If retail sector investors have their sights set on surprise blowout Q2 earnings after recent blowout earnings from one online retailer—yes; that would be Amazon.com, Inc. (NASDAQ:AMZN)— they might be in for a sad and sorry disappointment.

The first full quarter under the coronavirus pandemic—and subsequent quarantine and lockdown—is likely to show up as deep double-digit sales declines for many of the nation’s largest retailers. It may not be a total repeat of Q1—when stores were first closed in an effort to stem the spread of the outbreak, but it still likely won’t be pretty.

Though many retailers have reported improved sales since some stores began reopening in late April and May, many analysts believe that spending could have been more tied to pent-up demand than a reflection of how consumers feel about spending. The earnings results and conference calls might give better insight.

Some analysts see a chunk of Q2’s spending, which happened at a time when hordes of folks were still on temporary furlough or permanent layoff, being tied to the $600 weekly unemployment boost that ended July 31. Also, many consumers received a $1,200 check from the government during the quarter that might have motivated them to spend. The size and scope of any subsequent stimulus (now under debate in Washington) will likely impact spending in the second half of the year.

And then there’s the government’s gross domestic product (GDP) estimate update for the second quarter: a record 34.6% percent nosedive in consumer spending on an annualized basis, and an overall 32.9% GDP drop on an annual pace—marking the economy’s worst showing since 1875, according to recent data by the Bureau of Economic Analysis.

One thing seems relatively certain: When the nation’s largest retailers unleash their earnings in the coming days and weeks, we’ll get an idea of how consumers have been spending their money. Or not.

