Looking for the best rate and coverage for life insurance? Consider Sproutt.

Quick Look: The Best Flood Insurance

- Allstate: Best Overall for Flood Insurance

- TypTap: Cheapest for Flood Insurance

- Private Market Flood: Best for Claims

According to FEMA data, just an inch of water inside an average home can cause nearly $27,000 in damage. Your home insurance policy can protect your home against several types of water damage but the damage caused by flooding is excluded on a standard policy. A flood insurance policy can fill the coverage gap and help protect your home.

The Best Flood Insurance Companies

The vast majority of flood insurance policies for homes are written through the NFIP or through its WYO program, which may have your insurer’s name on the policy but which provides coverage through FEMA. Remember, your insurance agent can help you understand which flood zone you’re in, but they can’t fully assess your flood risk. It’s better to speak to carriers and comparison shop.

Until recently, it was more challenging to switch insurance companies before your policy term ended. New rules from FEMA make it possible for homeowners to choose a private market insurer and to receive a refund of unused premiums from FEMA. Remember, there’s usually a 30-day waiting period for natural disaster insurance. High-risk flood areas, of course, will cost more, but carriers offer a range of major disaster insurance that will cover flood events, personal property, mortgage loans, etc.

Even with these new changes in place, finding another flood insurance provider may be challenging in some areas. The previous structure of NFIP policies prevented changing providers easily, leading to fewer private market providers. Expect the number of private market flood insurance providers to grow over time.

Remember, too, that you may not live on a flood plain, and there are several types of flood insurance you can use to protect yourself when there’s a very low level of risk.

1. Allstate

In the short term, as the private flood insurance market builds, many homeowners may still be best served by seeking coverage through their home insurance provider or through a WYO provider. Allstate is a write your own (WYO) provider and can issue flood insurance coverage of up to $250,000 for home and $100,000 for contents coverage.

While there are about 80 WYO providers to choose from, Allstate invests in training agents and producers in the art of writing a flood insurance policy properly. As one of the largest insurers in the country and one that provides coverage in all 50 states, there's a good chance you'll find a knowledgeable Allstate agent near your home. Agents in some areas may also be able to offer excess insurance, which raises your available coverage limits if you already have an NFIP policy in place.

Read Benzinga's full Allstate Home Insurance Review

2. TypTap

A fast-growing private market flood insurance provider, TypTap is expanding its market beyond its Florida roots.

Flood coverage policies in the Sunshine State are underwritten by TypTap Insurance, but TypTap now also offers coverage in Arkansas, California, Maryland, New Jersey, Ohio, Pennsylvania, South Carolina and Texas backed by Homeowners Choice Property & Casualty Insurance Company, Inc. TypTap continues to expand to new areas.

We priced at a quote with TypTap in a low-risk flood zone with the maximum coverages available through a FEMA policy. The quote was about 30% lower than the average NFIP premium and higher coverage amounts were also available.

3. Private Market Flood (AIG’s Lexington Insurance)

Now operating in 34 states, Private Market Flood offers an easy alternative to FEMA flood coverage, with coverage options that parallel those of an NFIP policy often priced more affordably and with underwriting that does not require an elevation certificate.

We priced out coverage for a low-risk property to match FEMA’s maximum coverage limits and were pleased with our quote which was lower than both FEMA’s average cost and slightly lower than the quote from TypTap.

However, there is no option to raise the coverage limit above the maximum limits provided by FEMA. Think of Private Market Flood as a drop-in replacement for an NFIP policy which will probably save you money and is widely accepted by lenders.

