Introduction

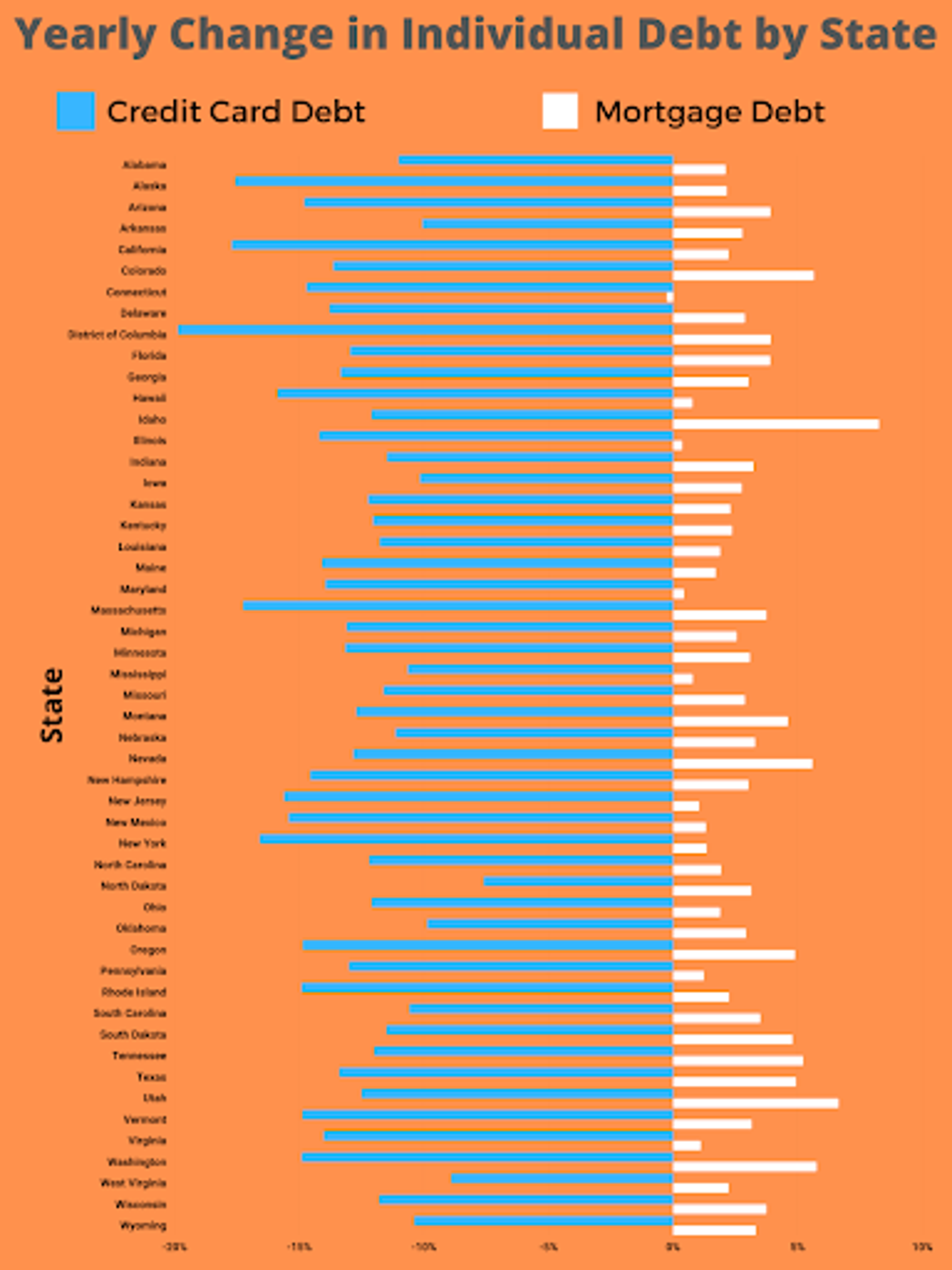

The COVID-19 pandemic acted as a wake-up call for people all around the world, especially in the United States, as it completely transformed the way we work, go to school, and conduct our daily lives. However, though it increased unemployment and mental health issues, the coronavirus also paved the way for increased savings, better personal finance habits, and fiscal stimulus. These factors combined with low-interest rates for personal loans to create a downtrend in credit card debt across the country, with an average decrease of 13.34% nationwide.

On the other hand, mortgage debt increased by an average of 3% across the United States primarily due to the boom in the housing market, as home prices rose to the highest levels in over a decade. In fact, a majority of this household debt has accumulated from initial mortgage purchases as well as refinances due to the aforementioned low rates. To add, the pandemic caused people to borrow less to finance their education and automobiles and shift the money into mortgages, another catalyst of the slight increase in mortgage debt.

Nevertheless, there is one glaring similarity in the catalysts for not only the change in credit card debt but also mortgage debt: low-interest rates. As the Federal Reserve starts to begin tapering bond purchases later this year, they may begin hiking rates in 2022, reversing the trends we’re currently experiencing in mortgage and credit card debt.

Read this edition of Benzinga Reports for an in-depth look at how the COVID-19 pandemic affected not only mortgage but also credit card debt by analyzing their change from 2019 to 2020. Discover how the debt levels vary state by state and whether there is any relation between mortgage debt and credit card debt.

