From the perspective of technical analysis, U stock arguably looks worse. From July through the present juncture, the security appears to be forming a bearish head-and-shoulders pattern. If so, the security may fall to the "natural" support line of approximately $24.

Despite these apparent risks to U stock, there are serious questions about the fundamental and technical approach. Essentially, both the premise and the conclusion are contingent on the person making the claim. As stated earlier, Unity trades at a 130-times forward multiple. Because that number "sounds big," traders might avoid it. But what does big even mean in this context?

As for the head and shoulders, who arbitrates the authenticity of this and other patterns? Who defines what a support line is or where to draw the line and how long to draw it? Bob? Susie?

We need a more airtight methodology and that's where the quantitative approach comes into play.

A Quantitative Dive Into U Stock

To quickly lay the framework, quantitative analysis — per Google's Gemini — is a method of evaluating a company’s performance and stock value using mathematical and statistical models, numerical data and algorithms. In my opinion, the fulcrum that distinguishes quant models from the fundamental or technical schools is the non-contingent premise.

All statements about the unknown future are necessarily contingent by definition. The flaw with the fundamental or technical approach is that the premise is contingent on the author; that is, the author perceives forward value or imminent patterns and thus writes about it. As such, the framing of the narrative integrates the author's bias as its own justification.

Such ego-driven "analyses" are fine if the author guesses right. If not, the whole argument collapses.

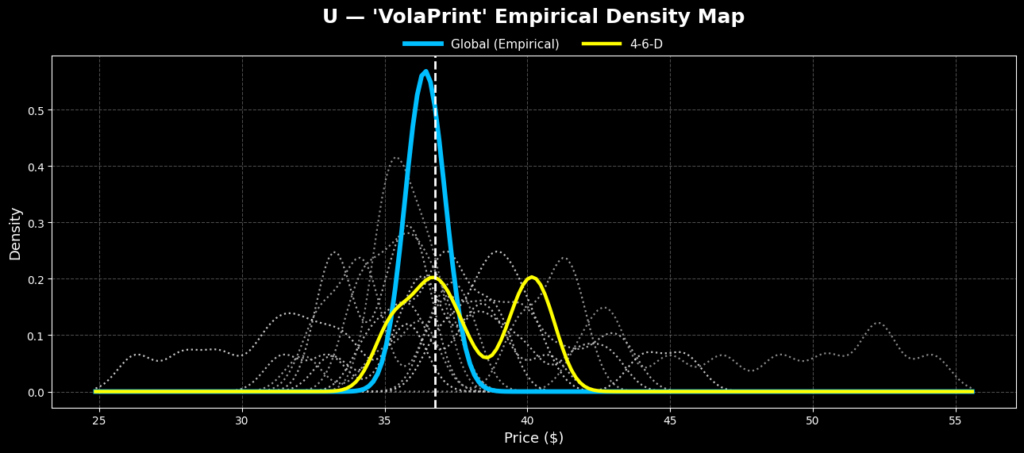

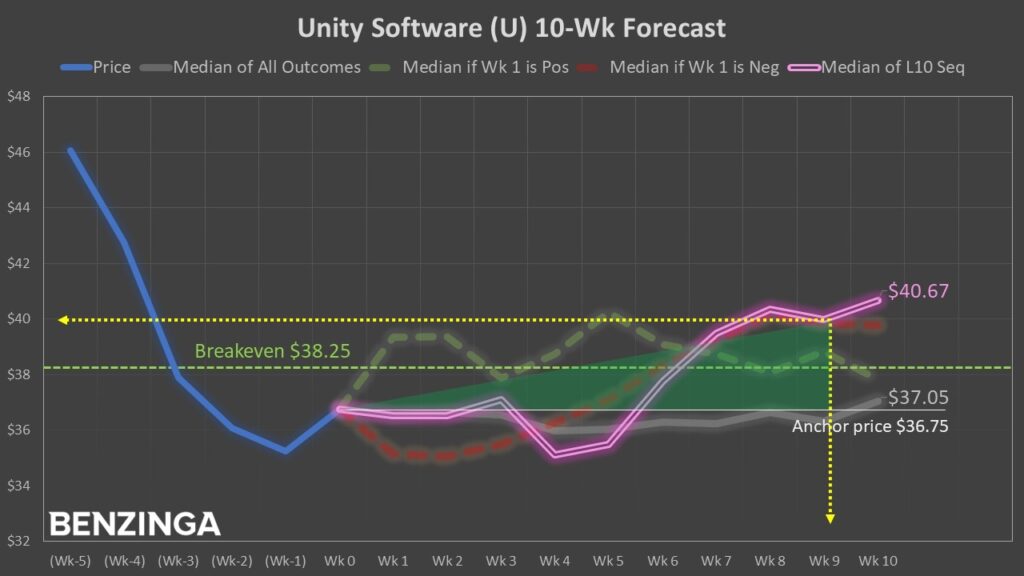

In contrast, the quantitative approach is falsifiable. Using data since its initial public offering, the projected 10-week returns of U stock form a slightly skewed standard distribution, with prices projected to cluster around $36.40 (assuming a starting point or anchor price of $36.75). Also, the exceedance ratio (profitability rate) at the tenth week is calculated to hit 51%, a slightly positive bias.

However, the quant argument is that U stock is not trading at its homeostatic state. Instead, as mentioned earlier, the security lost 20% in the trailing month. More specifically, in the trailing 10 weeks, U has printed a 4-6-D sequence: four up weeks, six down weeks, with an overall downward trajectory.

This sequence isn't important per se. But by tagging this signal and isolating its behavior relative to the parent dataset, we can form what's known as a bimodal distribution of its probabilistic outcomes. As it turns out, under 4-6-D conditions, there are two prominent price density zones: roughly $36.70 and $40.50.

Both density zones are above the price clustering of $36.40 that would be expected under baseline conditions. Even better, the exceedance ratio on the tenth week would be projected to hit 63.2%.

Now, I have to be careful about presenting this idea as an easy trade because it's not. Under 4-6-D conditions, the risk tail of U stock would also extend southward to around $32, below the $35.50 that would be expected under baseline conditions.

Quantitatively, then, the conclusion is as follows: U stock offers more upside opportunity than what you would normally expect but at the cost of a more painful black-swan risk.

Advantaging Market Skepticism

While U stock is a high-risk, high-reward opportunity, the longer-term exceedance ratio is firmly in positive territory. Of course, the power of the quant signal must hold temporally and that's not guaranteed. However, with all the metrics considered, the bullish argument makes more sense than the bearish.

With that in mind, I'm really loving the idea of the 37/40 bull call spread. This trade requires U stock to rise through the second-leg strike price ($40) at expiration. Doing so would trigger the maximum payout of 140%. Further, breakeven lands at $38.25.

The justification for the above trade is simple. As stated earlier, the empirical data under 4-6-D conditions show price clustering above $40. It's possible, then, that the second-leg strike is conservative and even bolder traders may go for $41.

Here's the way I look at it: if market makers are willing to give me a 140% payout at the median cluster, that's too tempting of an idea to simply ignore.

Read More:

Image: Shutterstock

© 2026 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

To add Benzinga News as your preferred source on Google, click here.