Filing your own taxes online may seem like a daunting prospect, but it doesn’t have to be. Even if you’re self-employed, have sold property or stock, have investment income or have other potential complications, you don’t have to spend money on an accountant. According to the IRS, 90% of people who file their own taxes use online tax preparation software, which is designed to guide you through the tax filing process with relative ease. In addition, you’ll learn a lot about your finances and taxes when you prepare your own taxes.

Step 1: Get Prepped and Organized

The most important part of tax preparation is not the 1040 form, it’s preparing to file and diligently tracking information throughout the year. Knowing your taxable events throughout the year and any deductions or credits you are eligible for is key to being able to file quickly and efficiently. Many itemized deductions require you to carefully keep track of your information throughout the year, such as business expenses and mileage or charity donations. Also, gather together last year’s taxes to see how much you received in state or local income tax refunds last year, if any. You’ll also need your Social Security number and that of your spouse (if filing jointly) and any dependents you claim.

Step 2: Check the Mail

Several forms will need to arrive in the mail before you file. Most taxable events or deductions will trigger a company to mail you a form (usually, you don’t have to scramble to calculate the information yourself).

- W-2 from your employer

- Form 1099 for wages earned as a contractor (one from each job with over $600 in earnings)

- 1099-DIV for stock dividend income

- 1099-B for sale of stock

- W-2G for gambling winnings

- 1099-G for unemployment income

- SSA-1099 for social security benefits received

- Form 1098 for mortgage interest paid

- Form 1098-E for student loan interest

- Form 1098-T for tuition payments

Your tax preparation software online will walk you through the different sections which cover your income, income adjustments, deductions and credits. For 2018, the form 1040 has been redesigned and simplified, but you’ll still file additional schedule forms.

Step 3: Employment Income

Most people have a W-2 form from their employer which outlines income and tax withholdings. Plugging this information into your tax preparation software is easy. For example, if the software asks what for the number in box 14, you enter the number. If you’ve multiple jobs during the tax year, simply enter each W-2 separately. If you were a contractor, enter the same information for your 1099 form. Remember, if you were a contractor and did not have your taxes taken out throughout the year, you will owe taxes on those earnings. Even if you did not receive a 1099 form or you earned less than $600 from a single client, you still owe taxes on your earnings.

Step 4: Business Income

If you’re self-employed, earned over $400, and file your taxes under your Social Security number and not under a separate legal business entity, then you would file a Schedule C form along with your 1040 form. Self-employment can be a side hustle or full-time business, but both require you to pay taxes on your income. Any online tax software will walk you through questions designed to understand the nature of your business and explain how to enter your income information. If you keep good records, you’ll simply plug the numbers into the right spots. The software will look for deductions based on your business type and have you fill in the data for applicable deductions, including mileage, home office deduction, supplies, and equipment.

Step 5: Non-Employment Income

If you earned income from receiving unemployment or Social Security benefits, that income is taxable and you will report the information as stated on your 1099-G and SSA-1099, respectively. You may also have earned income from the sale of stock or from dividends, in which case your broker will have mailed you forms to report that information. If you sold stock, you have to calculate your gains and losses. It can be pretty confusing to calculate your taxable basis, especially if you had stocks that you held over a long period of time that had reinvested dividends but even a novice can calculate it.

Most brokerage companies will be able to send you the information you need and help explain how brokerage accounts are taxed. Also, in this section, you’ll report any state or local tax refunds you received and any other miscellaneous income you’ve earned, such as from alimony, gambling winnings or even payment for jury duty. Don’t forget to report distributions from your medical savings account and your retirement accounts and income earned from the sale of property.

