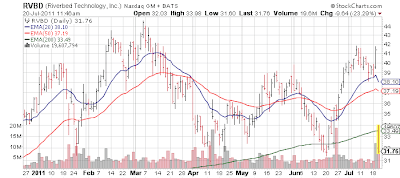

As mentioned late yesterday, Riverbed Technology (RVBD) was going to take the boot today - something that usually happens once every 4-6 quarters with this name. Analysts have a mixed opinion on whether to buy this dip. Obviously the technical makeup is damaged, but we can see this area of $31ish has generally held during 2011. So if it holds again in the coming days this could be an attractice long term entry...

The bullish crowd:

And the not so much group:

Market News and Data brought to you by Benzinga APIs

The bullish crowd:

- Scott Zeller, Needham & Co.: Reiterates a Buy rating while lowering his price target to $41 from $48. “Our sense from field discussions is that demand for software is unchanged in EMEA, and we attribute this miss to “company specific” issues. The acquisitions of Zeus Technology and Aptimize are complementary as they offer capabilities in Application Delivery Control (ADC) and Web Content Optimization (WCO), and are EPS neutral then accretive in CY12. We don't view these acquisitions as “buying revenue” as some might suspect; our view from the field is that WAN acceleration and data center refresh remain strong secular trends (e.g. US +50% y/y in JuneQ).” Zeller cut this year's estimate to $725.9 million in revenue and 87 cents EPS, from a prior $737.6 million and 90 cents, and cut 2012′s estimate to $900 million and $1.16 per share from a prior $912 million and $1.17.

- Daniel Ives, FBR Capital Markets: Reiterates an Outperform rating and a $43 price target. “While the weakness in the quarter is confined to mostly macro headwinds in the EMEA region, which resulted in some deals slipping into 2H, we believe this is more of an air pocket quarter, which should smooth itself out during the next few quarters.” Ives raised his 2011 estimate to $725.9 million and 89 cents per share in profit, from a prior $722.3 million and 88 cents to account for the addition of revenue from the two acquisitions. His estimate for 2012 goes to $906 million and $1.17, from a prior $887 million and $1.14, again, to account for acquisitionsRyan Hutchinson, Lazard Capital Markets: Reiterates a Buy rating, while cutting his price target to $40 from $45. “Riverbed missed its revenue guidance for the first time since 2Q09 amid broad expectations, ours included, for another strong beat and raise quarter. We get the sense that deeper execution problems have not been anticipated […] But strong fundamentals underpinning our positive view are unchanged. The stock will face an uphill battle against sentiment for the time being.” Mansky cut his 2011 estimate to $720 million in revenue and 89 cents EPS from a prior $738 million and 95 cents.

- Paul Mansky, Canaccord Genuity: Reiterates a Buy rating and a $44 price target. “Although less crisp than we'd prefer, European organizational changes have been broadly known and are a “fixable” issue in our view given the company's demonstrated product/technology lead – evidenced by continued strong growth in more established domestic markets.” Mansky actually raised his 2011 revenue estimate to $721.7 million from a prior $720 million, while sticking with 89 cents in EPS

- Michael Genovese, MKM Partners: Reiterates a Buy rating and lowers his price target to $40 from $43. “Weviewthepullback in the stock as overdone and recommend buying on what could be temporary weakness.” Genovese cut his 2011 estimates to $730 million and 88 cents EPS from a prior $741 million and 94 cents.

And the not so much group:

- Mark Sue, RBC Capital Markets: Reiterates a Sector Perform rating and cuts his price target to $33 from $35. “We don't think Riverbed is losing share and its products provide a strong ROI case. Nevertheless, we do think the sales execution changes may take more than several quarters to fix and, with Federal to increase sharply as a percentage of revenues in 3Q, we're waiting for an investment horizon when the linearity improves.” Sue cut his 2011 estimate to $727.9 million in revenue and 86 cents EPS from a prior $733.6 million and 91 cents. He also cut his 2012 view to $896 million and $1.15 from a prior $942 million and $1.25.

- Ittai Kidron, Oppenheimer & Co.: Reiterates a “Perform” rating. “. While we believe Riverbed is well positioned long term, the company faces multiple headwinds near term including tough macro trends in Europe, uncertain government spending and dilution due to the acquisitions. Thus, we remain on the sidelines until the growth story takes shape.” Kidron raised his 2011 revenue outlook to $724.6 million from a prior $716 million, while cutting his EPS estimate to 88 cents from 90 cents.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Loading...

Benzinga simplifies the market for smarter investing

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.

Join Now: Free!

Already a member?Sign in