Current consists of a mobile-only financial technology app that offers banking services via its account options. This non-bank offers hybrid accounts that have components of both savings with interest and checking accounts, and it offers an attractive alternative to traditional brick-and-mortar banking institutions.

- Up to 4.00% APY return on savings of up to $6,000

- No minimum deposit

- No monthly fee

- Savings Pods for individual savings goals

- Large network of U.S. ATMs

- Account access only available on mobile devices

Current Boost Ratings at a Glance

Savings With Interest With Current Boost

In January 2022, Current launched Current Boost, which is a high-yield savings bonus that lets anyone with a Current personal account earn up to a 4.00% bonus on funds up to a total of $6,000 annually.

Furthermore, all Current accounts are FDIC insured up to $250,000 through its partner banks. Current’s payment service also works with Apple Pay and Google Pay for faster and more convenient purchases.

With Current Boost, members now have easy access to an opportunity to grow their savings during a time of record inflation rates in the United States. Current Boost is available to all personal account members on Current through Savings Pods, which are one of the most highly-engaged features on the platform.

Members can seamlessly move money from their spending balance to their Savings Pods by enabling the feature in the Current App. With Current Boost, you incur no minimum deposit requirement to open an account, as well as no hidden fees2, no minimum balance, no restrictions on moving money and no spending requirement.

Over the past year, Current member balances in Savings Pods have more than doubled, with the largest spikes following periods of cash infusions such as stimulus payments and tax refunds. The launch of Current Boost helps members grow those funds as part of Current’s mission to enable everyone to improve their financial lives.

