What is it about the human race that some people feel the need to take what is not theirs? Why do some people choose to prey on the vulnerable or less experienced? Many of these individuals are intelligent but still decide to take the easy way and steal other people's hard-earned money.

It is unfortunate that wherever vast amounts of money flow, scammers maneuver in like sharks to blood. Not always, but many times the victims of scams are new to the crypto sector. They have not yet educated themselves or gained enough experience to navigate the scam-filled waters. The sad part is that many will never return to the crypto sector after being swindled.

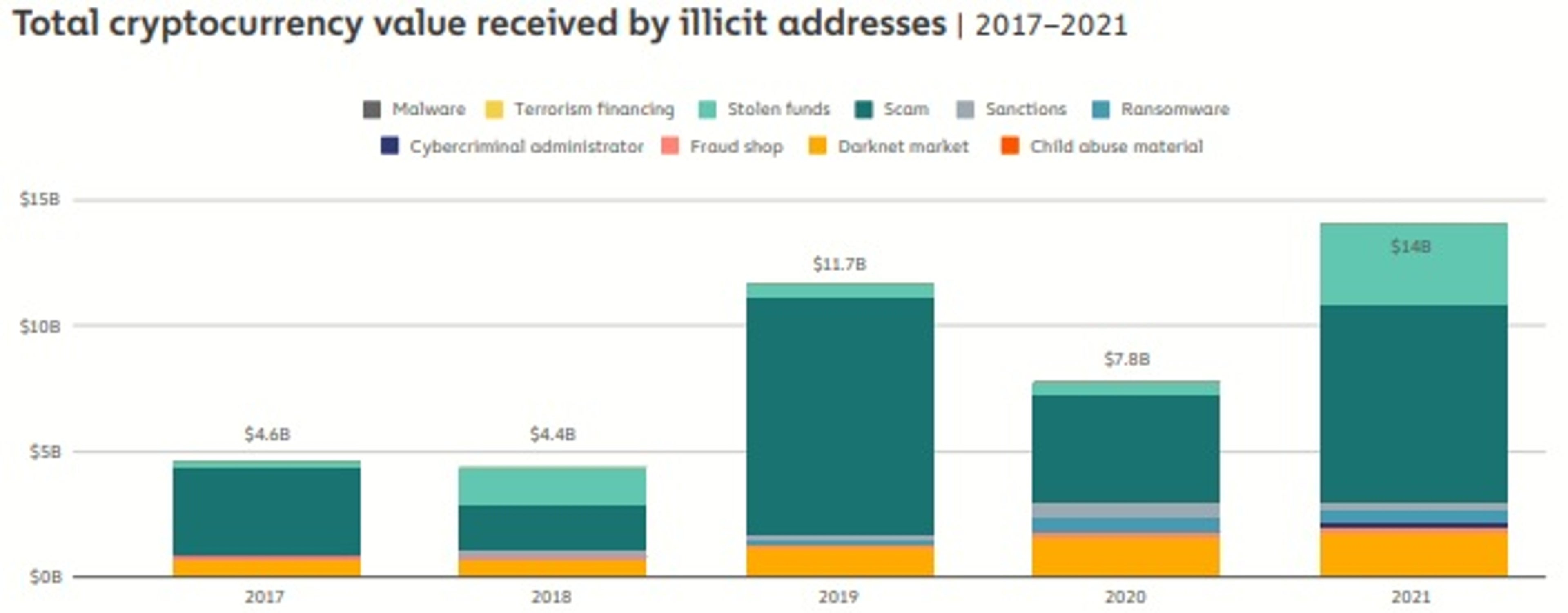

It has been just over 14 years since Bitcoin came into existence and led to the formation of the crypto sector. Tens of thousands of cryptocurrencies vie for attention, and plenty of con artists are continually present. Hopefully, as the crypto sector matures, the number of scams and hacks will decrease, but so far, it appears the opposite is true.

You have to wonder what effects the possibility of fraud will have on the sector. Will cryptocurrencies be forever relegated to the high-risk portion of investors' portfolios? Must the crypto sector be considered a second-tier investment class? Could the number of hacks and scams keep increasing until they kill the crypto sector?

The 5 Worst Crypto Hacks and Scams of All Time

Everyone is familiar with the phrase “crime doesn’t pay.” In most instances, that is probably true, but looking at some of these scams, they paid off pretty well. Hacks and scams are evil, and the victims of these crimes are innocent people who lose their hard-earned money and sometimes their life savings.

The following examples show some of the more prominent scams and hacks.

- The Mount Gox Hack

Mount Gox was a cryptocurrency exchange that operated from 2010 to 2014. The Mount Gox exchange at one time handled over 70% of all Bitcoin transactions. In early February 2014, Mount Gox was hacked for an estimated 650,000 to 850,000 Bitcoin. Shortly after the hack, Mount Gox filed for bankruptcy. Investors are still waiting to see if they will get any of their Bitcoin back.

