No matter which tax bracket you’re in, you probably want to pay as little in taxes as possible. Luckily, the Internal Revenue Service (IRS) offers a number of tax credits and deductions that you can take advantage of to lower your tax burden when filing your federal income taxes.

But what is the difference between a tax credit and a tax deduction—and for which do you qualify? We’ve summarized the difference between tax credits and deductions in one convenient place, along with some advice on how you can use some of the most common creditsand deductions to save money during tax time.

Overview: What is a Tax Credit or Deduction?

A tax credit is a direct reduction to the amount that you owe in taxes. Tax credits give you a dollar-for-dollar reduction after you’ve calculated how much you owe to the IRS. For example, let’s say that you owe $10,000 in taxes but you have a $1,000 tax credit. The tax credit would be subtracted from your total tax liability, and you would actually owe $9,000.

Though some tax credits are refundable, most are not (this means that if you owe less than the amount of the credit, you can keep the remainder of the credit post-filing)A tax deduction is a subtraction to your total gross income. Tax deductions allow you to pay less in taxes because they lower the amount of taxable income that you’ve earned.

When calculating your income taxes, capital gains taxes, and brokerage taxes, you may subtract your deduction-amount from your total income and you’ll only have to pay taxes on the remainder following the subtraction. For example, let’s say that you earned $50,000 last year and you have $10,000 in tax deductions. You would be able to subtract that $10,000 from your income and you would only be responsible for paying taxes on $40,000 of your income.

Type | Definition | Common in Education | Common in Retirement | Common in Self-Employment | Common in Green Energy Credits |

| Tax Credit | Subtracted from your tax liability | The American Opportunity Credit and The Lifetime Learning Credit | Can deduct between 10% and 50% of $2,000 in contributions to an IRA, 401(k), 403(b) or another retirement plan | None | None |

| Tax Deduction | Subtracted from taxable income | Deducting student loan interest and teacher expenses | Deduct a percentage of what you paid into a traditional IRA | Office supplies, company vehicles used to travel to clients, and even a percentage of your mortgage and utilities may be deductible from your income | Subtract 30% of the cost of solar panels from your tax liability. Get between $2,500 and $7,500 if you’ve purchased a rechargeable vehicle |

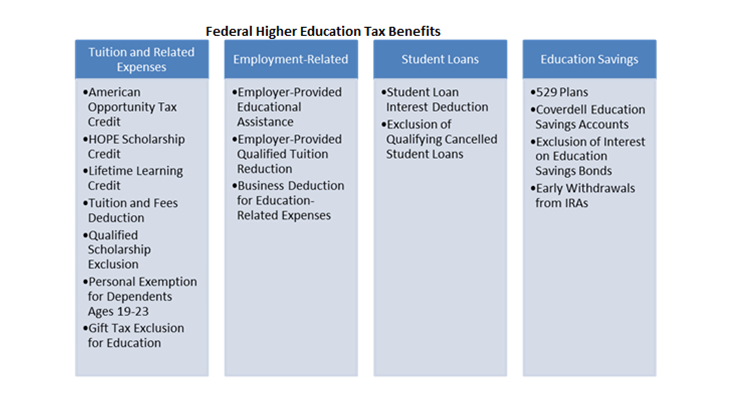

Credits vs. Deductions in Education

Depending on where you're at in you're education, you may qualify for different tax credits

Credits in Education

There are two major tax credits that students can take advantage of when filing their taxes: the American Opportunity Credit and the Lifetime Learning Credit.The American Opportunity Credit allows most students with at least a half-time course load to credit $2,500 to their taxes for tuition, books, activity fees, and other expenses associated with attending college.

The student must not be classified as a dependent, must have an adjusted gross income (AGI) of less than $90,000 and must have no felony drug convictions. The Lifetime Learning Credit allows students to credit $2,000 to their tax burden even if they do not meet the qualifications for a part-time student as long as their adjusted gross income (AGI) is less than $66,000. The American Opportunity credit and the Lifetime Learning credit are mutually exclusive—you can take one or the other, but not both.

Deductions in Education

If you have student loans that you have paid interest on in the previous year, you can deduct the cost of your interest from your gross income up to $2,500. Additionally, teachers and other educators can deduct up to $250 that they’ve spent on classroom supplies from their income.

Credits vs. Deductions in Retirement Saving

If you're using a tax-advantaged retirement vehicle, you may be eligible for special credits and deductions.

Credits in Retirement Saving

The Saver’s Credit allows you to deduct between 10% and 50% of $2,000 in contributions to an individual retirement account (IRA), 401(k), 403(b) or other retirement savings plan from your tax liability. Additionally, contributions made to your 401(k) through direct paycheck diversion are untaxed by the IRS—so make sure you max out your contributions if possible, especially if your employer offers a match program.

Deductions in Retirement Saving

Depending on your income, you may be able to deduct a percentage of what you paid into a traditional IRA from your income. These deductions are only valid for traditional IRAs—Roth IRAs are always subject to investment taxes, no matter your income or bracket.

Credits vs. Deductions in Self-Employment

If you are self-employed, there are a wide range of deductions that you can make to your income associated with the costs of doing business. Office supplies, company vehicles used to travel to clients, and even a percentage of your mortgage and utilities may be deductible from your income depending on the nature of your business and your income levels. Self-employed men and women are advised to carefully document their expenses throughout the year so they do not end up overpaying on their income tax.

Credits vs. Deductions in Green Energy Credits

Going green can come with a credit, but not a deductionThe Residential Energy Efficiency Tax Credit allows you to subtract 30% of the cost of solar panels from your tax liability, while the plug-in electric-drive motor vehicle credit allows you to get between $2,500 and $7,500 if you’ve purchased a rechargeable vehicle. According to the IRS, your vehicle must “have four wheels” and be propelled “to a significant extent” by a rechargeable battery that can operate for at least four kilowatt hours.

Final Thoughts

Though we’ve listed some of the most commonly-claimed credits and deductibles, the U.S. tax code is filled with hundreds of credits and deductions—more than anyone could possibly memorize or compile in a single list. If you file your own taxes, we recommend that you use a comprehensive tax filing software to fill out your return. These programs are constantly updated with currently-available tax deductions and credits so you can take advantage of every dollar at tax time.

About Sarah Horvath

Sarah is an expert in the insurance, investing for retirement and cryptocurrency space.