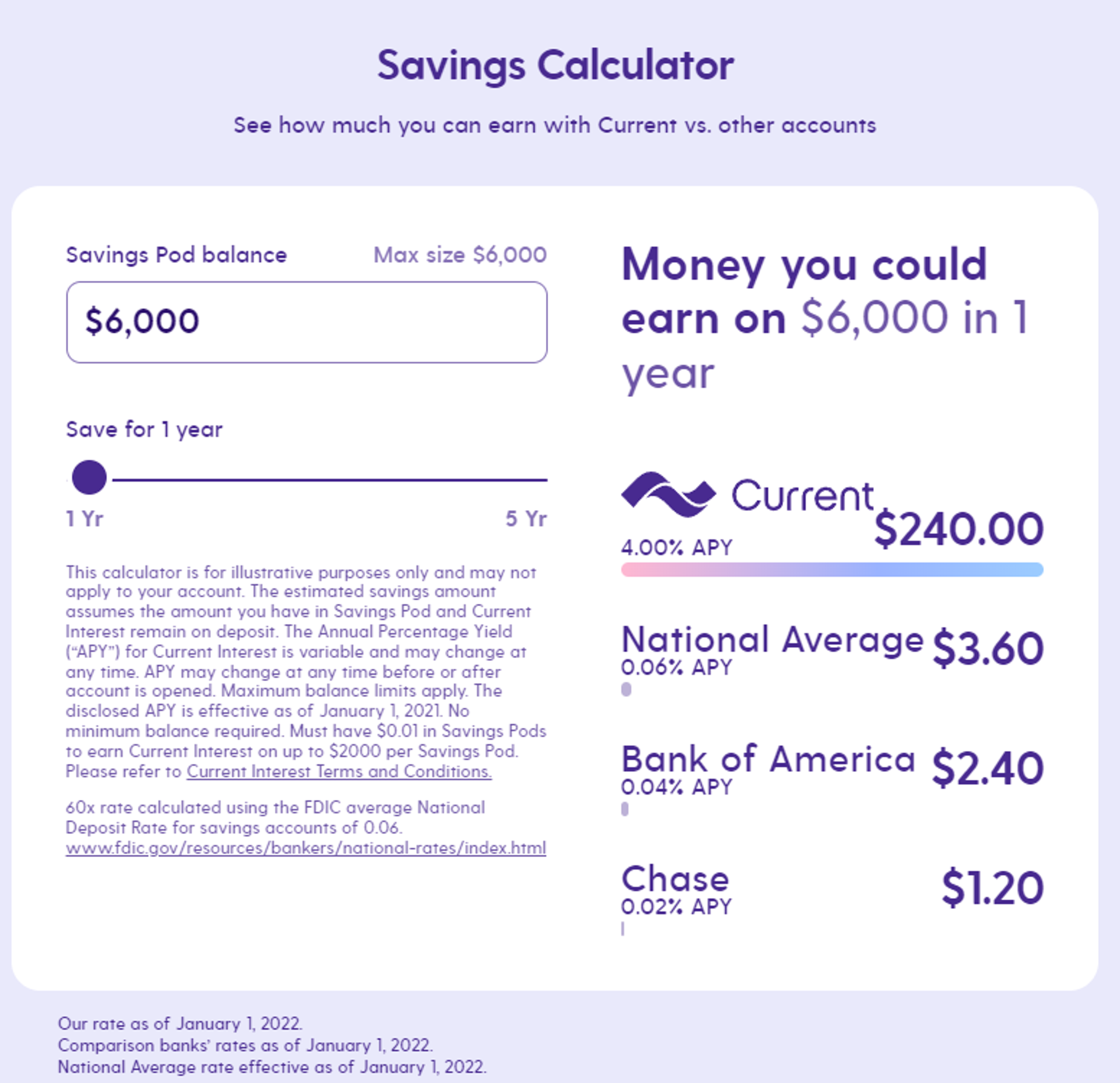

See how much you can be saving using Current’s free Savings Calculator here. Enrolled Current Boost members earn a bonus on their funds compounded daily. Check out Benzinga’s article on compound interest to read more about how this benefit can increase your interest income.

Given the substantial interest rate earning benefits of having an FDIC-insured Current Interest account, Benzinga gives this service its highest rating of 5 stars.

Current offers excellent and responsive customer service support for members via live chat, website form submission and email to support@current.com. This service is available 24 hours a day, 7 days a week, 365 days a year, so you should always be able to reach a customer service representative to help with any issues. No phone support is presently available, which reduces Current’s customer service rating somewhat.

Current’s Basic and Teen accounts have no membership fees.

The affordable customer pricing for Current’s services, the lack of hidden fees and the high interest rate clients can earn on Current Interest accounts seem especially notable, so Current gets a top 5-star rating with respect to its pricing.

Current is presently only available through its mobile app. The app can be freely downloaded for both iOS and Android devices, and it has been highly rated by users with 4.7 and 4.6 ratings at the Apple App Store and Google Play respectively.

Image of Current’s mobile app. Source: Google Play.

The mobile app has a sleek appearance and has a number of privacy controls including a Face ID and fingerprint lock. The app keeps you fully up to date on all activity in your account with features that include:

- Notifications every time your card is swiped

- Paycheck early arrival notification

- Gas holds removed instantly with Current Premium

- ATM locator for in-network machines without ATM fees2

- Locations near you for adding cash to your account

- Access to the company’s peer-to-peer payment platform called Current Pay

- Access to Apple Pay or Google Pay

- Mobile check deposits

- Privacy settings

- Spending notifications

Through the mobile app, parents can also access settings to their children’s Teen accounts that include automating allowance payments, setting chores and pausing debit cards issued on the Teen accounts. Basically, Current’s excellent mobile app provides many useful banking features and definitely deserves its top rating of 5 stars.

In addition to the unusually high APY up to 4.00%1 on up to $6,000 and other benefits mentioned above for most users, Current also offers accounts for those under 18. This feature allows teens to learn financial responsibility and independence with their own account and debit card while also providing parents the convenience to transfer money instantly, have full visibility into spending and balances as well as offer cashless convenience and security.

Current members can automatically save money into different Savings Pods using scheduled deposits. They can also use round-ups every time they swipe to automatically allocate funds for specific purchases. This money then is no longer available in their spending balance, but it can be instantly unlocked when it is ready for use.

The Teen accounts offer just one Savings Pod. With the Premium account, you also get up to $2003 in overdraft protection without any overdraft fees up to a variable limit when you enable Overdrive, as well as faster direct deposits4, getting gas holds instantly removed and up to 15 times more points5 for Current’s cashback program with participating retailers.

Additional useful Current member benefits include the ability to:

- Withdraw cash from their accounts without any ATM fees at over 40,000 Allpoint ATMs in the U.S.2

- Add cash instantly into their Current account at over 60,000 participating stores.

