The catalyst for this post was an article at Hard Assets Investor comparing the Claymore/Clear Global Timber Index (CUT) to the iShares S&P Global Timber & Forestry Index Fund (WOOD). I wrote about CUT for TSCM in 2007 but have not written about WOOD before.

I have written many posts about investing in timber assets one way or another with the inspiration having come from former Harvard Management Company CEO Jack Meyer. There have been other luminary investors also known to invest in the space including Julian Robertson.

The big idea as you may well know is that timber assets tend to offer a steadier return than broad equity indexes and a low correlation to broad equity indexes.

Stocks like Plum Creek Timber (PCL) have long been popular as offering the potential diversification benefit mentioned above along with an above market dividend yield.

Stocks like Plum Creek Timber (PCL) have long been popular as offering the potential diversification benefit mentioned above along with an above market dividend yield.

The correlation of these stocks and ETFs ebbs and flows of course but are not that low. According to ETFreplay.com CUT's correlation to SPY is currently 0.96 and while that site did not seem to know WOOD, the correlation between the ETFs is very high.

Since the inception of WOOD in July 2008 that ETF is down 20% and CUT is down 7% compared to a drop of 18% for the S&P 500. However from that inception date to the low in March 2009 both WOOD and CUT dropped 60% (July 2008-March 2009) versus a 40% drop for the S&P 500.

I believe the drop ties into both the sector makeup of the funds being very heavy in materials stocks (with kind of an industrial twist if you look at some of the companies) which got hit harder than the market and that the nature of the panic in the market was that there were almost no themes or market segments that did what they were "supposed" to do.

Given that cyclical makeup of the ETFs I'm not sure they can offer much in the way of zig zag as the market appears to be rolling over again--and if it is not rolling over now then apply the comment to whenever the next bear market comes.

That there may not be much in the way of diversification benefit does not invalidate the theme or the funds. The need for timber would seem poised to trend higher over the coming years, some of the companies in the funds do indeed own a lot of timberland around the world, some of the stocks do have very attractive yields and offer foreign exposure with almost nothing allocated to big western Europe, especially CUT which is 61% in foreign stocks.

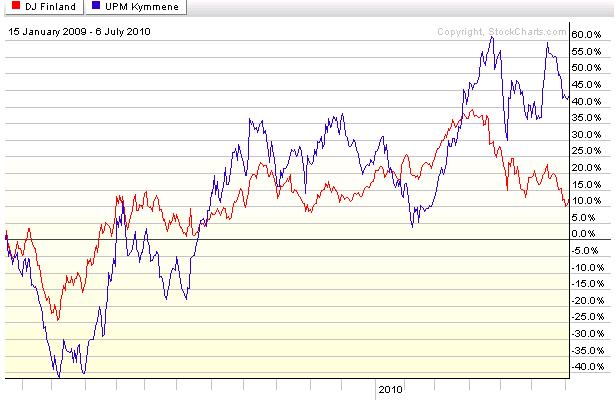

A little more specifically some of the names in the fund could be a starting point for picking stocks to serve as proxies for certain countries. Finland figures prominently in both funds with exposure to UPM Kymmene (UPMKY) and Stora Enso (SEOAY).

A little more specifically some of the names in the fund could be a starting point for picking stocks to serve as proxies for certain countries. Finland figures prominently in both funds with exposure to UPM Kymmene (UPMKY) and Stora Enso (SEOAY).

I believe Finland would benefit in the unlikely event of a breakup of the euro and to a lesser extent if there were to be a dramatic change in the composition of the euro.

Is UPM Kymmene a good company and/or a good proxy? You can decide that for yourself but the bigger picture idea of looking under the hood of an ETF as a starting point for seeking out ways into a country that interests you is a valid approach.

Market News and Data brought to you by Benzinga APIsI have written many posts about investing in timber assets one way or another with the inspiration having come from former Harvard Management Company CEO Jack Meyer. There have been other luminary investors also known to invest in the space including Julian Robertson.

The big idea as you may well know is that timber assets tend to offer a steadier return than broad equity indexes and a low correlation to broad equity indexes.

Stocks like Plum Creek Timber (PCL) have long been popular as offering the potential diversification benefit mentioned above along with an above market dividend yield.

Stocks like Plum Creek Timber (PCL) have long been popular as offering the potential diversification benefit mentioned above along with an above market dividend yield.The correlation of these stocks and ETFs ebbs and flows of course but are not that low. According to ETFreplay.com CUT's correlation to SPY is currently 0.96 and while that site did not seem to know WOOD, the correlation between the ETFs is very high.

Since the inception of WOOD in July 2008 that ETF is down 20% and CUT is down 7% compared to a drop of 18% for the S&P 500. However from that inception date to the low in March 2009 both WOOD and CUT dropped 60% (July 2008-March 2009) versus a 40% drop for the S&P 500.

I believe the drop ties into both the sector makeup of the funds being very heavy in materials stocks (with kind of an industrial twist if you look at some of the companies) which got hit harder than the market and that the nature of the panic in the market was that there were almost no themes or market segments that did what they were "supposed" to do.

Given that cyclical makeup of the ETFs I'm not sure they can offer much in the way of zig zag as the market appears to be rolling over again--and if it is not rolling over now then apply the comment to whenever the next bear market comes.

That there may not be much in the way of diversification benefit does not invalidate the theme or the funds. The need for timber would seem poised to trend higher over the coming years, some of the companies in the funds do indeed own a lot of timberland around the world, some of the stocks do have very attractive yields and offer foreign exposure with almost nothing allocated to big western Europe, especially CUT which is 61% in foreign stocks.

A little more specifically some of the names in the fund could be a starting point for picking stocks to serve as proxies for certain countries. Finland figures prominently in both funds with exposure to UPM Kymmene (UPMKY) and Stora Enso (SEOAY).

A little more specifically some of the names in the fund could be a starting point for picking stocks to serve as proxies for certain countries. Finland figures prominently in both funds with exposure to UPM Kymmene (UPMKY) and Stora Enso (SEOAY).I believe Finland would benefit in the unlikely event of a breakup of the euro and to a lesser extent if there were to be a dramatic change in the composition of the euro.

Is UPM Kymmene a good company and/or a good proxy? You can decide that for yourself but the bigger picture idea of looking under the hood of an ETF as a starting point for seeking out ways into a country that interests you is a valid approach.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Loading...

Posted In: FinancialsSpecialized REIT's

Benzinga simplifies the market for smarter investing

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.

Join Now: Free!

Already a member?Sign in