Step 6: Income Adjustments

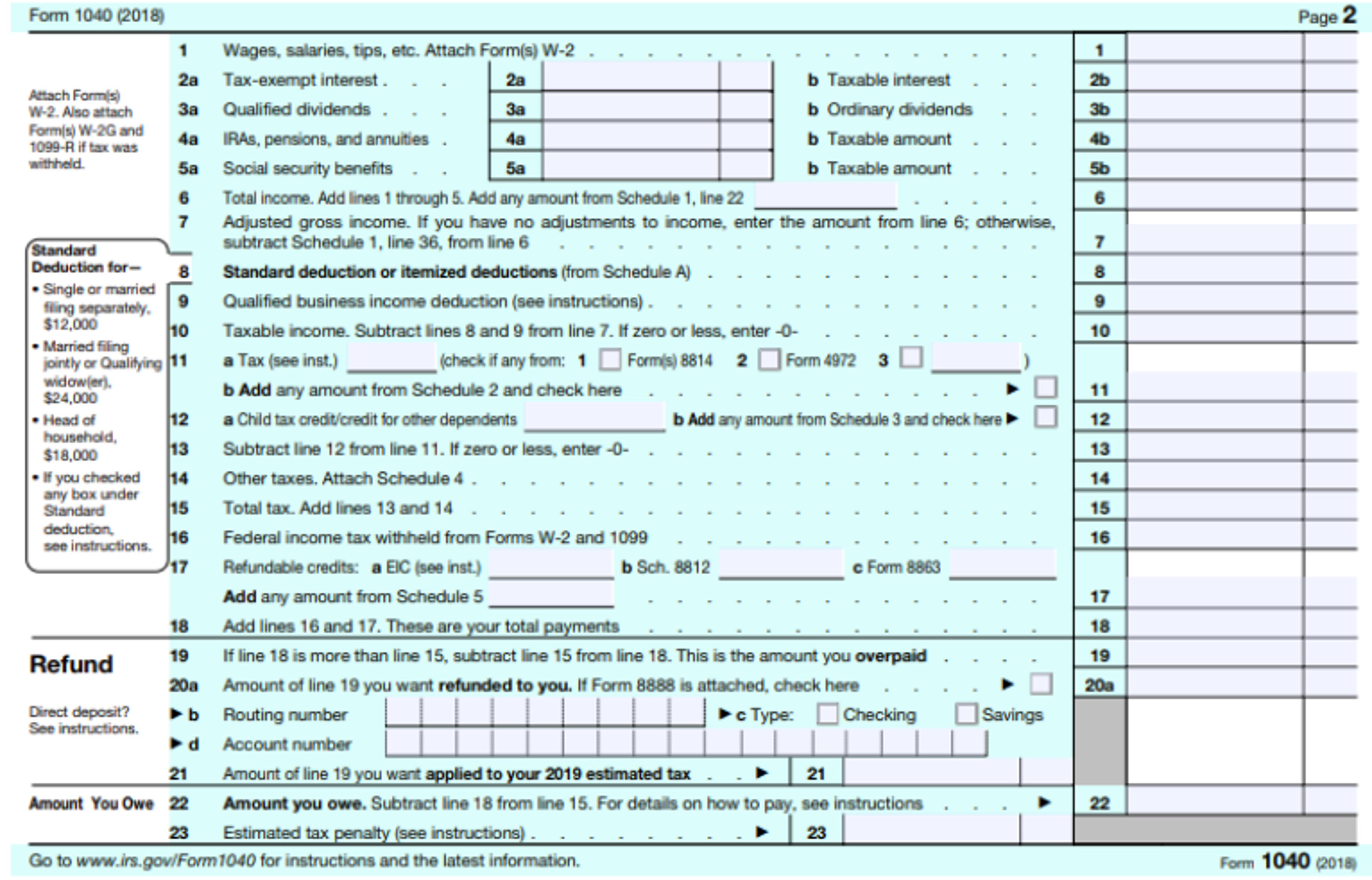

Now that you have entered your income information, calculate your adjusted gross income (AGI), the number that is your actual taxable income. The lower you can get your AGI, the better. To adjust your income down, you can deduct your mortgage and student loan interest paid, your IRA and medical savings account contributions and your self-employed health insurance costs.