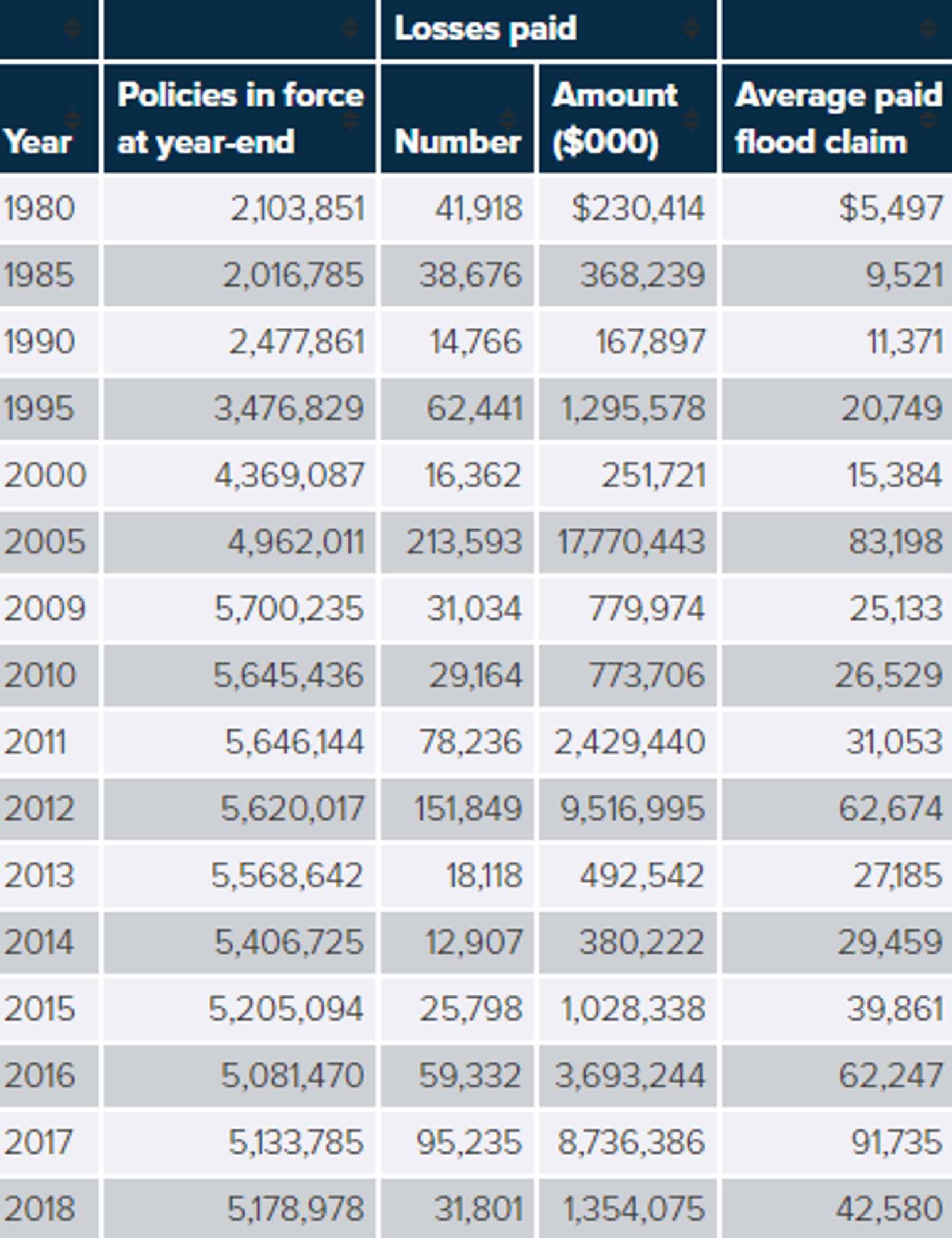

National Flood Insurance Program, 1980-2018

What Does Flood Insurance Cover?

Most types of water damage claims are addressed by your home insurance policy, which may include burst pipes, spills, accidental overflows or failed water heaters or appliances. Any of these home mishaps may look like a flood as the water pools in your home, but for insurance purposes, these aren’t considered floods. A private insurer is much more specific, to the point that commercial property owners and those on residential properties need to know exactly what’s covered.

Insurers sometimes refer to flooding as overland flooding, which makes the concept of flooding a bit easier to understand. If the water touched the ground before it came into your home, it’s a flood — and a standard homeowners insurance policy won’t cover the damage.

A flood policy, however, is designed specifically to cover overland flooding and can protect your home itself as well as the contents of your home. Remember, the rates for flood insurance and the affordability of flood insurance change depending on what’s covered and the risks that you face.

Policy provisions can vary by insurer, but in most cases, homeowners purchase flood insurance through the National Flood Insurance Program (NFIP). Below are the two primary coverages offered with an NFIP policy, each of which is typically purchased separately and has its own coverage limit and deductible.

Building Coverage

Your home itself is at the heart of building coverage and the coverage extends to nearly everything attached to the interior of your home. It’s important to note, however, that basement or crawlspace coverage is limited. Even if you have flood coverage, avoid storing anything of value below ground level if you’re concerned about floods.

