interjet was a flawed business model, with enormous debts. Interjet apparently believed the only way to survive was to produce cash by reducing ticket prices. Volaris and other competitors responded rationally by safeguarding market share which in turn hurt financial results. In my opinion, the industry structure of Mexico has now evolved to three rational competitors and the Company going forward will produce predictable and consistent growth and earnings. More on the competition later.

- Volaris is not widely known, and as a result, does not have a broad shareholder base. Although the Company has an outstanding group of analysts that report on them, the airline still needs to develop more of an international shareholder base outside of Mexico and the USA. As the Company continues to produce solid quarterly results accompanied by a series of roadshows in the USA and Europe, more buyers of the stock will emerge. Also, producing financial reports that are in US Dollars will make it easier for investors to compare its performance to other airlines.

- The Competition and Market

For the most part, the competition has performed and responded to the pandemic as I forecasted.

Aeromexico is about to emerge from bankruptcy like most legacy airlines do, with lower costs and reduced capacity. Their cost position is still much higher than Volaris or Viva, and they focus on the business and international customer. Domestically, they will remain primarily a feeder operation to their international segments (including Delta codeshare) and serve the premium customer. With private-equity owner Apollo, I would expect Aeromexico to be a rational competitor. In January 2021, Aeromexico had a 31% domestic market share. By November this year, their domestic market share had fallen to just over 26%.

Viva has performed well during the pandemic and has grown its market share from 26% to 29% over the same period. Very importantly, they are a rational competitor, pricing reasonably and directing much of their growth away from markets where Volaris is the leading airline.

For years, Viva has attempted to become a publicly-traded Company, but for various reasons, this has not happened. With their current performance and the recent announcement that Allegiant will invest $50M, 2022 may be the year that their IPO is realized. With this in mind, I would expect them to also be a rational competitor both before and after any IPO that may happen. Currently, as a private Company, they are not subject to the same scrutiny or standards that VLRS is as a public Company. Therefore, I am always suspect of any financial information the Company releases. Similarly, analysts should also consider this before including them in their analyst reports. Although Viva plans to grow its fleet, it is hard to imagine a scenario where they are able to secure aircraft under the same attractive terms and conditions as Volaris did as part of the Indigo Partners’ 255 aircraft order in November 2021. Further, it is my understanding that the leasing market is beginning to tighten again, further putting a governor on growth, if not previously committed.

Finally, the market is recovering very well. Domestically in November, the passengers traveling had increased to 94% of where it was in November of 2019. Each month seems to see a 2-3% increase. I expect by Q1 of 2022, the Domestic market will be fully recovered. The international market by October was 97% recovered, largely driven by USA traffic. In 2019, USA/MX traffic accounted for 51% of total international traffic. In October of 2021, USA/MX traffic was 25% above pre-pandemic levels, largely driven by US airlines increasing capacity and taking advantage of the FAA downgrade on Mexico.

Top 5 Predictions for 2022 #1. Q4-2021 and Q1-2022 performance will be a catalyst for significant share-price gains in the short term.By the end of third quarter 2021, the Company had produced TTM EBITDAR of about $700M. Q4 – 2020 was a good quarter, but still was working through pandemic issues, and Q1-2021 saw another significant surge of COVID which caused the Company to swiftly reduce capacity. In Mexico, these issues appear to be behind them. I am expecting a strong Q4-2021 as the oil price has fallen, and I believe the Company has passed along a fuel-price increase during the quarter. My current estimate is that the Company will have TTM EBITDAR after Q1-2022 of over $900M, an increase of $200M above the current TTM. This performance should send the stock into the $30s.

#2. Huge growth with consistent profitability.On the third quarter earnings call, management shared that they expect to increase capacity by 25% in 2022 over 2021 and finish the year with up to 115 - 120 planes. They currently have 101 planes operating and one soon to be delivered. Based on this, I expect the Company to produce $2.8B of Revenue and $1.0B of EBITDAR in 2022. Most analysts appear to be in the range of $2.2B to $2.5B of Revenue and $750M to $850M of EBITDAR. To a certain degree, analysts are like Company management teams – they prefer to have their estimates exceeded, thus allowing more opportunities for upgrades. I certainly believe that is the case with Volaris. When I forecasted $731M of EBITDAR for 2021 in January, a top analyst that has covered Volaris for years forecasted under $500M in April of 2021.

