On the positive side the world has continued past 6 PM Saturday. On the negative, there is a lot of red worldwide U.S. investors are waking up to this Monday. There are a bevy of issues on the plate from a slowdown in Chinese manufacturing (which was seen as a 'positive' the past few months as it indicated a soft landing) to European sovereign debt issues (which the market only seems to care about at certain moments) to the weakening euro / stronger dollar. It appears at this point, the warning signs from copper [May 9, 2011: Doctor Copper Breaks 200 Day Moving Average], defensive sectors [May 17, 2011: Two Recent Bull Markets - Consumer Non Discretionary and Healthcare], and the 30 year bond (now at year lows in yield) a few weeks back were fairly prescient, even as the S&P 500 stubbornly had held in between S&P 1330-1340.

The intraday low of 1320 will definitely be in play this morning, and that gap in the 1310s from mid April has a chance of finally being filled.

----------------------

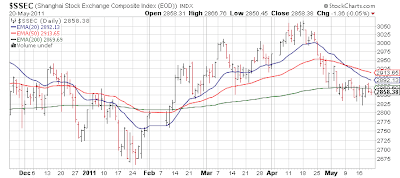

China's market has given back all of this year's gains as it suffered a 2.9% loss to 2774

(chart below is one day delayed)

The main manufacturing gauge used by insiders - the dual Purchasing Managers Indexes (one private, one from government) came in weak-ish in the preliminary HSBC report. This is kind of a catch 22 situation because many months of late people have been applauding a slowing manufacturing figure as they reasoned China could deal with inflation via the soft landing approach. Today however, they seem to be taking more of a hand wringing approach. Always fascinating to see how the same data means nothing one month, and affects the market so severely the next. In theory today's data should be 'positive' as long as China has not overdone its slowing as it means the country is closer to the end of its tightening policy.

Via Bloomberg:

Meanwhile over in Europe, a very expected trouncing by the Socialist Party in Spain, a debt downgrade in Italy, a slowdown in German manufacturing and overall weakness in the euro - down over 1% (leading to dollar strength and per HAL9000 weakness in asset prices, priced in dollars) all are weighing. The major European indexes are generally down in the 1.5%-2.0% range.

Via Reuters:

Also via Reuters:

These are still very healthy numbers, but with the other issues in the region today - helping to cause pain.

Market News and Data brought to you by Benzinga APIsThe intraday low of 1320 will definitely be in play this morning, and that gap in the 1310s from mid April has a chance of finally being filled.

----------------------

China's market has given back all of this year's gains as it suffered a 2.9% loss to 2774

(chart below is one day delayed)

The main manufacturing gauge used by insiders - the dual Purchasing Managers Indexes (one private, one from government) came in weak-ish in the preliminary HSBC report. This is kind of a catch 22 situation because many months of late people have been applauding a slowing manufacturing figure as they reasoned China could deal with inflation via the soft landing approach. Today however, they seem to be taking more of a hand wringing approach. Always fascinating to see how the same data means nothing one month, and affects the market so severely the next. In theory today's data should be 'positive' as long as China has not overdone its slowing as it means the country is closer to the end of its tightening policy.

Via Bloomberg:

- A Chinese manufacturing index fell to its lowest level in 10 months, adding to signs that economic growth is cooling after the government raised interest rates and curbed lending to rein in inflation. The preliminary purchasing managers' index compiled by HSBC Holdings Plc and Markit Economics dropped to 51.1 in May from a final reading of 51.8 in April. A number above 50 indicates expansion.

- Stocks in China extended declines after the report, with the benchmark index dropping to its lowest since February, on concern the government's measures to tame inflation will damp growth and corporate earnings. Vice Premier Wang Qishan reiterated this month that the government's top priority is to control price increases.

- The data “confirms growth is slowing, which will likely dampen price pressures and limit scope for monetary tightening,” said Dariusz Kowalczyk, senior economist at Credit Agricole CIB in Hong Kong.

- New export orders contracted in May and stocks of purchases and finished goods fell at a faster rate, HSBC said. An output gauge declined to a 10-month low, although it remained above the 50 level that divides expansion from contraction, the bank said.

- Industrial output growth weakened last month and the worst power shortage in seven years is hurting production at some factories as provinces start curtailing electricity supplies.

- “Cooling growth is not all bad news as it also helps to tame inflation,” Qu said. The preliminary index's input price gauge was at its lowest level since August 2010 and growth in output prices eased to 54.6 in May from 55.2 in April, he said.

- HSBC's preliminary manufacturing index, called the Flash PMI, is based on 85 percent to 90 percent of the total responses to its monthly purchasing managers' survey sent to executives in more than 400 manufacturing companies.

Meanwhile over in Europe, a very expected trouncing by the Socialist Party in Spain, a debt downgrade in Italy, a slowdown in German manufacturing and overall weakness in the euro - down over 1% (leading to dollar strength and per HAL9000 weakness in asset prices, priced in dollars) all are weighing. The major European indexes are generally down in the 1.5%-2.0% range.

Via Reuters:

- Following Fitch Ratings cut of Greece's debt ratings by three notches on Friday, pushing the country's debt deeper into junk status, rival Standard & Poor's cut its outlook for Italy to "negative" from "stable" on Saturday.

- Spanish voters added to the angst, becoming the latest electorate to punish sitting European governments for the current economic climate. The ruling Socialists were hit by stinging losses in local elections and now face a balancing act between voter anger over sky-high unemployment and investor demands for strict austerity measures.

- The euro fell to a record low against the generally safe-haven Swiss franc.

- Worries about some form of debt restructuring by Greece was a key element of the sell off. If Greece were to restructure its debt that could prompt Ireland and Portugal to follow with debt restructuring of their own.

Also via Reuters:

- The German private sector's growth slowed to its lowest rate since October in May, at 56.4. The key survey showed in a fresh sign Europe's largest economy is cooling from a surge in the first quarter. A flash composite purchasing managers index (PMI) of the manufacturing and services sector by research firm Markit fell to 56.4 from 59.2 in April.

- A separate PMI index tracking the manufacturing sector fell to 58.2, its weakest level since November last year, while a measure of the services sector dropped to 54.9, its lowest point since September.

- Both readings were below economists' expectations given in a Reuters poll, which had put consensus forecasts at 61.0 for the manufacturing sector and 57.0 for services. New orders growth also dropped for both sectors.

These are still very healthy numbers, but with the other issues in the region today - helping to cause pain.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Loading...

Posted In: FinancialsThrifts & Mortgage Finance

Benzinga simplifies the market for smarter investing

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.

Join Now: Free!

Already a member?Sign in