The U.S. Fed is turning more hawkish, as noted by the Central Bank’s desire to bump median projections for the end-2015 and end-2016 Fed Fund rates up by 12.5bps to 1.125 percent and 25bps to 2.50 percent, respectively.

The increase in FFR was offset by the FOMC’s decision to cut the neutral rate (a rate level that neither stimulates nor restrains economic growth) by 25bps to 3.75 percent.

Currently, this is an environment with low volatility and tight credit spreads, which are market characteristics that may signal a coming market meltdown. Goldman Sachs GS mentioned in a note that when this current rally ends, it “will likely end for reasons that have little to do with the self-destructive complacency and excess leverage that normally follow sustained periods of low volatility.”

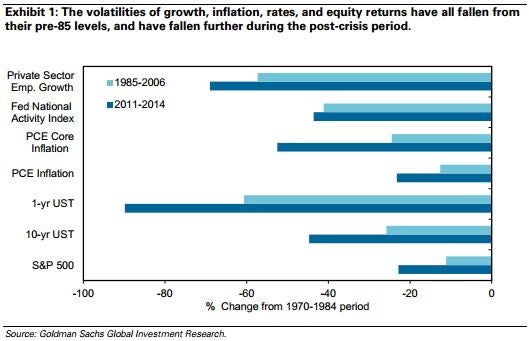

Observing the comparison between 1985-2006 and 2011-2014, volatility has dropped across select indicators and assets. This means that while central banks may suspend volatility in economic growth and financial markets for any period through their own policy, the action of doing so has the potential to induce complacency and leverage excesses. This historically brings abrupt ends to credit cycles that drive economic growth.

It also leaves observers and market participants wondering whether regulators in the U.S. are better apt now to identify excess leverage than they were in 2007, when bank and household leverage levels coupled with falling house prices drove large mortgage losses and obliterated confidence in financial institutions.

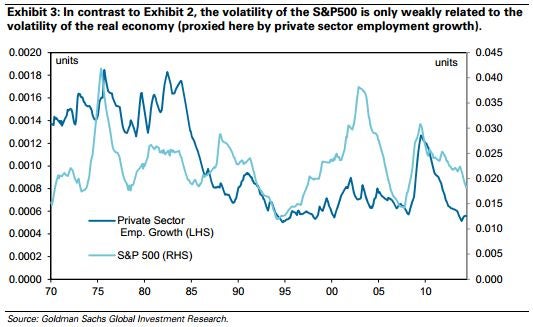

Further complicating the ability of the public to trust the central planners is the disconnect in the S&P 500 volatility from the volatility of the real economy, as proxied through private sector employment growth.

It’s no secret that the tech-heavy index disconnect may be driven by the 40 percent increase in Q1 profits this year over last year, along with the substantial premiums offered by technology firms being funded through either stock-options or cheap, Covenant-Lite loaded leverage-loan paper.

The lingering impact of macroprudential policies (also known as “anti-bubble” policies) may create a new skewing in the indicators used to measure financial system stresses. This would create a new form of hubris regarding excess leverage and the appearance of a problem-free environment in the midst of low-volatility.

Participants may want to adapt to the coming changes and take a pro-active measure to defend against a new manifestation of Fed and Banking hubris being driven by low-volatility and cheap money.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.