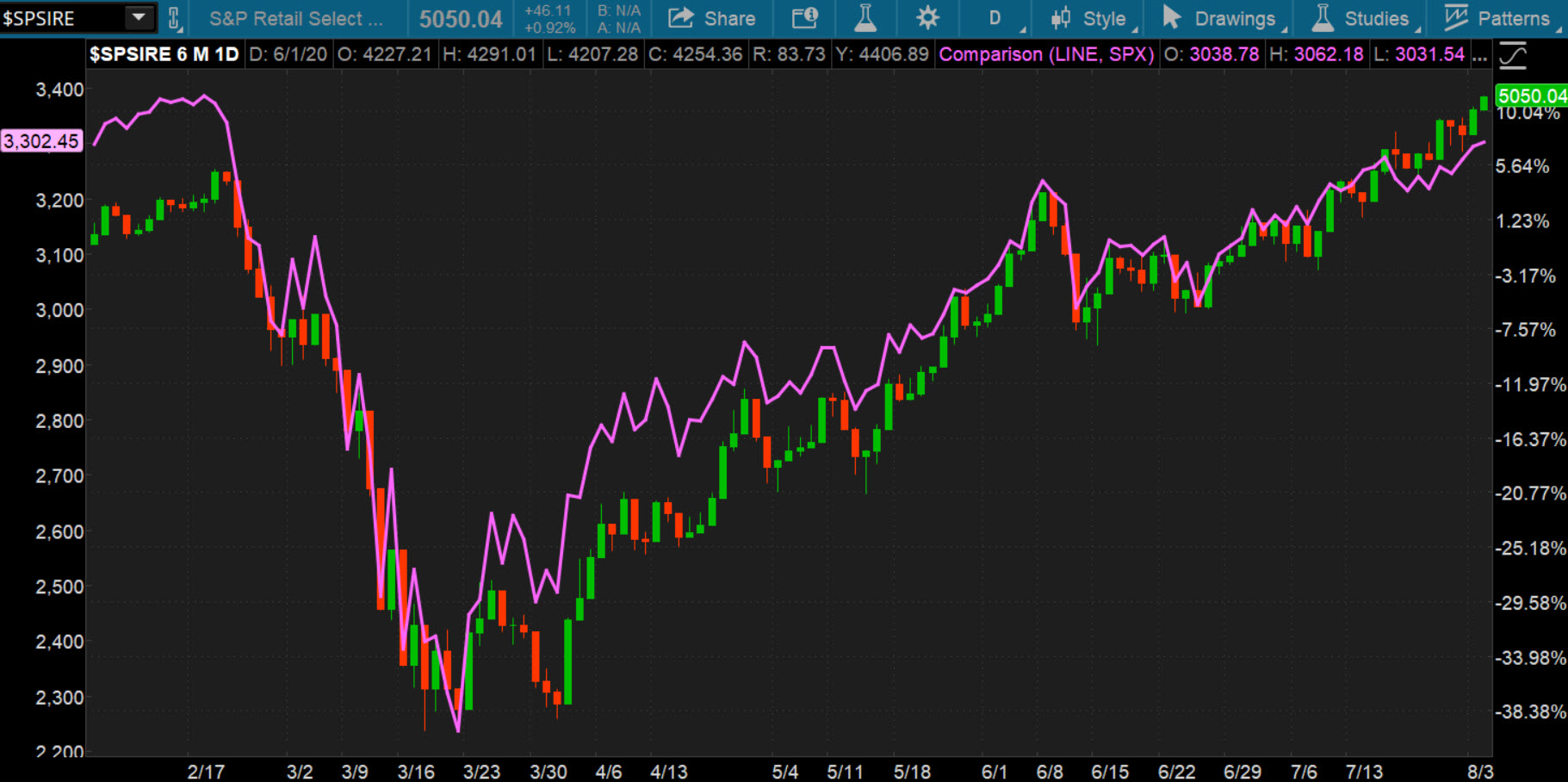

FIGURE 1: RETAIL’S CRUISIN’. Overall the S&P 500 Retail Select Industry Index ($SPSIRE—candlestick) has been moving pretty much in line with the S&P 500 Index (SPX—purple line). In the last few weeks, $SPSIRE has outpaced the SPX. This may seem a bit surprising considering the tough times many retailers are suffering, but it could reflect hopes for more government stimulus. Data source: S&P Dow Jones Indices. Chart source: The thinkorswim® platform from TD Ameritrade. For illustrative purposes only. Past performance does not guarantee future results.

The Retail Reality

FactSet forecasts a 201% drop off in earnings in the textiles, apparel, and luxury goods industries of the consumer discretionary sector. Overall, the sector is expected to report the second-largest year-over-year earnings decline of all 11 sectors in the S&P 500 at minus-116.6%.

“If -116.6% is the actual decline for the quarter, it will mark the largest year-over-year decline in earnings for the consumer discretionary sector since FactSet began tracking this data in Q3 2008,” John Butters, senior earnings analyst, wrote in a recent report.

On the revenue side, Butters projects an 18.9% decline for the quarter, representing the third-largest pullback of the 11 S&P sectors and another “worst” for the sector. The record is a minus-18.4% in the depths of the Great Recession in Q1 2009. Textiles, apparel, and luxury goods are expected to see sales drop 45%, according to FactSet.

It could get worse depending on whether cities and states reissue stay-at-home mandates as COVID-19 cases continue to flow in. Investors might want to keep close tabs on what’s happening across the country as the coronavirus cases climb.

Another thing to watch is pricing. It’s not just about moving units, it’s about the price those units fetch. Will companies have to discount? If retail firms don’t see enough demand occurring, they often have to cut prices. If that happens, it could generally speak to a consumer who’s a little cautious and not willing to pay up for clothing and other items. People who don’t want to pay up for clothing because they’re worried about or have lost their jobs are even less likely to want to pay more for (or even buy) major items like cars and washing machines. Those products are what really drive the consumer economy—which makes up more than two-thirds of the total U.S. economy.

Another Tale of “Two” Sectors

Like Q1, earnings results might tell the essential vs. nonessential tale of consumer spending.

It’s not likely to have a happy ending for the likes of Macy’s Inc (NYSE:M) and J.C. Penney retailers, both of which have reported lackluster sales over the course of the pandemic.

Ditto for casualwear retailers Lululemon (NASDAQ:LULU) and Nike Inc (NYSE:NKE) but analysts mostly expect these two to snap back relatively quickly—even if the pandemic wears on. Apparel and footwear retailer sales have been trounced during the pandemic—who’s buying dress wear these days?—but many analysts believe the double-digit dips in sales at LULU and NKE during Q1 could be more of pandemic-related and operational blips than ongoing trends for casual wear.

NKE has made management and workforce changes as it focuses on direct-to-consumer sales and beefing up its training and exercise apps for at-home athletes. LULU has been doing much of the same on the fitness side, and analysts believe that though its efforts didn’t pan out in Q1, it looks like it might be poised well going forward.

LULU, for example, reported 50% new-customer growth during Q1, which Susquehanna analyst Sam Poser said he expects to see more of. “They have been very good about keeping their customers and developing them, and that bodes well for the future,” he said on Bloomberg TV.

