In 2018, the average cost of tuition, room and board at an in-state public school topped $30,000 annually. That means the sticker price of a 4-year degree at a public school comes close to a $100,000 investment. Private school tuition can cost even more — but remember, that’s before you add grants and scholarships and everything you'll need when you learn how to pay for college.

Daunting numbers? Sure. But smart school choices and excellent planning mean that you can take advantage of several ways to pay for college. The best way to fund your education is with grants and scholarships, then your money, and then finally with student loans.

- Method 1: Savings

- Method 2: Grants

- Method 3: Scholarships

- See All 8 Items

Method 1: Savings

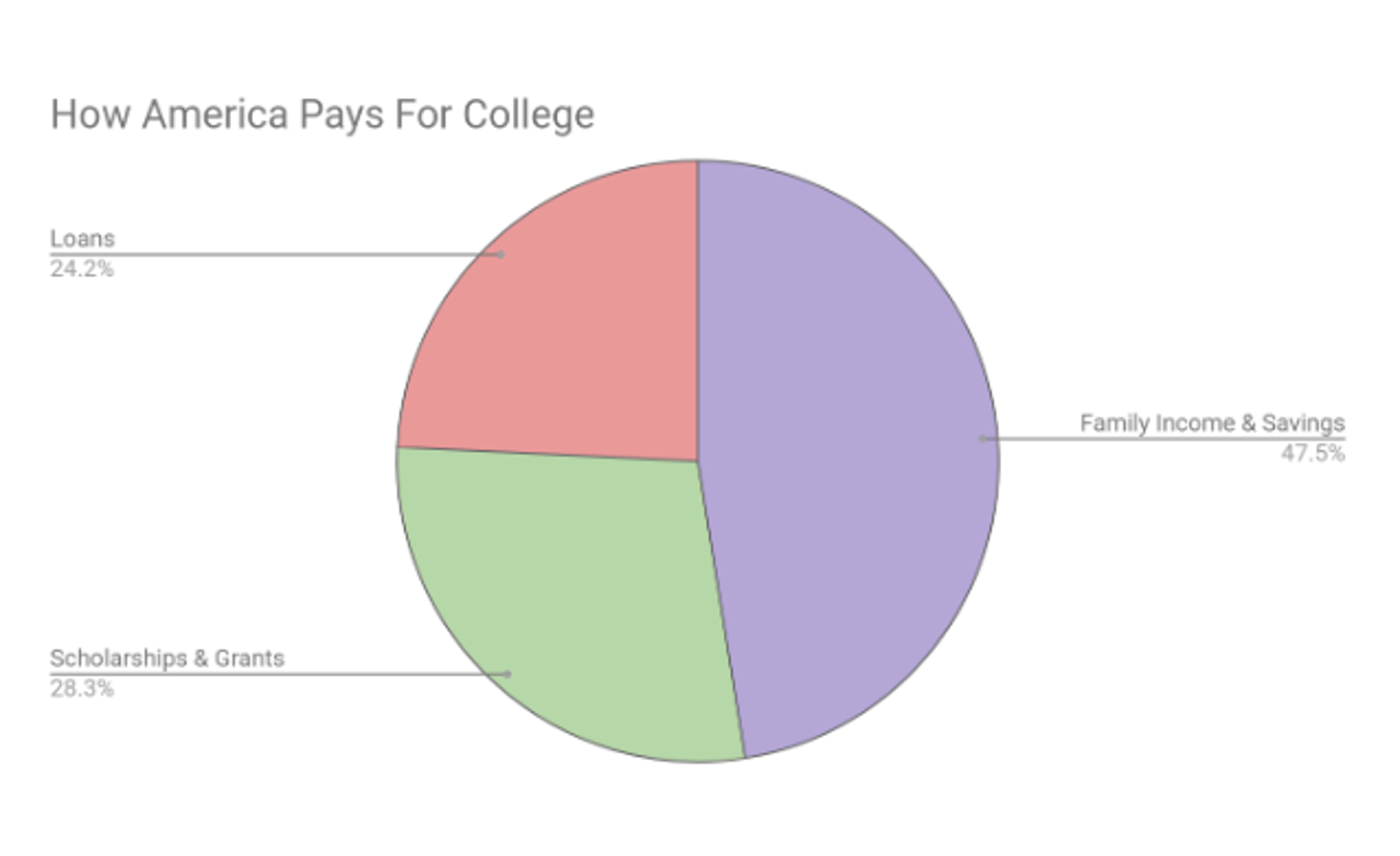

In 2018, about 47% of families paid for college out of savings or their income, according to Sallie Mae. Planning for these payments is key. Investing in a tax-exempt 529 college savings plan allows parents and students to let time and compound interest work in your favor.

