Year 4, Week 4 Major Position Changes

To see historic weekly fund changes click here OR the label at the bottom of this entry entitled 'fund positions'.

Cash: 71.0% (v 80.2% last week)

20 long bias: 20.7% (v 17.7% last week)

5 short bias: 8.3% (v 2.1% last week)

25 positions (vs 20 last week)

Weekly thought

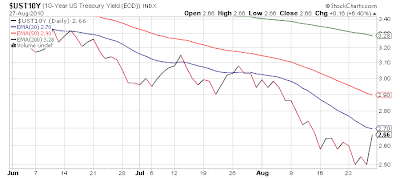

A rally Friday in the face of an Intel warning saved face for U.S. markets . While both the indexes and many individual stocks were oversold, it certainly was a stiking reversal in the action after an early morning selloff, and negative reaction to the first blush to Bernanke's speech. But generally once the rubber band is pulled back too far, it has to snap back - and more than equities the move in bonds was prone to a snap back, and with all computers trained on this relationship, once bonds showed any faint sign of life, the rush into equities was on. So the question from here, since we live in one huge correlated trade, rather than any form of markets nowadays is how far can the bond move go, because equities should move in inverse. Already in 1 session of dramatic reversal, the US 10 year treasury nears resistance.

As for the S&P 500, a cool 25 points was tacked on from the intraday low of S&P 1040, relieving some of the oversold pressure. S&P 1057 held as resistance for much of the day but a late afternoon push through 1060 had buyers rush in (and bears cover ahead of the weekend) taking the index to 1065. There is a small upside gap at 1067 that still needs to be filled, so I'd assume this happens soon. However, bigger picture all we are doing is going back and forth in a wide range, benefiting no one but traders. The current levels of importance remain the same:

1010

1040

1057

1070

1085ish (the 50 day simple moving average which was a key level of support, now resistance)

After ignoring the domestic selloff for a few weeks, the Chinese market finally began to show signs of rolling over again. Their purchasing managers index data Tuesday evening our time, should be a key driver for the week. On the other hand, copper is still holding in well. An interesting divergence.

-----------------------------

Economic data is important this week and then will take a hiatus in the coming weeks as secondary & housing reports take the baton in early to mid September. I would expect gap ups or down on the indexes both Wednesday and Friday mornings as we get PMI reports and the monthly employment data, not to mention Chinese/European industrial data the first day of the month. These are impossible to game - essentially an "earnings report" type of atmosphere but for the entire stock market, not one stock. I do believe there is a chance that private payrolls in America went negative in July; and if not for the birth death model I'd say it is almost guaranteed but with the typical 100K+ of phantom jobs added to this piece of 'art work' who knows what the exact number will be. But let us be clear, if its 50K or 75K that is not even keeping up with population growth so the stagnant economy shows no sign of recovery in labor data. Tuesday morning should also be volatile.

Monday: Personal Income and Outlays (premarket)

Tuesday: Case-Shiller Housing Prices (premarket), Chicago PMI, Consumer Confidence

Wednesday: ISM Manufacturing (consensus 53, down from 55.5 in June), also European mfg indexes and overnight Tuesday China purchasing manager indexes. Construction spending.

Thursday: Weekly claims (premarket), Productivity & Costs (premarket), Factory Orders

Friday: Monthly job reports (consensus -80K including census workers let go), and ISM Services (consensus 53, down from 54.3 in June)

-----------------------------

Portfolio

I am making selective buys here or there when stocks I like finally come in but frankly many of the stock we own are 'generals' who have been mostly teflon during this selloff. [Need to See Pain in these Names - the Generals] I don't really trust a move down to be complete until the generals take at least a day or three of serious pain, and thus far some of these names have not even seen 1 harsh day despite a serious selloff the past 2.5 weeks. Bigger picture, with the indexes below all key moving averages any purchases are still knife catching in general and the building of intermediate term positions remains problematic. It feels like almost everyone in the market right long is just a flipper - trying to catch a turn, get their quick trade, and then get out. Certainly not a great environment for 'investing'. As I added a bit of long exposure (about 3%) I made a trade on the short side once S&P 1070 was broken, but the farther we pulled the rubber band away the more sensible it became to switch to some individual equities on the short side rather than a heavy emphasis on indexes. That helped save the bacon Friday, but now that the rubber band had snapped back to some degree, index positions are more attractive of an option for hedging.

On the long side:

On the short side:

Market News and Data brought to you by Benzinga APIsTo see historic weekly fund changes click here OR the label at the bottom of this entry entitled 'fund positions'.

Cash: 71.0% (v 80.2% last week)

20 long bias: 20.7% (v 17.7% last week)

5 short bias: 8.3% (v 2.1% last week)

25 positions (vs 20 last week)

Weekly thought

A rally Friday in the face of an Intel warning saved face for U.S. markets . While both the indexes and many individual stocks were oversold, it certainly was a stiking reversal in the action after an early morning selloff, and negative reaction to the first blush to Bernanke's speech. But generally once the rubber band is pulled back too far, it has to snap back - and more than equities the move in bonds was prone to a snap back, and with all computers trained on this relationship, once bonds showed any faint sign of life, the rush into equities was on. So the question from here, since we live in one huge correlated trade, rather than any form of markets nowadays is how far can the bond move go, because equities should move in inverse. Already in 1 session of dramatic reversal, the US 10 year treasury nears resistance.