- Deposit physical checks into their Current account using their phone’s camera.

- Get tools to help manage their expenses, including options to create individual monthly budgets for specific spending categories.

- Gain insights into their spending habits, including how much money they have spent in a month versus how much they have earned.

- Instantly send or request money via Current Pay to other members on Current without any transfer fees using their personalized Current tags.2

Overall, the user benefits at Current deserve a high rating of 4.5 stars.

Current’s mobile app has an intuitive, easy-to-navigate interface, although a companion desktop app would be useful for those who prefer to use that method to access their accounts.

With the recent addition of a 4.00% APY return on up to $6,000, this app could be a great alternative to other banking apps that pay a fraction of the interest. The Savings Pods feature gives users an excellent way to save money for particular products or services and is one of the best features offered by the app.

In addition, having more than 40,000 ATMs and 60,000 participating stores to add and withdraw money gives you easy access to your account while letting you earn a great APY return on up to $6,000 of your money.

Letting you deposit checks via your mobile phone camera and up to a 2-day advance on paychecks4 also makes the app perfect for people working in conventional jobs. In addition, Current’s Teen accounts give parents and their teenage children a framework for managing their interrelated finances. The app has many appealing features to justify its 4.5-star user experience rating.

Current Boost vs Competitors

Benzinga has compiled the chart below showing how Current compares to other companies in its sector:

- Best For:Parents with teenage childrenVIEW PROS & CONS:securely through Current Boost's website

Mobile banking continues expanding with more banks and companies jumping on the bandwagon each year. Current’s excellent mobile app combined with the temptation of offering a 4.00% APY return on up to $6,000 basically puts the company in a higher league that can solidly compete with other banks and mobile apps providing similar services.

Savings calculator on Current’s website showing your APY return at Current versus other competing banks like Bank of America and Chase. Source: Current.

You can also get your tax refund up to 5 days faster when you sign up for direct deposit to your Current account4. Current has teamed up with TurboTax to offer discounted rates, and members can save an additional $20 when signing up for TurboTax through the Current app, although this is a limited-time offer.

Another special offer for new Current members that distinguishes it from its competitors lets you get a $50 bonus if you sign up for a Premium subscription using the advertised campaign link here, enter the code WELCOME50 and add a qualifying payroll direct deposit of $200 or more within 45 days. Check the terms and conditions to see this might apply to you.

Current has earned its place as a leading U.S.-based digital financial platform that aims to serve the needs of its members working to create better future financial outcomes for themselves. The company excels by leveraging the best in modern technology to deliver inspirational and motivational financial products in a world of increasing digitization and complexity.

Overall, Current has been given one of the highest ratings Benzinga offers. The app ranks highly in all categories and received the 4.5-star rating on User Benefits from its lack of a desktop version and inability for a user to link to their brokerage accounts.

Current Boost Tutorial

Check out Current’s YouTube channel for a tutorial on how to use its mobile app and other useful information about this digital financial platform.

Frequently Asked Questions

Is Current a legit bank?

While Current is a legitimate financial technology company, it is not a bank. The digital financial platform offers high-interest savings accounts, Visa debit cards and banking services provided by FDIC member Choice Financial Group to its U.S.-based members.

How does Current savings app make money?

Current primarily makes its money through its Premium account subscription charges. Current may also receive money from FDIC Member Choice Financial Group that provides banking services and issues Visa debit cards to its clients.

Does Current offer a savings account?

Current does offer a type of savings account. Those who sign up will receive an account along with three virtual savings pods. Each of the pods earns 4% APY and you can keep $2,000 in each one.

Current is a financial technology company, not a bank. Banking services provided by and Visa® Debit Card issued by Choice Financial Group, Member FDIC, pursuant to a license from Visa U.S.A. Inc and can be used everywhere Visa debit cards are accepted.

1The Annual Percentage Yield ("APY") for Current Interest is variable and may change at any time. The disclosed APY is effective as of January 1, 2022. No minimum balance is required. Must have $0.01 in savings pods to earn Current Interest on up to $2000 in deposits per Savings Pod up to $6000 total. Please refer to Current Interest Terms and Conditions

2Out of network cash withdrawal fees apply. Third-party, adding cash and Current membership fees may apply.

