Bookkeeping: Restarting Bucryus (BUCY) on Muted Response to Earnings

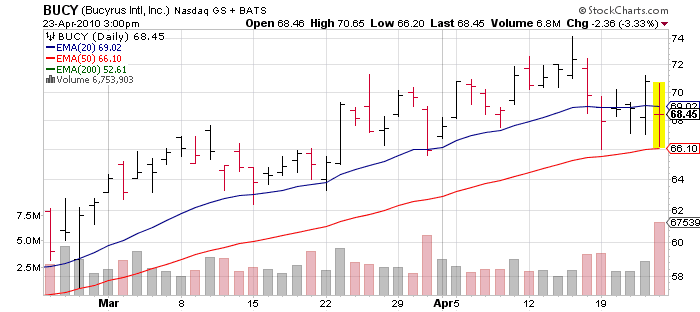

I am restarting a position in Bucryus (BUCY) as we have 2 things working in our favor to reduce risk. First, the company reported yesterday so earnings risk is out of the way; second, the stock is sitting right above the 50 day moving average so we have a clearly defined area to exit the position if we're wrong. We last were in the stock July 2009; stopped out at what is now an unmentionable price.

Bucyrus is an unique franchise essentially providing the tools for the world's miners to feed China. I absolutely loved the purchase of the Terex assets at the end of 2009; the synergies should be huge once integrated in the coming 12-18 months. Unfortunately it mostly trades as if it is a coal or steel stock rather than on its own merits but it is what it is. On $4 of EPS it is very reasonable, but has a low multiple due to the cyclical nature of its business - however that has not stopped other cyclical stocks from now sporting 30-50x type of PE ratios (which make no sense to me)

While I like the company, I will be heading for the exits if this important support below is broken. I've begun a 3.2% exposure around $68.40. Our key moving average is down at $66, which is exactly where the stock fell to earlier today. A move to that level would offer 3.5% downside risk which is manageable. If the stock can bounce a move to $74 should be a no brainer... then it has to break over that to start a new leg up.

Some flavor on today's earning report:

- Bucyrus (BUCY) the mining equipment maker, fell short of Wall Street targets by a wide margin when it reported first-quarter results after the market close Thursday, but the company's CEO is adamant that demand is building for Bucyrus' huge excavation gear.

- The company, in the midst of integrating its $1.3 billion acquisition of Terex's (TEX) mining-machinery unit, reported adjusted earnings of 69 cents a share for the quarter. Analysts on average were looking for 81 cents, according to various surveys of the sell side. All the numbers exclude results from the new Terex business, as well as costs related to the deal and the integration.

- Executives blamed the weak sales of underground machinery on "timing issues" related to shifting customer delivery schedules. Margins in that segment -- which produce machines to dig and construct mining shafts -- eroded during the quarter due to "under absorption," analysts say. Translated from the jargon, that means Bucyrus had ratched up its labor force in preparation for demand that never materialized, increasing costs.

- The company forecast 2010 revenue above analysts' expectations, but lower-than-expected quarterly results took its shares down as much as 5 percent.

- In a conference call with analysts, Bucyrus said it expects 2010 revenue to be $3.65 billion to $3.75 billion, including about $1 billion worth of revenue from Terex, which the company acquired in February. Analysts on average were expecting revenue of $3.35 billion.

- After market close Thursday, Bucyrus posted first-quarter results below analysts' expectations on lower revenue from its underground mining segment.

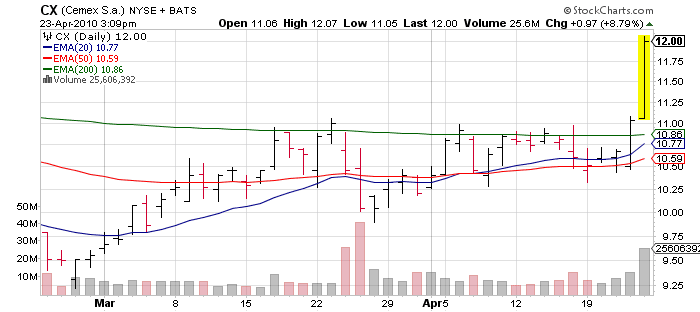

An interesting contrast in styles here... another "infrastructure" name that broke out today is Cemex (CX) so I will track both stocks mentally to see which would have been the better buy. Do you buy the one that pulls back, or do you buy the one that is surging... in this market, 90%+ of people who had chosen Cemex. (I think Cemex is rallying due to the "surprising" housing reports) So we'll check back in a few weeks to see if I made a mistake in my choice.

[Dec 22, 2009: More Color on Terex-Bucryus Deal]

[Dec 21, 2009: Bucyrus Buys Mining Assets of Terex]

Long Bucryus in fund; no personal position

The preceding article is from one of our external contributors. It does not represent the opinion of Benzinga and has not been edited.

© 2026 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.