“There’s been an evolving casualization going on for some time that LULU has been capitalizing on,” he said. The pandemic “moves that casualization forward … however, consumers have a very large choice … on where to buy casualwear,” he added, calling out NKE as one alternative.

The Bankruptcy Issue

Like others in the big-box sector, JCP filed for Chapter 11 bankruptcy protection and already has said it will close more than 242 stores or roughly one-third of its stores across the country. Indeed, the quarter was stocked with one major retail bankruptcy after another, including Neiman Marcus, J. Crew, True Religion, and GNC.

The start of Q3 has seen more of the same, with the parents of Lord & Taylor and Men’s Wearhouse stores the most recent to file for bankruptcy protection. The Men’s Wearhouse situation probably reflects what we said above about few people needing dresswear right now with so many still working at home.

M reported some improvement in May and June as customers ventured out to shopping centers and malls again during the early phase of reopening. But Jeff Gennette, M CEO, might have said it best during the company’s Q1 conference call when he told investors and analysts that a heavy cloud of uncertainty still hangs over the sector.

“Initial sales trends as stores reopened were stronger than we modeled with a few encouraging signs,” he said. “In most stores, we saw a steady, modest improvement in sales on a weekly basis. Digital sales remained strong in each market as our stores reopened and our customers were very happy to be back in our stores. Both customers and colleagues have adapted to new health and safety standards.

“So we felt momentum as we work through the second quarter and we’ve seen this in Macy’s, Bloomingdale’s and the Bluemercury brands,” he added. “But I want to remind you that there is still a high degree of uncertainty in the market that causes us to take a conservative approach for the back half of the year.”

He pointed to three issues to keep an eye on: The COVID-19 pandemic is still in “full swing in some parts of the country,” and he anticipated there will be regional closings as consumers are encouraged to stay home. He also reminded investors that most stores are on reduced hours, meaning less opportunity to ring up sales, something nearly all retailers are experiencing.

Though M stores may be open, many of the malls they operate in are closed as are many of the other stores, restaurants, and services, all leading to a downturn in foot traffic. And finally, M’s large urban and flagship stores are opening at a slower pace than others. He attributed that to the dense urban areas in which they’re located which were most affected by the pandemic coupled with “the virtual disappearance of international tourism spending, which we do not expect to recover anytime soon,” Gennette said.

Those are issues that appear to be affecting all retailers as they scramble to reopen—and stay reopened.

Those That Thrived

While the coronavirus pandemic has battered much of the retail industry, there’s a relatively short list of retailers that have not only survived but appear to have prospered as consumers limited their activities and focused more on the homefront and at-home activities to keep them busy.

As in Q1, there will be essential retailers such as Walmart Inc (NYSE:WMT), Target (NYSE:TGT), Costco (NASDAQ:COST), Home Depot (NYSE:HD), and Lowe’s (NYSE:LOW) that may have benefited from the focus on home life during the pandemic.

Analysts said they are mostly expecting another quarter of strong sales out of WMT, TGT, and COST, three magnets for shoppers looking to stock their pantries as well as their fridges, linen closets, and even summer clothes closets.

Home improvement also has largely avoided the pitfalls other retail sectors endured. When you’re locked up in your home for such long periods of time, it’s hard not to notice the leaky faucets, weathered flooring, and outdated paint colors.

And it’s that time of year when the “honey-do” projects may actually get done, especially as consumers working from home are finding time to do them.

“It does seem that people are still going to go ahead and do projects they had in mind because they have the wherewithal to do it, home prices are still going up, and they still have the jobs,” Wedbush Securities’ Seth Basham, managing director of equity research, told Business Insider. “That’s what really has driven the vast majority of the improvement in their sales trends,” he said of HD and LOW.

If there’s a caveat, it might come from the professional side of the business. While many contractors have reported being busy during the first wave of the pandemic—especially as construction was considered an essential service in many parts of the country—it’s unclear what the pipeline might hold.

Many commercial real estate projects have been put on hold, and the same could be happening in major home remodels. What’s more, if the economy spirals further and unemployment stays in these double-digit rates, the housing industry could take a big hit—something investors might want to also keep tabs on.

Investors might want to keep their ears tuned to any insight on what might be ahead in the construction and development industries, both huge feeders to HD and LOW.

With the economy still on such shaky ground, it’s probably a good idea to keep both hands on the wheel as you steer through this earnings period and into the second half.

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Photo by Ashim D’Silva on Unsplash

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.