- OneCoin Crypto Scam

OneCoin was a crypto Ponzi scheme that took in $4 billion from 2014 to 2016. A Bulgarian national, Ruja Ignatova, founded OneCoin Ltd. and OneLife Network Ltd in 2014. The main business was selling course materials covering various subjects, including trading and investing.

It all came crashing down in 2017 when founder Ignatova disappeared after a warrant was issued for her arrest. It is estimated that she made off with about $4 billion. She has never been caught and remains on the FBI’s most wanted list.

- The BitConnect Scam

The BitConnect coin BCC was released in 2016 as part of the BitConnect high-yield program. The program's central theme was a lending platform where investors would deposit Bitcoin and earn daily interest. A trading bot determined the interest payouts.

On Nov. 7, 2017, the U.K. government gave BitConnect two months to prove it was legitimate. Then on Jan. 3, 2018, the Texas State Securities Board issued a cease and desist to BitConnect. On Jan. 17, 2018, Bitconnect shut down and was estimated to have cost investors more than $2 billion.

- The AfriCrypt Rug Pull

AfriCrypt was a South African crypto investment firm founded in 2019 by two brothers. The company claimed to have an artificial intelligence trading platform to invest money. The company operated until 2021 when the brothers disappeared with Bitcoin worth an estimated $3.6 billion. According to the brothers, a hack was responsible for the lost Bitcoin.

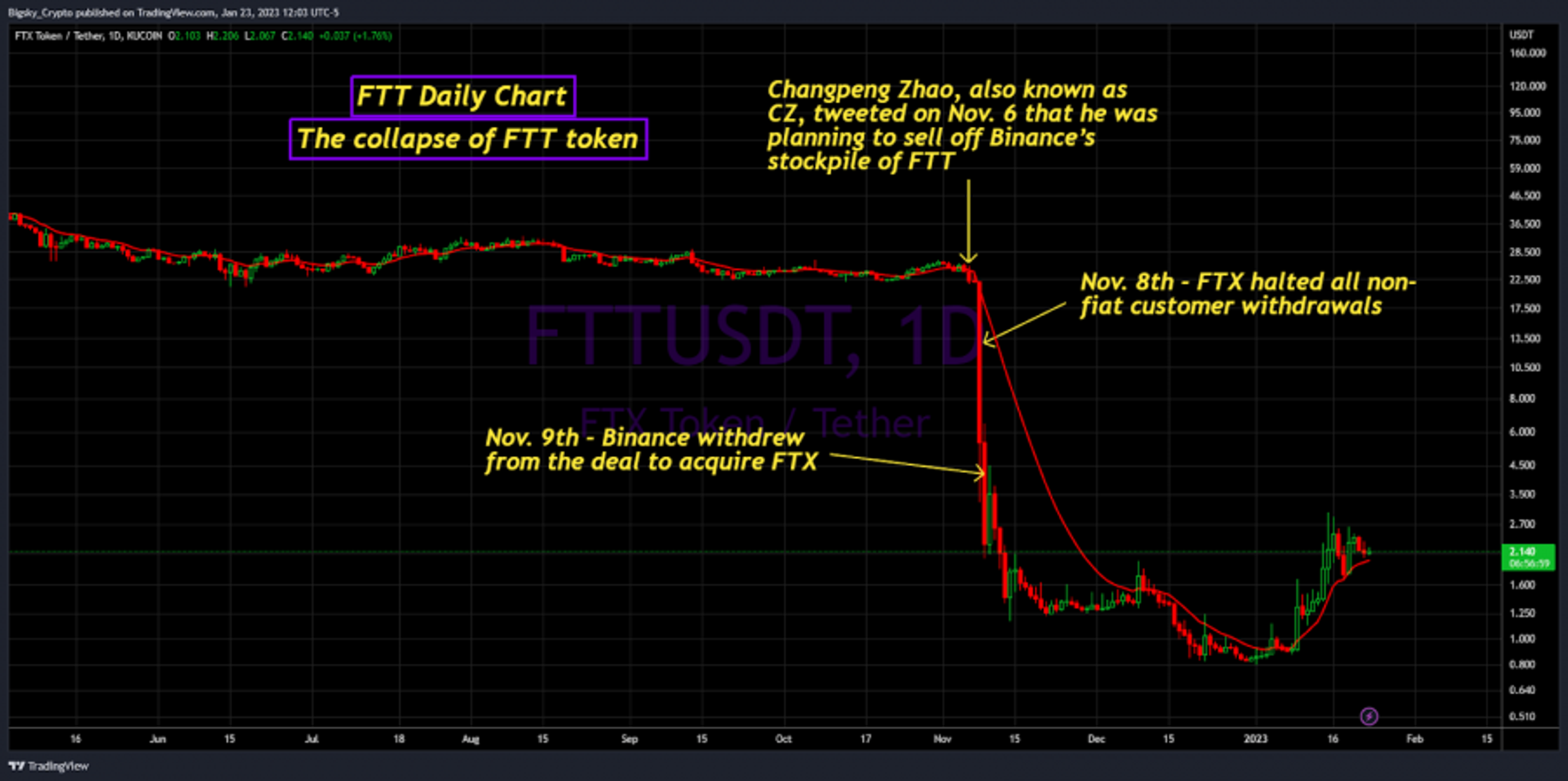

- The FTX Collapse

The FTX collapse is one of the highest-profile collapses in crypto history. Most people believed FTX was a top-tier crypto exchange. In November 2017, Sam Bankman-Fried co-founded Alameda Research, a quant trading firm. Then in May 2019, Bankman-Fried founded the FTX exchange; FTX is short for futures exchange.

