Over the past half century, gold and silver prices have shown a strong positive correlation. Their correlation has been especially high during the past 18 years (Figure 1).

Figure 1: Gold and silver typically show a strong, positive correlation

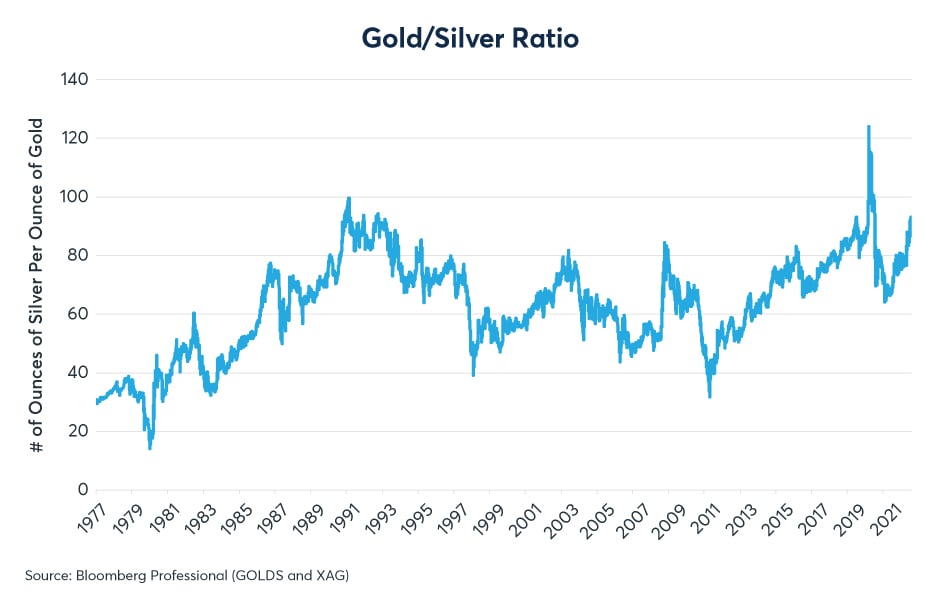

While gold and silver have a strong positive correlation, the ratio of their prices has ranged widely, from one ounce of gold buying as few as 30 ounces of silver in 2011 to as many as 120 ounces of silver in 2020 (Figure 2). In the early stages of the pandemic, silver snapped back, jumping from 120 ounces of silver per ounce of gold to as few as 65. However, in recent months the ratio has begun to slide again: currently one ounce of gold buys over 90 ounces of silver.

Scan the above QR code for more expert analysis of market events and trends driving opportunities today!

Figure 2: The Gold-Silver ratio has ranged widely over the past several decades

What is behind the sharp movements in the price of silver relative to gold? There are three factors:

- Differences in the end uses of silver and gold

- The decline in conventional photography, and the energy transition

- Fluctuations in Chinese demand.

Mirror, mirror on the wall, which is the most precious metal of all?

Although gold and silver are both classified as precious metals, gold has the edge in the sense that it has relative few industrials uses. Last year, 12% of gold was used for some sort of industrial application (including dentistry) compared to 60% that went into making jewellery. The remaining 28% was stored for investment purposes (Figure 3).

Figure 3: Gold is used primarily for jewellery and for investments

By contrast, silver is used primarily for industrial purposes. In 2021, approximately 29% of silver was used to create jewellery and silverware, 23% went into electronics, 12% into solar panels and 24% for other industrial uses (Figure 4). As such, investors tend to treat silver as a hybrid precious- industrial metal, one that follows gold prices on a day-to-day basis but also with long periods of over and underperformance against the yellow metal. Historically, silver often outperformed gold during periods of strong economic expansion during which industrial economies boomed, and tended to underperform gold during periods of economic stress.

Figure 4: Silver is primarily used for industrial applications, batteries & solar panels

The Decline of Conventional Photography and the Energy Transition

From the late 1990s to 2020, silver tended to underperform gold except for the period immediately after the global financial crisis due largely to one factor: the decline of traditional photography. In 1999, 267.7 million ounces of silver were used to develop photographs. By 2021, that number had fallen by 83% to 46.5 million. The rise of digital cameras essentially erased about 20% of silver use within two decades.

While the decline of traditional photography hurt silver demand, other uses have emerged, with the energy transition being the biggest among them. In 2021, 114 million troy ounces were used to create solar panels, which were essentially non-existent about 15 years ago. Moreover, silver demand for use in batteries and electronics has doubled since the end of the 1990s. Silver’s growing use in the energy transition may explain why it’s price has gained on gold in the past few years.

Chinese Growth May Determine Short-Term Fluctuations in the Gold-Silver Ratio

Short-term changes in the gold-silver ratio appear to follow the pace of growth in China’s industrial sector. We use the Li Keqiang Index, a measure that tracks bank loans, rail freight volumes and electricity production, as a proxy for Chinese industrial growth. The index shows exceptionally strong positive correlations with the prices of many commodities one-year forward. While silver is not among the most highly correlated with the index from 2005 to 2021, a change in the pace of growth as measured by the index still showed a +0.37 correlation with the price of silver, less than industrial metals like aluminum and copper, but higher than gold. Among the major commodities, gold is the only one to show a negative (albeit slightly) correlation with Chinese growth (Figure 5).

Figure 5: Silver is a quasi-industrial metals judging from its correlation with Chinese growth

Silver prices rose sharply from 2005 to 2007 following a period of strong growth in China. They then fell sharply in 2008 as China’s economy slowed a great deal during the early stages of the U.S. sub-prime crisis. Starting in 2009 Chinese growth surged as China launched a massive stimulus program that took the growth rate of its industrial sector up to 27% year on year. Silver prices soared in the wake of this extraordinary Chinese boom, eventually rising towards $50 per ounce in 2011. By this time, however, China’s economy had begun to slow sharply and silver prices fell with it. Silver’s extraordinary rebound versus gold in 2020 and 2021 may relate to the rebound in growth that China experienced in late 2020 and early 2021 as they were the first nation to emerge from pandemic lockdowns. However, China’s growth has slowed considerably this year and that might explain why silver has underperformed gold in recent months (Figure 6).

Figure 6: Silver prices tend to follow Chinese growth with a considerable lag

China’s economy appears to be weakened by a sharp contraction in the property sector. Housing construction has fallen by more than a third year on year. China’s debt levels remain relatively high and the high-yield bond market has sold off sharply. These factors may pose considerable downside risks for silver but aren’t necessarily bearish for gold.

There are also upside risks for China’s economy: the government has proposed a $200 billion stimulus plan and a $175 billion mortgage relief plan. The People’s Bank of China has been easing monetary policy even as many other central banks raise interest rates. If Chinese fiscal and monetary stimulus prove to be sufficiently strong to overcome the weakness in the housing sector, that might remove some of the recent downdraft on silver.

This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.