#3. USA restores Category I rating and Volaris adds several USA routes.Capacity increases by US carriers have soared over the last several months largely because Mexico stayed open during the pandemic but also because Mexican airlines were not able to add new routes because of the FAA downgrade. From conversations with people in Mexico, there seems to be a consensus that Mexico will have its Category I status restored by mid-year, thus allowing Volaris to open new destinations in the USA, many of which have already been approved.

#4. Company Announces Initiatives to Enhance Shareholder Value.One way the Company can quickly gain wider shareholder following is to announce a program that enhances shareholder value. As the Company continues to perform, their cash balances will significantly increase year over year and clearly communicating a set of value-enhancing initiatives is important. The options for use of cash are:

- Growth.

- Paydown debt.

- Buy planes vs leasing them.

- Issue a dividend.

- Share repurchase.

Given what I know about the Company and the fact that the current share price is well below its intrinsic value, I would be in favor of a share repurchase program that reduces the share count and increases EPS. This approach of reducing share count is a tax-efficient way to increase shareholder value and allows the Company flexibility if other opportunities present themselves. This tool is widely used and practiced by many companies. Warren Buffett at Berkshire Hathaway, long viewed as the greatest investor and greatest capital allocator of our time, conducted over $24B of share repurchases in 2020 and an additional $20B through nine months of 2021.

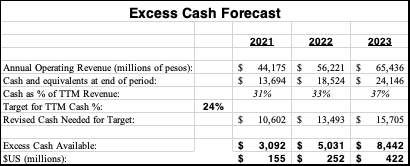

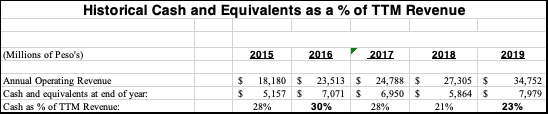

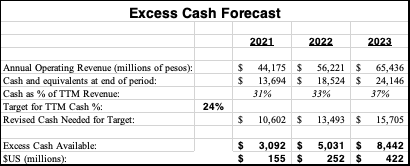

A good rule of thumb for airlines and specifically an ultra-low-cost airline like Volaris is to have 24% of TTM Revenue available in cash. As you can see below, Volaris entered the pandemic, the single biggest negative event to ever hit the airline industry, with 23%, just below what could be considered appropriate and expertly managed through the crisis with multiple liquidity initiatives.

Source: Volaris Annual Reports, Independent Analysis

The Company has successfully managed through the pandemic, so now would be a good time to begin discussions on developing a multi-year program to enhance shareholder value.

#5. Share Price hits over $40.Using an EV/EBITDAR multiple of 7.6x, the historical multiple realized by the Company, the fair value of the Company should currently be $28. Based on achieving Revenue of $2.8B in 2022 and EBITDAR of $1.0B, the share price could be over $40.

SummaryVolaris has emerged as the No. 1 airline in Mexico and produced record revenue and profits in a year where most airlines were still experiencing losses. The Company’s strong management team has built the foundation and future fleet plan that will allow them to continue to produce years of double-digit top-line growth and record profits. In 2022, Volaris should produce $2.7B to $2.9B of Revenue and over $1 Billion USD of EBITDAR, realizing a share price of over $40 by year end and propelling the Company to the next level. By 2026, I expect this airline to be producing $5B of revenue and over $1.8B of EBITDAR.

Disclosure: I/we have a beneficial long position in the shares of VLRS either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: I was a co-creator of the business plan for Volaris and co-founder of the airline in 2005. In addition to my background in aviation as a consultant and senior executive, I have been a consultant with Bain & Company and a Private Equity Investor. I currently own stock in Volaris and have since 2005. I have purchased additional shares over the last year.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.