FTX grew to be the third-largest crypto exchange by volume. The downfall of FTX started with an article by CoinDesk that claimed a significant portion of Alameda Research’s assets were held in FTT tokens. The FTT token is the native token of the FTX exchange. After the article was published, Changpeng Zhao, the CEO of Binance, announced that it would sell all of its FTT tokens worth $580 million.

That news led to a broader sell-off of the FTT token, resulting in a significant price drop. It also led to mass withdrawals from FTX and in response, FTX halted all withdrawals. After Binance backed out of a deal to acquire FTX, FTX filed for bankruptcy on Nov. 11, 2022.

On December 12, Bankman-Fried was arrested in the Bahamas after federal prosecutors in New York filed criminal charges. On December 13, Bankman-Fried was charged by the U.S. Securities and Exchange Commission (SEC) with defrauding over 1 million investors.

How to Spot a Crypto Scam

If you are going to invest in cryptocurrencies, you must learn how to spot crypto scams. It’s unfortunate to have to say that, but it is true. In some cases, using common sense will help you avoid them, but in other instances, it can be much more challenging to spot them. Scammers can be creative in crafting their scams, so you have to be vigilant.

Here is a list of things to help you spot a crypto scam.

- Unsolicited random messages (email or text)

- Claims guaranteeing that you will make money

- Promises that the investment has zero risk

- Offers of free cash or crypto

- Big claims with few to no details

- Grammatical errors in messages, websites or social media profiles

- Claims that you have won crypto, cash, NFTs or spots on whitelists

- Anyone who wants to supply you with a wallet

- Tokens or NFTs appear in your wallet that you have no idea where they came from

- Mining pool scams where you have to pay a subscription or use their wallet

Rug pulls or exit scams: Before investing in a project, thoroughly research the project, including the team behind it. Look for a well-written whitepaper and a team with social media links such as LinkedIn where you can see their employment history. Look into their social media engagement; how active are they? Anything you can find that allows you to dig deeper into the team or project is a plus.

How Can You Protect Your Crypto Assets?

Here is a list of ways that you can protect your crypto assets.

- Don’t store crypto assets on exchanges.

- When possible, use a cold storage hardware wallet like a Ledger or Trezor.

- Use strong passwords and change them often.

- Write out your passwords and recovery phrases, make duplicate copies and store a copy off-site.

- Self-custody is essential; not your keys = not your crypto.

- Use a dedicated laptop for software and browser extension wallets. Only connect it to the internet when interacting with one of your wallets.

- Only use a secure internet connection and a VPN.

- Spread your assets across multiple wallets.

- If you are using a mobile wallet, contact your mobile service provider to see if it offers Port Freeze or Number Lock to protect your mobile number from unauthorized transfer.

- Always use two-factor authentication, avoid SMS authentication and use Google Authenticator or Authy.

- Best For:ERC-20 tokensVIEW PROS & CONS:securely through Ledger Hardware Wallet's website

Do Scams and Hacks Pose a Threat to The Crypto Sector?

Trust is crucial in a system where financial transactions and payments occur. On the other hand, trustlessness is the cornerstone of blockchain technology, crypto payments and smart contracts. Trustless means there is no need for a trusted third party or intermediary.

Although blockchain technology enables peer-to-peer trustless transactions, the general public's confidence in the crypto sector is essential for mainstream adoption. That trust is eroded a little with every report of a hack and scam that costs innocent investors their hard-earned money.

If too many people are burned while interacting with cryptocurrencies, it could permanently damage the public’s perception of the whole crypto sector. There is no doubt that this is already happening, but if it gets too bad, it could take many years to change public opinion.

Unfortunately, as cryptocurrencies become more popular, the number of scams is also increasing. Because this could be an existential threat to all crypto, the crypto community as a whole needs to step up and help fight these scammers.

As bad as the problem is now, it will probably take a mix of solutions to get things under control. This could mean more regulations are needed and the crypto community should work directly with regulators to find a solution.

It would be refreshing to see the crypto community come together with a common goal of ridding the space of scammers. Instead, we now see in-fighting between projects or Bitcoin maximalists and everyone else.

Although it has been 14 years since Bitcoin was launched, the crypto sector is still in its infancy. As such, now is the time to step up and confront this before scams become so ingrained in the crypto sector that they will be impossible to eliminate.

About Donald Hancock

Donald’s expertise lies in the technical analysis of both stocks and crypto.