If you’ve removed yourself from the rat race, congratulations! Now that you’re officially retired, you might be wondering just how your retirement income is taxed and how different income sources are treated by the IRS.

As you probably already know, your tax situation might have changed a bit in retirement. Read on for tips and tricks to learn how file taxes once you stow your briefcase.

What Parts of Your Retirement Income are Taxed?

Federal law taxes different sources of income at different rates, provides different rules and rates on income from pensions, Social Security, retirement savings accounts and investments.

State taxes vary by state and there are even a handful of states that do not tax income from Social Security or retirement, though federal taxes still apply.

Pensions

You have to pay income tax on your pension in the year you take the money, though you might want to look into what your state’s tax treatment is for pension income. Some states don’t tax pension income and some do.

You will also owe federal income tax at your regular rate as you receive the money from pension annuities and periodic pension payments. Did you take a direct lump-sum payout from your pension? If you did, you must also pay the total tax due when you file your return for the year you receive the money.

Social Security

You may be surprised to learn that though you paid into Social Security throughout your working years, you are indeed taxed on the Social Security monthly retirement, survivor and disability benefits you receive. You are not taxed on supplemental security income (SSI) benefits.

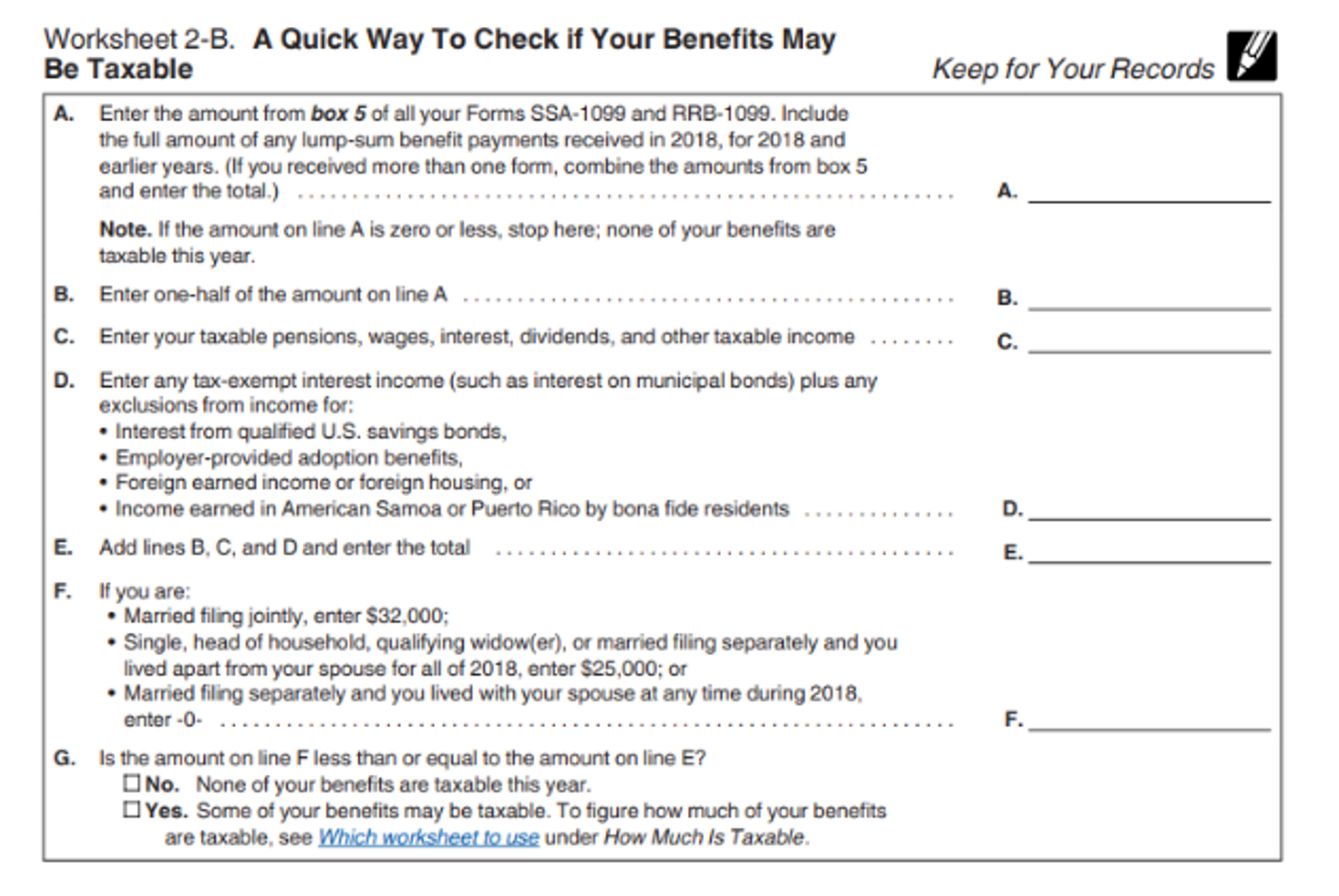

The percentage of your benefits, which are subject to taxation, depend on your income. If your retirement income is over the base amount of $25,000 if you are single or $32,000 if married filing jointly, then you need to run the numbers to determine what percentage of your Social Security benefits are taxable. To do so, calculate half of your Social Security benefits and add all your other income, including tax-exempt interest. If that total amount is more than your base amount, noted above, then part of your benefits are taxable. The IRS provides Worksheet-2B in Publication 554 to walk you through the calculations, or you can use the IRS’ interactive tool online.

