Oppenheimer analyst Timothy Horan maintained Verizon Communications Inc VZ with an Outperform rating and a $48 price target. The stock is trading higher on Tuesday following Monday’s first-quarter print.

Horan noted Verizon continued to build on strong momentum from 2023, driven by significant network upgrades, refreshed management and improved go-to-market. Results were messy due to January price increases, which he noted impacted volumes, as did one-time expenses, which is a good setup for strong FCF growth.

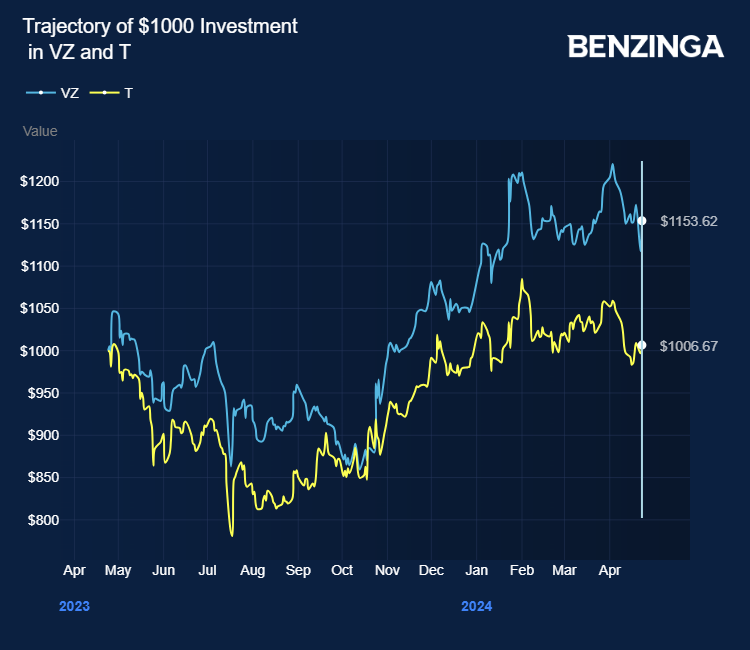

Also Read: Verizon’s Q1: Flat Revenue, Bump In Free Cash Flow And Stable 2024 Outlook

A 25bps EBITDA beat could have been larger given low upgrade volumes, but as the analyst stated, returning to subscriber growth is prioritized.

Horan said Verizon was much better positioned than two years ago, with solid momentum and trends were set to improve further.

It remains one of his best dividend plays with an attractive ~7% yield. Debt is high at $151.7 billion, but paydown is of focus and should be reduced by over $6 billion per year, as per Horan.

The analyst flagged ARPA grew 3.9%, driven by pricing action and consistent myPlan adoption, which created a recurring revenue stream of perks/services.

He said the second quarter would be the high watermark for growth, given the quarter impact of price increases, followed by tougher year-on-year comps in the second half.

Postpaid phone net adds of -68K improved vs fiscal first-quarter 2023’s -127K. He estimated as many as 50K phone additions were from second lines, but this is a limited opportunity and not a primary source of momentum. The company expects to achieve positive Consumer net adds for fiscal 2024.

The analyst said Verizon now serves over 11 million broadband customers across FWA and wireline. FWA net adds moderated to +354K, but this was not unexpected given ramping competition from AT&T Inc T and the low move environment. FiOS remains steady at +53K net adds.

Horan trimmed fiscal 2024 and 2025 revenue by 20bps each, mainly on weaker equipment revenues but a net positive for EBITDA and FCF. He reduced fiscal 2024 and 2025 EPS by $0.01 each on higher interest expense. The analyst maintained his remaining fiscal 2024 quarterly and 2025 postpaid phone net adds and FWA estimates. The fiscal 2024 FCF estimate of $19 billion is unchanged, but $1.5 billion was shifted from the first to the second half.

Verizon stock gained 8% in the past 12 months. Investors can gain exposure to the stock via Invesco Dow Jones Industrial Average Dividend ETF DJD and First Trust Morningstar Dividend Leaders Index Fund FDL.

VZ Price action: Verizon shares traded higher by 3.45% at $39.93 at the last check Tuesday.

Read Next: What’s Going On With Tesla Stock Ahead Of Earnings Tuesday?

Photo: Shutterstock

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

date | ticker | name | Price Target | Upside/Downside | Recommendation | Firm |

|---|

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.