Plus, the growth on your investments is not federally taxable, which saves you some cash on the back end when you go to use the money.

Starting a college savings plan for a baby allows the money to grow for nearly 2 decades. The best way to save money is through a 529 plan, and to save early and often, in order to pay for a big chunk of your education.

Method 2: Grants

Federal grants provide money you don’t have to pay back as long as you meet the eligibility requirements and continue to make satisfactory academic progress.

Students who exhibit exceptional financial need can be awarded a Pell Grant of up to $6,195 for the 2019-2020 academic year. Pell Grant eligibility is based on financial need and expected family contribution (EFC).

It can be awarded for up to 12 semesters if you still remain eligible and as long as you apply each year using the FAFSA form. You’ll also be considered for other federal grants when you file the FAFSA if you are:

- An undergraduate student with exceptional financial need.

- Studying to be a teacher and agree to work for 4 years after graduation in a high-need/low-income school.

- A student whose parent or guardian died as a result of their military service in Iraq and Afghanistan post-9/11.

Each state also has its own grant programs. Some state programs are need-based and some are based on your program of study. Research grants available in the state you reside in and from the state you are attending school because you could be eligible for grants in either or both.

Your university’s financial aid office may even automatically give you state grants you’re eligible for after you submit the FAFSA.

Method 3: Scholarships

Another ideal way to get free money that doesn’t have to be paid back is to be awarded scholarships. On average, 28% of most students’ tuition is covered by scholarships and grants.

Scholarships are usually merit-based, which means they’re based on your particular skills or abilities. For example, a merit-based scholarship might be awarded based on a student's high grades.

There are thousands of scholarships available in widely varying amounts. You can get a scholarship from your school, one from a local business and even one from a charitable organization. Websites like FastWeb and College Board can help direct you to a list of scholarships you may be eligible for. Don’t forget to ask about scholarships sponsored by local businesses in your town.

Make applying for scholarships your part-time job in your later years of high school and throughout college. Sometimes all you need to do to apply is to fill out a form, but most require some kind of essay as part of the application process.

If an essay gains you even a $500 scholarship, it’s absolutely worth your time and attention.

Talk to your school’s financial aid office to see if there might be any other scholarships you could work toward. If you are a talented athlete, you may be able to get an athletic scholarship. Schools also offer scholarships for artists, musicians, scientists, dancers, singers and other non-academic related talents.

Method 4: Military Service

Serving in the military is a great way to pay for your education and make yourself more marketable in the workforce. With a multi-year commitment to service in the Army, Navy, Marines, Air Force, Coast Guard or National Guard, you can gain valuable training and experience and fully-paid-for college education.

The average commitment to full-time military service is 4 years but can vary from 2 to 6 years and include additional years in the Individual Ready Reserve (IRR).

The Montgomery GI Bill-Active Duty program (known as MGIB-AD or Chapter 30) is for current and former military personnel who have at least two years of active duty service.

You can get up to 36 months of education benefits, based on the type of training, length of service, college fund availability and whether you contributed to the $600 buy-up program while on active duty. Benefits last for up to 10 years, but the time limit can be extended.

You may be eligible to enroll in a tuition assistance program while you are active duty and work on getting that degree before you have completed your service commitment.

If you want to go to college straight out of high school but you know you want to join the Army, Air Force, Navy, or Marines, you can opt for the Reserve Officer in Training Program (ROTC). This allows you to attend school full-time on the government’s dime and be commissioned as an officer when you graduate and start to fulfill your active duty commitment to the military.