Subject to your coverage limit and deductible, your policy may cover damage to:

- Electrical and plumbing systems

- Other home systems, such as furnaces and water heaters

- Appliances, including refrigerators, dishwashers and stoves

- Permanent installations, such as paneling, carpeting, wallboard, cabinets and bookcases

- A detached garage (subject to limitations)

- Foundation walls

- Fuel tanks and well water tanks

- Solar energy equipment

Contents Coverage

Your personal belongings are covered by the contents coverage on your flood insurance policy. However, there are some rules and exclusions that apply to coverage. Items stored outside aren’t covered, items stored in the basement may not be covered and vehicles aren’t covered.

Comprehensive coverage on your auto insurance policy can help protect your vehicles against flood damage. Currency, precious metals and valuable papers are also excluded from coverage. Consider storing these items someplace where they are safe from rising waters.

Contents coverage on an NFIP policy may cover the following:

- Clothing, furniture and electronics

- Portable appliances, like air conditioners, dishwashers or microwave ovens

- Washing machines or dryers

- Food freezers and their food contents

- Curtains and loose carpets

Coverage for contents is paid at actual cash value, a depreciated amount based on age and is subject to your chosen deductible. Coverage for your primary residence is paid at replacement cost value, which is based on the cost of rebuilding the property.

However, NFIP policies require that the home be insured to at least 80% of its rebuild cost to avoid prorated coverage. Building coverage is also subject to a deductible.

Cost of Flood Insurance

The average cost of flood insurance is about $700 per year but this number may not be meaningful when estimating costs because rates can vary widely.

Flood insurance is priced according to risk. Insured value also plays a role but the role may be smaller than with home insurance because NFIP flood insurance is capped at a $250,000 coverage limit for building coverage and $100,000 for contents coverage.

Risk is determined by your home’s location. FEMA uses a system that assigns flood zones with letter codes to group properties according to their risk of flooding. Flood insurance rate maps (FIRMs) consider the elevation and the proximity to water to help understand risk. In some cases, an elevation certificate is also needed to establish a premium.

Generally speaking, you can expect to pay more if your home is near water or in a low-lying area prone to flooding. However, FEMA reports that about 20% of its covered claims are in areas that aren’t in a high-risk zone. The takeaway is that Mother Nature isn't always predictable and that more people should probably have coverage.

Preferred risk policies are available for properties in moderate-risk B, C, and X flood zones, which typically have lower premiums.

Both contents and building coverage are subject to a deductible, which is the part of a claim that you pay. For homes with a building coverage of less than $100,000, the minimum deductible for an NFIP policy is $1,000. For homes insured for more than $100,000, the minimum deductible is $1,250.

You can choose a higher deductible, which often leads to lower premiums. However, some lenders may not accept deductibles of $5,000 or higher.

How Much Coverage You’ll Need

The average flood insurance claim is $30,000. You might think you can purchase coverage for a slightly higher amount and be okay, but it's likely that your coverage will be prorated if you choose an amount that's too low.

Property insurance, including flood insurance, uses a principle called coinsurance. With a policy that has a coinsurance clause, you'll be required to insure the property to at least 80% of its rebuild value to receive full coverage.

For example, if your home would cost $100,000 to rebuild but you only purchase insurance for $50,000, you can expect your policy to pay 50% of your claim up to your coverage limit. The deductible is also subtracted from the claim payment.

Ideally, you'll want to match your flood insurance coverage limits to those on your home insurance policy. Your home insurance provider has already done the math to calculate the cost of rebuilding your home. Contents coverage can use a similar approach but is limited to $100,000 with an NFIP policy.

Choose Flood Insurance for Your Home

As a technical matter, every home is in a flood zone. However, some homes are more at risk than others, like those near water or those in low-lying areas. Mother Nature can be unpredictable and many homes that you may not think to be at risk are damaged every year by flooding.

If you're in a low-risk area, there’s still a risk — but you'll often be rewarded with a lower premium. Choose your coverage amount and deductible carefully because both can affect how much of the loss is covered if you have a flood damage claim.

Interested in reading more? Check out Benzinga's guides to the best homeowners insurance, best car insurance and best health insurance companies.

Frequently Asked Questions

Does flood insurance fires?

Flood insurance covers fires caused by the effects of flooding already covered under the policy.

Does flood insurance fall under homeowners insurance?

Flood insurance is a separate policy from your homeowners insurance, meaning you will pay a premium for both throughout the year.

Methodology

Benzinga crafted a specific methodology to rank life insurance. To see a comprehensive breakdown of our methodology, please visit our Life Insurance Methodology page.