DO NOT POST YET PLEASE

Continued slow increases in most measures of labor compensation offer further evidence of labor market slack".

(Click To Enlarge)

All of this is taking place as inflation in food and energy begins to accelerate back toward the 2 percent level. The central bank noted

"...with wages growing slowly and raw materials prices generally flat or moving downward, firms are not facing much in the way of cost pressures that they might otherwise try to pass on". Anyone who's ran a business knows you cut costs and maximize selling price points to maximize margins.

Change In Chain-Type Index, Personal Consumption Expenditures

(Click To Enlarge)

Regarding actual wealth, the aggregate household net wealth reading approached 6.5x the value of disposable personal income in H1 2014. This is the highest this value has been since 2007 when wealth in terms of household valuations was approaching 7x the value of disposable personal income. It's truly amazing to see that on a price basis, nearly everything appears back to the pre-crisis levels. This is what happens when monetary policy is used to drive away depression, usher in euphoria, and left to run amok because of the simple nature of how easy it is to cut make money cheap and flood pockets of the system with drowning amounts of liquidity.

There is one bright spot here though. Even as the wealth-to-income ratio expands, the quality of borrowing conditions for households has eased dramatically thanks to banks easing up on standards for home purchase loans to prime borrowers coupled with easing credit standards for consumer loans.

(Click To Enlarge)

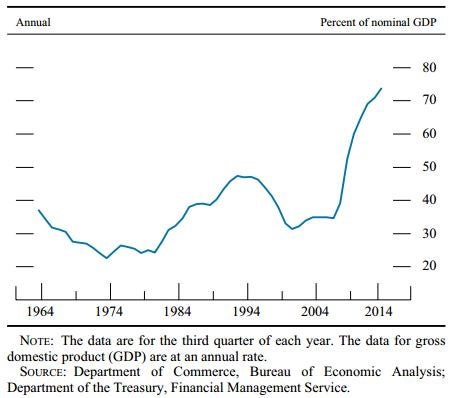

Though the citizens have managed their household debt situation, the same can not be said for the Federal government. The US Government has taking the nominal debt-to-GDP percentage to almost 75. Though debt has been paired with economic growth, the clear danger that was on citizen balance sheets has been transfer to the federal books.

(Click To Enlarge)

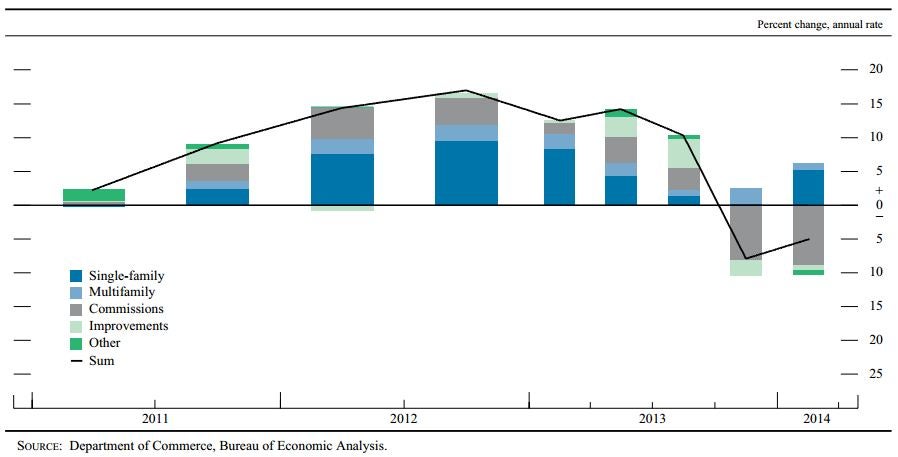

When Case-Shiller came out a few weeks ago the crowd proclaimed the virtues of a housing recovery. The problem is that the resiliency of this housing recovery is weak, at best. When rates spiked in late 2013 (Chart 1), the impact on total residential investment is clear (Chart 2).

(Chart 1)

(Click To Enlarge)

(Chart 2)

(Click To Enlarge)

Total residential investment is sensitive to interest rates. Though household debt has improved the burdens have been shifted from the citizens to the US government as it's debt-to-GDP ratio has swelled. The workforce in America is weak, at best. The true unemployment levels of America's skilled labor force is not allocation optimally. Thoughts costs are down, earnings and compensation have fallen while PCE appears to have caught some footing and is beginning to increase. Overall, the basic foundation of our economy is weak and all the FED did with its monetary policy was pull future demand forward when it started QE thus leaving the fractures to our economic policy open.

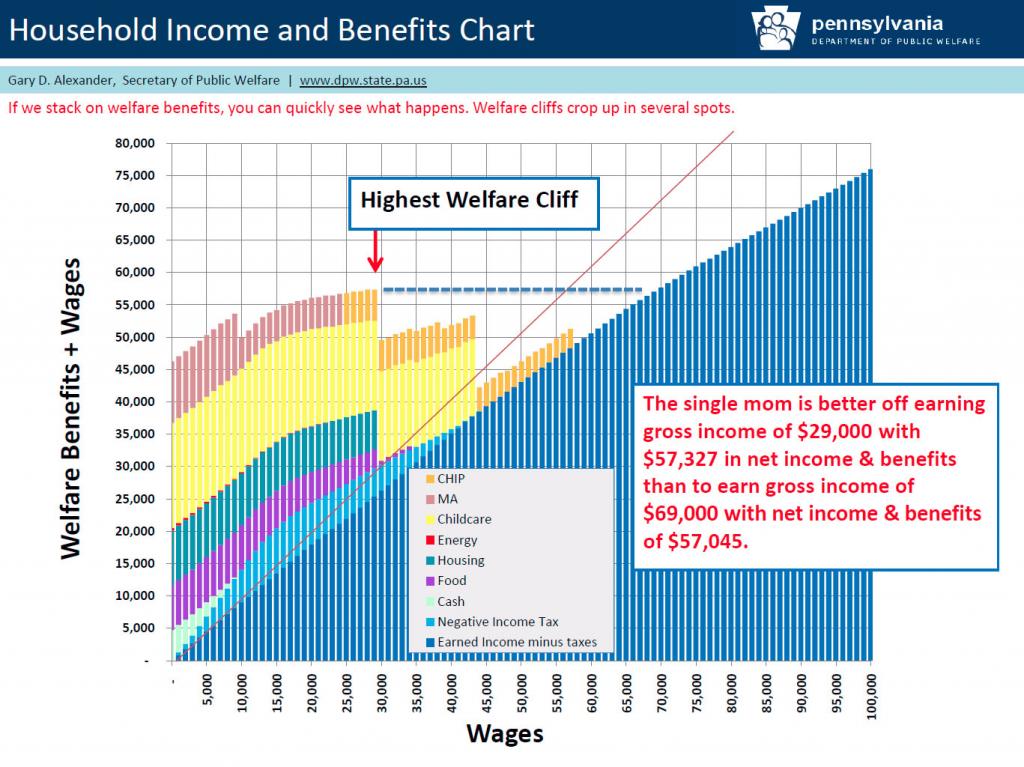

The performance of luxury retailers compared with discount retailers shows highlights a sample of the wealth gap that has increased in the wake of the Great Recession. The middle class has been left with the burden of tax increases to supplement state and federal spending. Single mothers earning a gross income of $29K annually with $57.3K in net income and benefits than to earn $69K gross annually with $57.0K in net income and benefits.

(Click To Enlarge)

We're in a mess and as each week passes we are coming closer to our day of reckoning.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.