Year 3, Week 49 Major Position Changes

Cash:

18 long bias

2 short bias:

20 positions (vs 19 last week)

Weekly thoughts

Economic reports

Tuesday

Wednesday

Thursday

Friday

Monday

Tuesday

Wednesday

Thursday

Friday

To see historic weekly fund changes

click here OR the label at the bottom of this entry entitled 'fund positions'.

Cash:

70.6% (v 78.3% last week)

18 long bias

: 27.8% (v 21.1% last week)

2 short bias:

1.5% (v 0.6% last week)

20 positions (vs 19 last week)

Weekly thoughts

------------

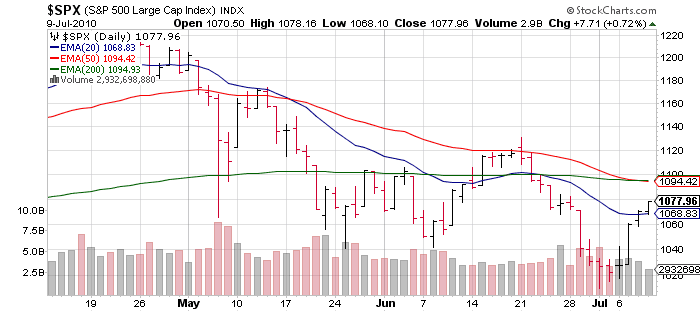

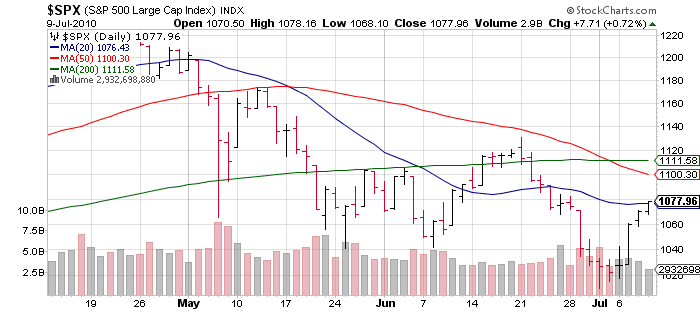

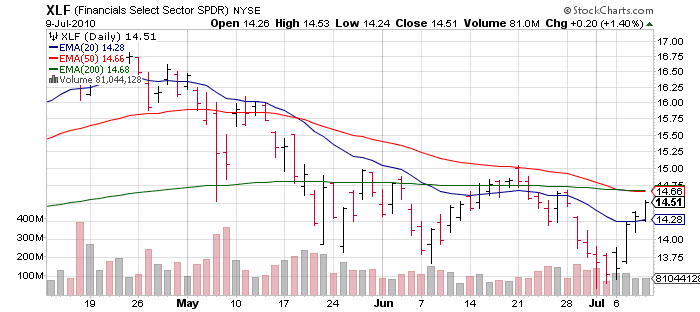

This is a key week for financial company reporting with some big players hitting - XLF is fast approaching key resistance. Make or break it time.

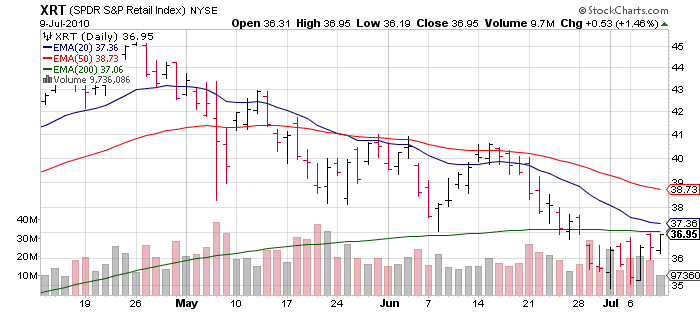

After being *the* darling of the stock market in Q1 2010 as the "playbook for recovery" was utilized by the institutional money, consumer discretionary was dropped like Cleveland in a Lebron James made for TV special. It too sits at a make it or break it area.