These are rigorous programs designed to craft future military leaders and each branch has different requirements for their ROTC program, as well as a list of colleges and universities that offer it. Each ROTC program has a mix of specialized military training courses you take as electives at your university interspersed with your regular academic studies.

If you take the opposite approach and join the Army or Navy after you take out loans for your education, you might be eligible for tuition reimbursement programs for active military service personnel with up to $65,000 reimbursed incrementally over your years of commitment.

Method 5: Consider Working Through School

Working your way through school can fill in the gaps that savings, grants and scholarships don’t cove. It also allows you to get valuable work experience while you complete your degree. Employers are often impressed to see applicants’ ability to multitask, prioritize and follow through on multiple commitments.

Even if you didn’t work jobs relevant to your career field, those jobs will not only help pay for college but can help you get a job after college. Working during the school year or even over the summer can help you get the money needed for tuition. Careful budgeting will help you meet your educational goals and also teach you how to be fiscally responsible.

If you want to be a teacher, working part-time at a school or as a nanny might be a good fit. If you want to be a writer or publisher, working as a freelance writer or editor gains you valuable experience. A job as a bank teller gives you a literal hands-on approach to dealing with other people’s money if you want to go into finance.

You can also look for a work-study program that can get you a job through your university, allowing you to stay on campus and work around your class schedule.

Method 6: Federal Loans

Cobbling together money from grants, scholarships and family savings might mean that you’re still short the cost of tuition, room, board and fees. On average, 24% of a student’s college costs are paid for with loans, either federal or private loans.