As for the S&P 500, a cool 25 points was tacked on from the intraday low of S&P 1040, relieving some of the oversold pressure. S&P 1057 held as resistance for much of the day but a late afternoon push through 1060 had buyers rush in (and bears cover ahead of the weekend) taking the index to 1065. There is a small upside gap at 1067 that still needs to be filled, so I'd assume this happens soon. However, bigger picture all we are doing is going back and forth in a wide range, benefiting no one but traders. The current levels of importance remain the same:

1010

1040

1057

1070

1085ish (the 50 day simple moving average which was a key level of support, now resistance)

After ignoring the domestic selloff for a few weeks, the Chinese market finally began to show signs of rolling over again. Their purchasing managers index data Tuesday evening our time, should be a key driver for the week. On the other hand, copper is still holding in well. An interesting divergence.

-----------------------------

Economic data is important this week and then will take a hiatus in the coming weeks as secondary & housing reports take the baton in early to mid September. I would expect gap ups or down on the indexes both Wednesday and Friday mornings as we get PMI reports and the monthly employment data, not to mention Chinese/European industrial data the first day of the month. These are impossible to game - essentially an "earnings report" type of atmosphere but for the entire stock market, not one stock. I do believe there is a chance that private payrolls in America went negative in July; and if not for the birth death model I'd say it is almost guaranteed but with the typical 100K+ of phantom jobs added to this piece of 'art work' who knows what the exact number will be. But let us be clear, if its 50K or 75K that is not even keeping up with population growth so the stagnant economy shows no sign of recovery in labor data. Tuesday morning should also be volatile.

Monday: Personal Income and Outlays (premarket)

Tuesday: Case-Shiller Housing Prices (premarket), Chicago PMI, Consumer Confidence

Wednesday: ISM Manufacturing (consensus 53, down from 55.5 in June), also European mfg indexes and overnight Tuesday China purchasing manager indexes. Construction spending.

Thursday: Weekly claims (premarket), Productivity & Costs (premarket), Factory Orders

Friday: Monthly job reports (consensus -80K including census workers let go), and ISM Services (consensus 53, down from 54.3 in June)

-----------------------------

Portfolio

I am making selective buys here or there when stocks I like finally come in but frankly many of the stock we own are 'generals' who have been mostly teflon during this selloff. [Need to See Pain in these Names - the Generals] I don't really trust a move down to be complete until the generals take at least a day or three of serious pain, and thus far some of these names have not even seen 1 harsh day despite a serious selloff the past 2.5 weeks. Bigger picture, with the indexes below all key moving averages any purchases are still knife catching in general and the building of intermediate term positions remains problematic. It feels like almost everyone in the market right long is just a flipper - trying to catch a turn, get their quick trade, and then get out. Certainly not a great environment for 'investing'. As I added a bit of long exposure (about 3%) I made a trade on the short side once S&P 1070 was broken, but the farther we pulled the rubber band away the more sensible it became to switch to some individual equities on the short side rather than a heavy emphasis on indexes. That helped save the bacon Friday, but now that the rubber band had snapped back to some degree, index positions are more attractive of an option for hedging.

On the long side:

- Tuesday as the market continued to selloff, I began to rebuild a position in auto supplier BorgWarner (BWA) which had been sold off for good profits. The stock came back down to the 50 day moving average, allowing us a sensible place to purchase.

- Polypore International (PPO) similarly fell back down to the 50 day moving average, letting us have a chance to begin to rebuild a position we had sold higher to lock in profits.

- Once the S&P 500 fell to 1056, I tried some index plays (TNA/BGU) long hoping for a quick oversold bounce - when this did not happen I quickly sold out for a small loss.

- Wednesday, I started another auto supplier position - one of the most impressive earning reports of the previous period, Magna International (MGA) as it fell back to near its 50 day moving average.

On the short side:

- As I tried the previous week (unsuccessfully) once S&P 1070 broke Monday, I put some index short positions on (TNA/BGU) with a target of S&P 1056. This was all based on Fibonacci levels - a move from the 50% retracement to 61.8%. It worked to perfection as I covered most the next day in the mid 1050s. I kept some very small positions as placeholders.

- Wednesday I covered a short in Global Payments (GPN) for a nearly useless 1.5% gain. This was supposed to be one of my hedges for a market selloff; the selloff came but this specific stock did not give up much of the ghost.

- Thursday, with the market quite extended to the downside I decided to focus on individual stocks with poor charts - which led me to a basket of Toll Brothers (TOL), Burger King (BKC), and Symantec (SYMC) - utilizing a 7.5% exposure in total.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Loading...

Posted In: Auto Parts & EquipmentConsumer DiscretionaryData Processing & Outsourced ServicesElectrical Components & EquipmentHomebuildingIndustrialsInformation TechnologyRestaurantsSystems Software

Benzinga simplifies the market for smarter investing

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.

Join Now: Free!

Already a member?Sign in