3Please refer to Overdrive™ Features Terms and Conditions. Current Premium Accounts Only

4Faster access to funds is based on a comparison of traditional banking policies and deposit of

paper checks from employers and government agencies versus deposits made electronically. Direct deposit and earlier availability of funds are subject to the timing of the payer's submission of deposits. Current Premium accounts only.

5Earning rates over 1x are only available on Current Premium accounts. Teen accounts do not earn points

Submit Your One Minute Opinion

About Jay and Julie Hawk

About Julie:

Julie Hawk earned her honors undergraduate degree from the University of Michigan before pursuing post-graduate scientific research at Cambridge University. She then started work in the private sector as a business systems analyst for a major investment bank, where she qualified as a Series 7 Registered Representative and received comprehensive training in various financial products. Further honing her skills, she attended the prestigious O’Connell and Piper options training course in Chicago, mastering professional option risk management techniques.

Julie then transitioned into the role of a professional Interbank forex trader, currency derivative risk manager and technical analyst, ascending to the position of vice president over a 12-year career in the financial markets. Julie’s illustrious banking career spanned working for major international banks in New York City, London, and San Francisco, where she served as an Interbank dealer, technical analyst, derivative specialist and risk manager. Her responsibilities included educating, devising customized foreign exchange hedging and risk-taking strategies, and overseeing large-scale transactions for esteemed banking clients, including corporations, fund managers and high-net-worth individuals. As part of her responsibilities, Julie managed substantial portfolios of forex options, spot, and futures positions as a currency options risk manager, earning recognition for executing innovative and highly profitable forex derivative transactions. Julie also spearheaded educational conferences on currency derivatives.

During her banking career, Julie attained world-class expertise in technical analysis, including Elliott Wave Theory, and pioneered research into automated trading and trading signal systems. An active member of the San Francisco Writers’ Guild, Julie also authored trade strategies, educational material, market commentary, newsletters, reports, articles, and press releases. She became a sought-after market expert who was frequently interviewed by financial magazines and news wires such as REUTERS.

Following her retirement from the banking sector, she dedicated 15 years to online forex trading, mentoring and freelance writing for TheFXperts, which she co-founded with her husband Jay. Julie is the co-author of “Forex Trading: A Beginner’s Guide” and “Technical Analysis for Financial Markets Traders,” in addition to five other books on financial markets trading and personal finance. She now focuses on writing articles on financial markets for platforms like Benzinga, although she continues to trade forex online and mentor fellow traders as part of TheFXperts’ financial team.

About Jay:

Jay Hawk grew up in Chicago and Mexico City where he became bilingual in English and Spanish. After taking formal training as a classical guitarist at prestigious music conservatories in Europe, Jay then embarked on a remarkable journey into the financial markets, cultivating his notable expertise through hands-on experience that began on the Midwest Stock Exchange.

His financial career progressed as he started actively participating in various exchange floor trading activities in the Chicago futures and options pits, where he worked his way up the ladder, serving as a clerk, trader, broker, investor and fund manager. Jay then ran a retail stock brokerage desk and managed funds for large institutional investors, leveraging his discretionary trading skills to yield profitable results for clients.

This ultimately led to Jay holding exchange seats and operating as a market maker on options exchanges in Chicago and San Francisco, initially on the Chicago Board Options Exchange. Jay also played a significant role in the Chicago Mercantile Exchange’s evolution, where he contributed to launching and actively trading the first listed currency futures options. After transitioning to the West Coast, Jay then held a seat and ventured into trading stock options and their underlying stocks on the Pacific Options Exchange.

Jay’s comprehensive understanding of fundamental economic and corporate analysis continues to inform his trading and investment activities and has led to his subsequent success as an expert financial writer. Together with his wife Julie, he co-authored “Stock Trading: A Beginner’s Guide”, “Commodity Trading: A Beginner’s Guide” and “Fundamental Analysis for Financial Markets Traders,” among their published books focusing on financial markets trading, market analysis, and personal finance.

As an integral member of TheFXperts’ team, Jay now excels in trading forex online for his personal account, mentoring aspiring traders and writing for financial platforms like Benzinga where he specializes in covering topics related to the stock and commodity markets, as well as investing, trading and reviewing online brokers.