Step 7: Deductions and Credits

Now comes the fun part. You may choose the standard deduction of $12,000 if you are single and $14,000 if you are married filing jointly and be done with it. Or, you can calculate what an itemized deduction would look like for you. Most online tax preparation software allows you to walk through all the itemizations and calculate them for you, then will tell you whether you would benefit most from the standard or itemized deductions. Spoiler alert: The standard deduction will most likely benefit you the most. If you gave a lot to charity, paid a lot in mortgage interest, had high medical expenses or paid high state or local income taxes, it may be worth your while to itemize.

It is an extra step and time consuming to walk through the deductions, but tax prep software is designed to look for deductions that apply to your situation and run the numbers for you. On the other hand, credits can benefit you whether or not you itemize and apply to you if you meet certain criteria, such as if you have low to moderate income, are a student, pay for child or dependent care, adopted a child, save a chunk of your income, have dependent children, made energy efficient upgrades to your home or are elderly or disabled.

How to Choose Your Tax Services

All tax prep software has some similarities in that it keeps up to date with the latest changes to the tax code so you don’t have to worry about knowing those details yourself. It also does the math for you. In fact, all the major brands guarantee accurate math and that it will get you the biggest refund possible.

Where the big differences lie is in the usability of the software (how easy it is to navigate and understand), how simple it can make the process for you by breaking down everything and the amount it costs. Most software will charge more to file your state return through an e-filing system, but if you want to avoid that charge, you can file directly with your state online using the information from your federal return. You may want to use the following, depending on your needs.

1. IRS Free File

If your income is below $66,000, you can use free online software at IRS Free File. If you make over $66,000, the IRS will make free fillable forms available but no software. Free File allows you to file your individual income taxes unless you own a business. You can also file many state taxes for free using the Free File system as well.

2. TurboTax

The industry leader in online tax software is TurboTax. To file your individual taxes, you can usually use the TurboTax software for free. You can upgrade to its paid versions which can offer live support from a tax professional and access to additional resources, like business filing of Schedule C forms, reporting investment income, and homeowner deductions.

You can pay between $39 and $89 to do your own taxes and $49 to $169 to have a CPA walk through it with you. The paid version of the software also saves your income and asset information year to year. The software is intuitive and very easy to use. It asks you simple questions to determine your income and taxable events, as well as the best deductions for you. The software also includes explanations of each step so that you can learn along the way. You can easily snap a photo or connect to a payroll server to import your W-2 information.

3. TaxSlayer

TaxSlayer is a less expensive time saver which still offers an easy-to-navigate interface. You can easily import your W-2 into TaxSlayer’s system. Like its competitors, it offers free state and federal filing for individual taxes and charges for additional forms and services for dependents, if you’re a homeowner, have investments, are self-employed or want a CPA to work with you. TaxSlayer’s plans start at $24 and go up to $47 for self-employed filers. Tax support via phone and email is included, even with the free version.

4. TaxAct

Phone and email tech support are free with TaxAct, which can provide extra assurance and information to a nervous self-filer. To save time, you can import your information year-to-year. The interface is very stripped down and simple, but is still easy to navigate through all the data points. TaxAct offers free simple federal and state returns like its competitors and its paid plans range from $9.95 for those with dependents and college expenses to $49.95 for self-employed filers.

5. H&R Block

If you want all the same online tax preparation software and also want the option to take out a loan against your refund, then H&R Block has you covered. Their Ask a Tax Pro and Tax Pro Review services are staffed by professionals with 60 hours of training, 30+ hours of annual training per tax season, and their online filers have an average of 15 years of experience in their field. You can file for free using software if you have dependents and are not a homeowner; paid plans range between $29.99 and $79.99. You can easily import information into the H&R Block system from other tax preparers and can upload a photo of your W-2.

Final Thoughts

A smidge of know-how, good organization, and a reputable online tax filer can help the online tax filing go smoothly. Pick the right service, because it matters. Select the software that makes you feel the most comfortable and ensures that you fully understand the process, no accounting degree required.