Key Points: Mortgage Debt, Credit Card Debt

- 50 States & Washington D.C.

- Factors researched: Mortgage Debt & Credit Card Debt

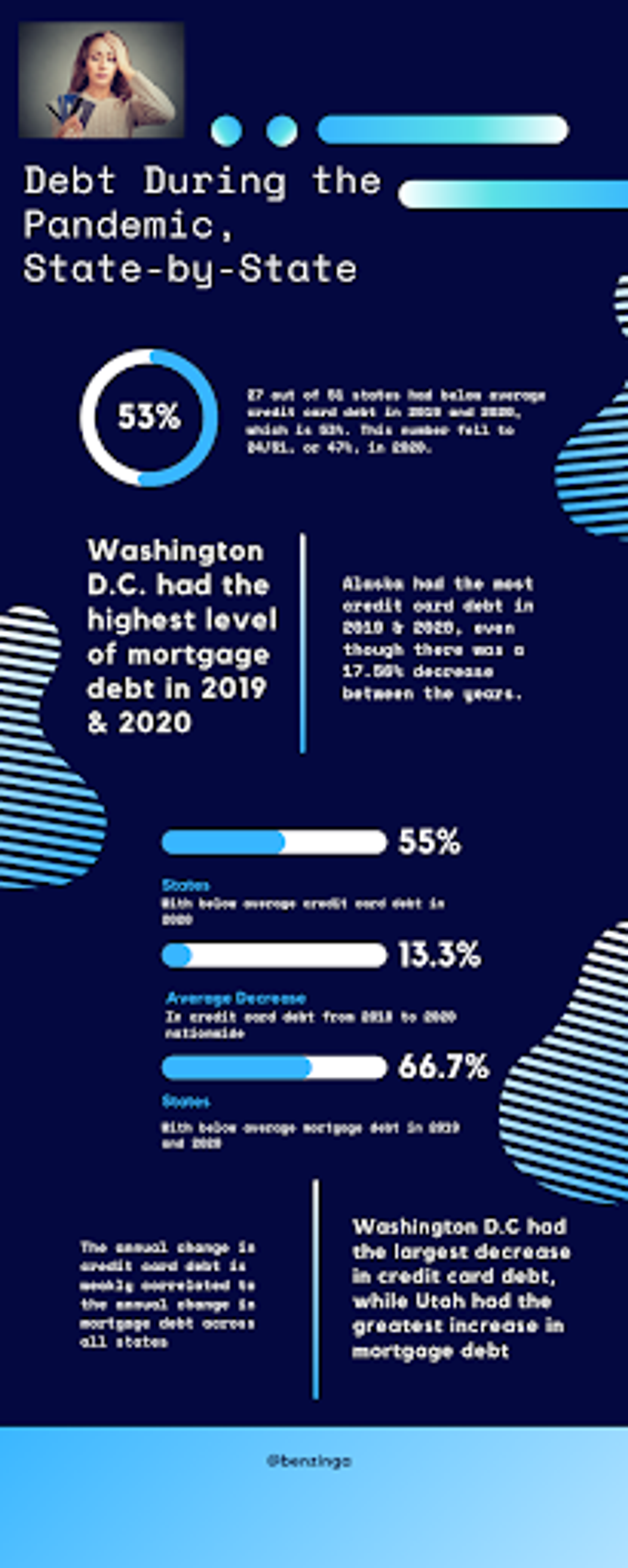

- States with above average credit card debt in 2019: 22/51

- States with below average credit card debt in 2019: 29/51

- States with above average credit card debt in 2020: 23/51

- States with below average credit card debt in 2020: 28/51

- States with above average credit card debt in ‘19 & ‘20: 20/51

- States with below average credit card debt in ‘19 & ‘20: 26/51

- States with above average mortgage debt in 2019: 17/51

- States with below average mortgage debt in 2019: 34/51

- States with above average mortgage debt in 2020: 17/51

- States with below average mortgage debt in 2020: 34/51

- States with above average mortgage debt in ‘19 & ‘20: 17/51

- States with below average mortgage debt in ‘19 & ‘20: 34/51

- Average credit card debt in 2019: $5,938

- Average credit card debt in 2020: $5,146

- Average mortgage debt in 2019: $187,156

- Average mortgage debt in 2020: $192,78

- Average Y-O-Y change in credit card debt: -13.34%

- Average Y-O-Y change in mortgage debt: 3.01

Diving Deeper: Correlations (or Lack of) Between Mortgage & Credit Card Debt

- States with above average credit card & mortgage Debt in 2019: 15/51

- States with below average credit card & mortgage debt in 2019: 27/51

- States with above average credit card & mortgage Debt in 2020: 13/51

- States with below average credit card & mortgage debt in 2020: 24/51

- States with above average Y-O-Y change in credit card & mortgage Debt: 15/51

- States with below average Y-O-Y change in credit card & mortgage Debt: 11/51

- States with above average credit card debt in ‘19 & ‘20: 20/51

- States with below average credit card debt in ‘19 & ‘20: 26/51

- States with above average mortgage debt in ‘19 & ‘20: 17/51

- States with below average mortgage debt in ‘19 & ‘20: 34/51

Methodology

To analyze a possible correlation between mortgage debt and credit card debt, we examined the change in all these entities for all states in the U.S. and Washington D.C.