Others instruments, we are stroking our virtual chin as we wonder what they are 'saying' (if anything).

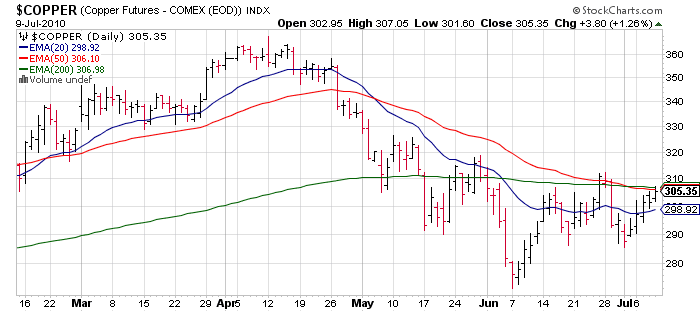

"Doctor" copper - much like the instruments above (remember, we are all one big monolith nowadays) has rebounded from oversold levels and ... (broken record) is at make it or break it areas.

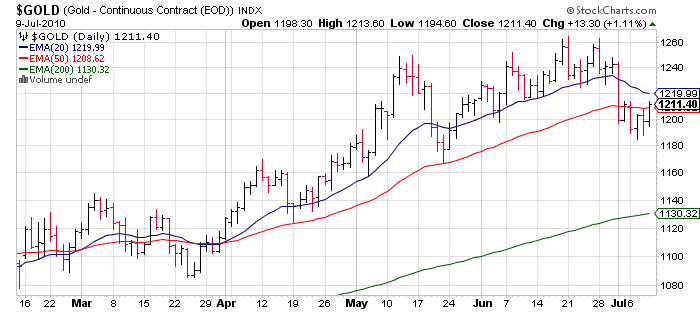

Gold broke down for the first time since March as it 'felt' like a hedge fund blew up - word has it John Paulson suffered $2 Billion of redemptions so maybe he had to do some selling? Who knows. It rebounded late week and (yawn) make it or break it. I still have a sinking feeling about that potential double top formation.

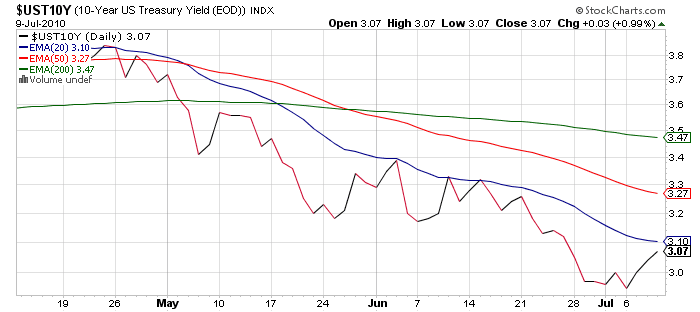

10 year bond? After falling below 3% recently - stirring up fears of deflation and/or a new recession on the horizon, it regained that level late in the week, but thus far is yet another dead cat bounce actor.

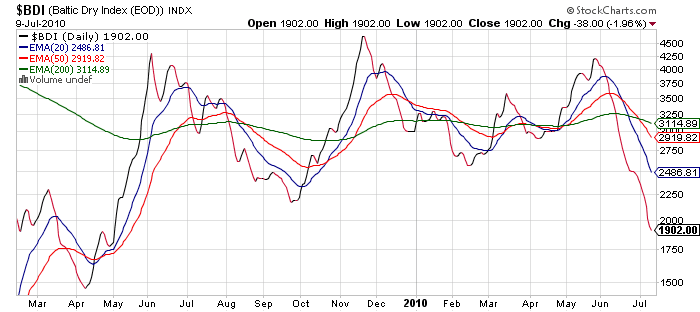

And one for fun - I think I read that the Baltic Dry Index (shipping rates) is down 30 days in a row. Essentially BDI has been taken hostage by China' whims. When they are hungry for commodities BDI runs and we all clap and cheer and sing songs of green shoots. When they pull back, BDI falls and ... well people try not to talk about it because it might upset the bull case. Shhhhh!