Once you have determined that part of your benefits are taxable, then you have to determine how much is subject to tax. Most people won’t have to pay taxes on more than 50% of their Social Security benefits, but you may be taxed up to 85% of your benefits if:

- The total of half your benefits plus all your income is over $34,000 if single and $44,000 if married.

- You are married filing separately and lived with your spouse at any time during the tax year.

- You are a nonresident alien, though Social Security benefits may exempt under some tax treaties.

You can choose to have taxes on your Social Security benefits withheld voluntarily by filing a W-4V form or you can choose to pay them when you file your taxes annually.

IRA, Roth IRA, or 401(k) Withdrawals

Tax-deferred retirement investment accounts like an Individual Retirement Account (IRA), 401(k), 403(b) or Thrift Savings Plan (TSP) (for federal employees and military personnel) contribute pre-tax funds from your work earnings which are sheltered from tax as they grow in the account. Those funds may even continue to grow even after you begin taking required minimum distributions when you reach 70 ½ since you cannot keep those accounts tax-sheltered indefinitely. As you pull money out of your retirement accounts, you are taxed on the money as ordinary income since it was untaxed when it went in.

If you have Roth, whether it’s a Roth IRA, Roth 401(k) or Roth 403(b), there’s no required minimum distribution age, though you do have to withdraw the funds when the account holder dies. The funds you contribute to a Roth account are post-tax, so when you take a distribution from the account the entire amount is not taxable. As long as you have had the account for at least five years and you are at least 59 ½ at the time of the withdrawal, the IRS leaves all that money to you.

Other Income

For investments that are taxable, or not in tax-sheltered retirement accounts, your taxes change a bit. You make those investments with post-tax dollars so the money you withdraw is not taxed as ordinary income since you already paid taxes on those invested dollars. The interest earned in those accounts is taxed as ordinary income.

For investment growth, you only owe taxes on the amount your investment grew, your gains and those are taxed at a lower long-term capital gains rate of zero to 20%, depending on your tax bracket, provided you have held the investment for at least a year. Regular investment accounts lose the tax-sheltered growth of a retirement account, but they do provide greater flexibility. Because there are no required minimum distributions, you can leave the funds invested indefinitely or you can pull them out any time you need them.

How Retirement Taxes Vary by State

Many folks choose to stay in the place they have lived and work for the time prior to their retirement, but others decide that this new phase of life requires a move to a new, perhaps warmer, locale. If you are thinking of relocating, keep in mind that retirement taxes vary by state and where you choose to re-plant roots may impact your retirement money either positively or negatively. Several states don’t tax pension or social security payments and others don’t have a state income tax.

If you earned your pension income in one state and move your legal residence to a state with no income tax, like Texas or Florida, your former state cannot tax your pension income. Of course, many states make up for low or no income taxes by levying higher property taxes or sales taxes, so be sure to run the numbers before you move for a tax break.

Filing Your Retirement Taxes

Now that you have a basic understanding of the different ways in which your retirement income is taxed, you’re ready to gather your documents and IRS worksheets to get ready to file your taxes.

What You’ll Need in Hand

Depending on your sources of income in retirement, you will need to gather the following relevant documents to file your income taxes.

- W-2: If you work at all, even if part-time or a whole new encore career, you will need a copy of your W-2 earnings statement

- 1099: If you earned more than $600 from freelance, consulting, or contract work, be sure you receive a 1099 from the company which hired you.

- SSA-1099: Your Social Security benefits statement will show the total amount of benefits you received and how much you will report as income.

- IRS Worksheet 2B in Publication 554: Worksheet-2B will help you calculate what percentage of your social security benefits are taxable.

- 1099R: If you received distributions, your pension plan, annuity, or retirement account will send you a 1099R showing how much you received. If you are a federal retiree, you’d receive a CSR 1099R, which is similar.

- Simplified Method or General Rule Worksheets: These worksheets help you calculate how much of your pension or annuity payment is taxable.

- 1099-B: This form reports capital gains and losses and is sent by your investment advisor or brokerage company.

- 1099-INT: This form reports interest income earned and is sent by your investment advisor, broker or banker.

- 1099-DIV: This form reports dividend income earned and is sent by your investment advisor or brokerage company.

Where You Can File

You can choose to file by hand using paper forms, online using reliable tax software or take your paperwork to a tax professional to have him or her file on your behalf. Which you choose depends on the complexity of your tax situation and your familiarity with your taxes, forms needed and tax law. It can never hurt to have a tax professional walk you through your tax situation, especially if you’re just now becoming familiar with retirement taxes. Both tax professionals and tax software can help you maximize your return to ensure you take all the deductions and credits you’re entitled to.

Both tax professionals and tax software can help you maximize your return to ensure you take all the deductions and credits you’re entitled to.

Final Thoughts

Taxes in retirement can be far more complicated than when you just had to file a single W-2 while you were working. Now that you have income from several sources, including pensions, annuities, Social Security, retirement accounts and investments, you may find that you have a learning curve to get familiar with all the different rules and tax rates. But getting familiar with the basic tax rules on each type of retirement income and how they are taxed can help you make smart financial decisions for your retirement, tackle your taxes and enjoy your time to the fullest.