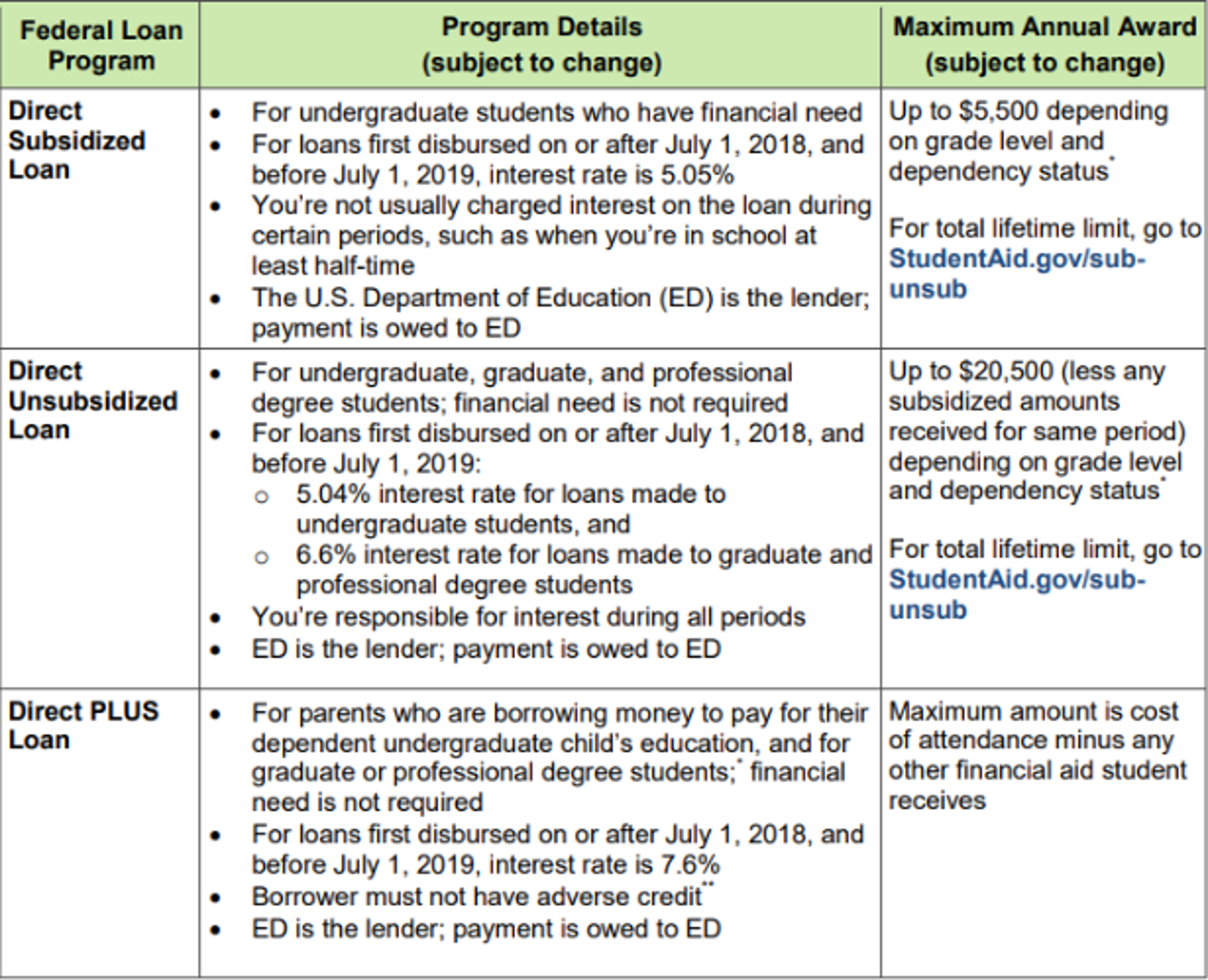

Federal loans are backed by the U.S. Department of Education. There are 2 types of federal student loans, Federal Direct Loans and Direct PLUS loans.

Direct Loans

Direct Loans can be subsidized, which means that the government covers the interest on the loan while you’re in school. They can also be unsubsidized, which means the government does not cover the interest on your loan. Both types are fixed-rate loans.

Loans that originated after July 1, 2018, and before July 1, 2019, are 5.05% for undergraduates and 6.6% for graduate students. These loans are a great first option for student loans because their rates are low and fixed, they discharge when the borrower dies or becomes permanently disabled, but the loans cannot be discharged in bankruptcy.

You may be eligible for loan forgiveness if you work as a teacher or the government and make payments during the first 10 years of the loan. Dependent undergraduate students’ total cap is $31,000 in both subsidized and unsubsidized federal student loans and graduate students are offered a $138,500 unsubsidized student loan cap (graduate students are ineligible for subsidized student loans).

Independent students are eligible for higher loan amounts than dependent students.

Direct PLUS Loans

Direct PLUS loans (commonly called Parent PLUS loans) are loans for parents to pay for their children’s college costs. These loans are in the parent’s name and not the name of the student, so the parent is legally responsible for repaying the loan.

The borrower has to have a good credit history and the loans are offered at a fixed rate of 7.6%. Parents can borrow up to the full amount of the cost of attendance, minus any other financial aid. Direct PLUS loans can also be discharged upon the death of the student and can be deferred while the student is in school at least part-time.

Method 7: Private Loans

There are many loan companies that can cover the remaining costs of college with a private loan. These loans are based on your credit history and therefore can be a higher interest rate than federal loans.

You can get a co-signer to help you get the loan and a better interest rate, but both signers are legally responsible for the balance of the loan.

Many companies also offer variable rate loans, but interest rates can rise. In any private loan situation, be sure to read the fine print. Private student loans often cannot be discharged upon the death of the student, nor can they be discharged in bankruptcy.

Carefully Choose How to Fund Your Education

Your full financial aid award will detail all the grants, scholarships, loans and other aid you’re awarded, and financial aid awards are all different even if you’re going to the same school as your neighbor or your best friend. Therefore, it’s important to consider the appropriate college funding options for yourself.

Overall, the best way to pay for college is to start by getting as much free money through grants and scholarships as possible, then use your savings and work as much as you can to pay for your tuition and living costs. If you’re still short and have to borrow money, the best loan option is a federal subsidized student loan.

Each funding option has a list of pros and cons, so weigh each choice carefully as you consider how to fund your education.

About Ryan Peterson

Ryan Peterson is a seasoned personal finance writer with a Bachelor’s Degree in Business from Indiana University. With over five years of experience, Ryan has crafted insightful content for multiple finance websites, including MoneyLion At Benzinga, he brings his expertise and passion for helping readers navigate the complex world of personal finance and investing, empowering them to make informed financial decisions.