As you consider building a rainy day fund, you need to know what you’re saving for, where to keep your money and how to plan for the future. Using these simple tips, you can begin saving even if you’ve never tried before.

What is a Rainy Day Fund?

A rainy day fund, in its purest form, is a savings account you keep for entertainment, travel or gift-giving purposes. The fund is meant to give you a bit of discretionary income that you can use throughout the year, planned or not.

Why Is a Rainy Day Fund Important?

A rainy day fund is important because it is the simplest way to gather funds for the things that make life exciting. Yes, your profession and supporting your family are, in the words of actor and comedian Robin Williams, noble pursuits indeed. However, there are certain things in life that make it fun, and you need money for those activities.

Vacations and entertainment: Vacations and entertainment are important for the family. Whether you travel or not, you want to have some cash set aside to make those activities happen. If you know precisely how much money you need, you should divide that amount by 12, aiming to save the exact amount of money you need to do your favorite things.

Hobbies: Hobbies can also be expensive, and you might set aside a few dollars every month to propel your hobby forward.

Unexpected expenses: While many people would say that you need a dedicated emergency fund for unexpected expenses, you may prefer to combine all that money in one account with your rainy day funds.

Large yearly expenses: If you make a massive purchase each year (annual life insurance premiums, annual passes to your favorite amusement park or summer camp for your child) you can divide that expense by 12 and save that amount each month.

Job loss: You might dip into your rainy day fund if you lose your job and need some time to find a new one.

Financial security: Having a savings account is better than not having one. At the very least, you can get started and begin saving so that you aren’t losing time.

How Much Money Should You Put in a Rainy Day Fund?

If you’re not sure how much money to put in your rainy day savings account, use these tips to organize your finances a bit better.

Create monthly budget: Create a monthly budget so that you can clearly see your income and expenses.

How much money is left after expenses: Subtract your expenses from your income to learn how much is left.

How many rainy day accounts do you keep: You can set up a rainy day savings fund for entertainment, and you might also set up an emergency fund.

Purchase roundups: Instead of just setting aside some money every month, use purchase roundups that save a few cents on every purchase. In this way, you’re always saving.

- Prizes & Features

About MoneyLion

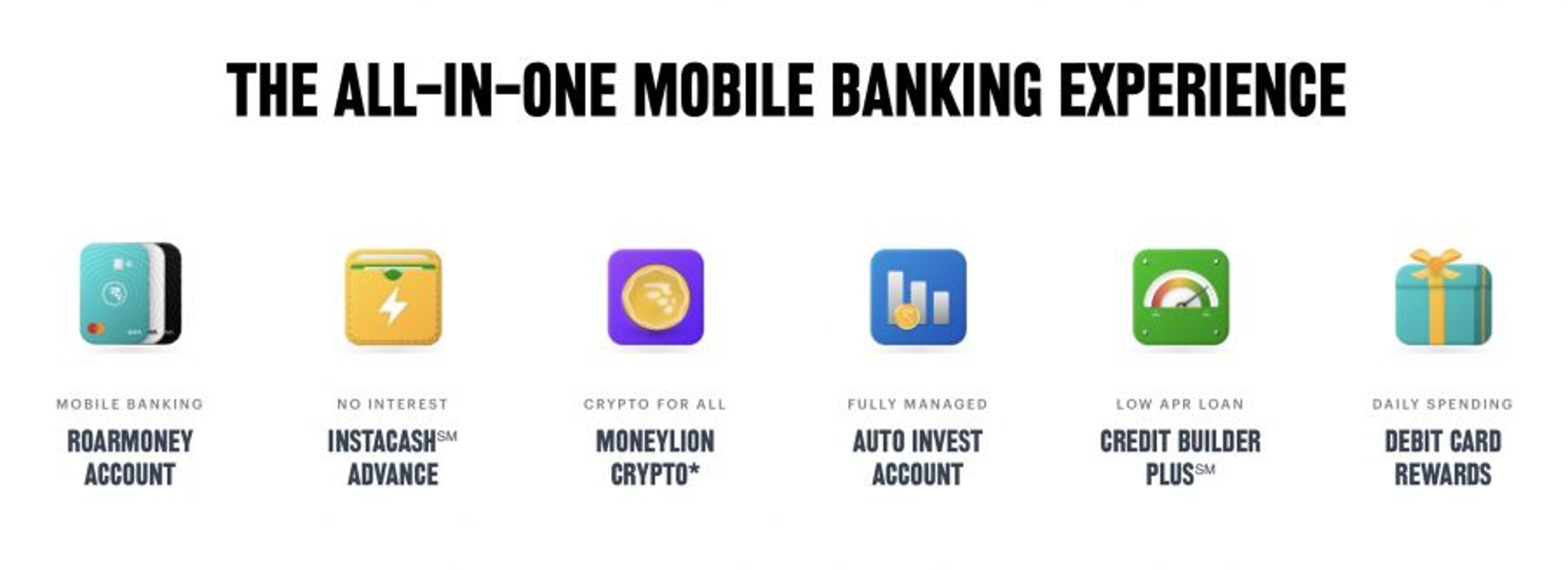

MoneyLion (NYSE: ML) is a digital financial platform that helps the 99% feel 100% about their finances. With a range of financial services, anyone can take control of their money using:

- Mobile banking

- Cashback rewards

- No hidden fees

- Financial calculators

- Buy now, pay later

- Get paid early with RoarMoneySM

- Investment and crypto accounts

- Credit-builder plus loan

- Cash advances

Create a Rainy Day Fund Today

You can create a rainy day fund today using the calculations noted above to plan for the future. Using a platform like MoneyLion is a great way to get started, and you might also use Benzinga to gather investment information to grow your fund that much more.

Frequently Asked Questions

What is the difference between a rainy day fund and an emergency fund?

A rainy day fund and an emergency fund are often seen as the same thing. However, it is best to set aside two savings funds. Your emergency fund should be used for car repairs, home repairs or medical expenses. A rainy day fund should be used for entertainment, gifts or travel.

How do I get a rainy day fund?

You can start a rainy day fund using any savings or checking account you prefer. There is no need to qualify. You simply need to start saving.

About Patton Hunnicutt

Patton Hunnicutt is a contributor and editor at Benzinga. He’s worked for several years on financial content, addressing issues related to personal finance, investments, retirement, and more.