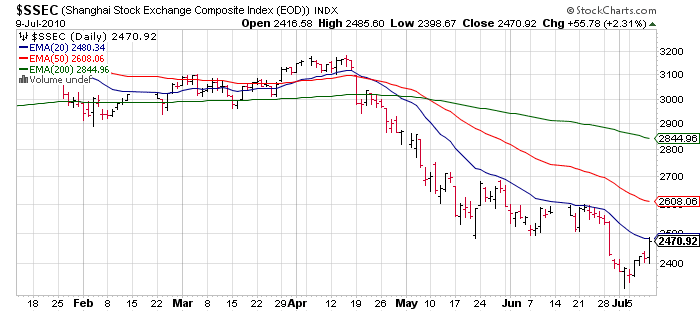

Speaking of which, China has been unable to get out of its own way... so weak the relatively minor 20 day moving average is acting as a noose around the neck At this point the 'sideways action' (while the rest of the world rallied) is not looking so bad in comparison. Another (wait for it) oversold bounce.

Needless to say the (quote-unquote) easy trades are in. Now we have a bevy of items approaching make it or break it levels, within a stock market that has no memory from day to day (bipolar) and ready to react to each major earnings report as if the world is either ending or green shoots are going to take over the world. Should be a lot of "fun" in premarket this week.

-----------------------------------------

Economic reports

pick up this week after a slow one last week. Last week saw even more weaker than expected day (ISM Services being the key) but it shows you the market often does its thing and the reaction to news is almost an afterthought much of the time. Thursday of this week, even excluding the weekly jobless claims, is especially full. However, earnings reports in the premarkets and after the bell will cause as much, if not more, volatility.

Tuesday

- International Trade

Wednesday

- Retail Sales (market will knee jerk to this one), Business Inventories

Thursday

- Producer Price Index, Empire State Mfg, Industrial Production, Philly Fed

Friday

- Consumer Price Index, Consumer Sentiment

Some key earnings reports for the week:

Monday

-

Alcoa (who cares, but as the first company each quarter market is obsessed with it as some sort of tell on the economy) Instead market should care about

CSX (railroad) not for "hitting earnings" but what they see in the economy.

Tuesday

-

Intel: nothing else matters

Wednesday

- market will obsess over

Texas Instruments; for a gauge of the higher end consumer & business consumer I'd interested in

Marriott instead.

Thursday

- JPMorgan will make sure you know it's the alpha male oligarch; however I bet trading is going to be off a bit since Q2 was so volatile and fixed income which has been the bread and butter for a few quarters might be light too. We'll see if expectations were brought down enough. In other news, before Apple reinvented itself,

Google was the thing. As if our entire economy is based on internet searches and how many people in the top 15% can buy higher end computers and gadgets. Again, I'll be more interested in what

JBHunt (trucking) company has to say rather than if "Google beats the whisper number!!!" But JBHunt does not make for interesting financial entertainment TeeVee.

Friday

- big day for our oligarchs aka taxpayer backstopped tools of "free market capitalism"

Bank of America and

Citigroup. The parent of financial infotainment TeeVee, which also has a big financial arm ... oh yeah I guess they still make things some things as well as a side business,

General Electric also speaks.

As always the reaction to the data is more important than the data. Especially with guidance this time around. In the go forward quarters, year over year comparisons are going to start getting much tougher.

------------------------------

Did you make it this far? Gosh you might be an addict to FMMF; support groups forming. I'm in hour 3 of writing this piece - boo yah. All this information handed to you, at no charge. Lucky duckies.

On the

long side:

On the

short side:

© 2026 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

To add Benzinga News as your preferred source on Google, click here.