The Missing Labor Link

Companies Focus on Productivity

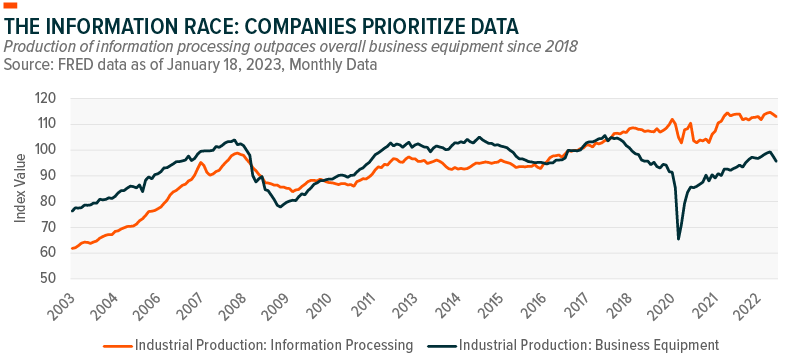

Productivity, or creating more per unit of input such as capital and labor, can help companies remain lean during economic downturns. The chart below shows a steady rise in industrial production focused on information processing, which outpaced overall business equipment production over the past four years. We expect digitization to be a focus of capital spending over the coming years.

Our sector views table below provides more detail on sector positioning and the current tailwinds and headwinds for each sector.

This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

© 2026 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

To add Benzinga News as your preferred source on Google, click here.