Ross Stores ROST reported better-than-expected third-quarter EPS results on Thursday.

Ross Stores reported quarterly earnings of $1.48 per share which beat the analyst consensus estimate of $1.40 per share. The company reported quarterly sales of $5.07 billion which missed the analyst consensus estimate of $5.15 billion.

Barbara Rentler, Chief Executive Officer, commented, “We are disappointed with our third quarter sales results as business slowed from the solid gains we reported in the first half of 2024. Although our low-to-moderate income customers continue to face persistently high costs on necessities pressuring their discretionary spending, we believe we should have better executed some of our merchandising initiatives. In addition, a combination of severe weather during the quarter from Hurricanes Helene and Milton, along with unseasonably warm temperatures, also negatively impacted our results.”

The company said it sees FY25 earnings of $6.10 to $6.17 per share.

Ross Stores shares gained 2.7% to trade at $146.80 on Friday.

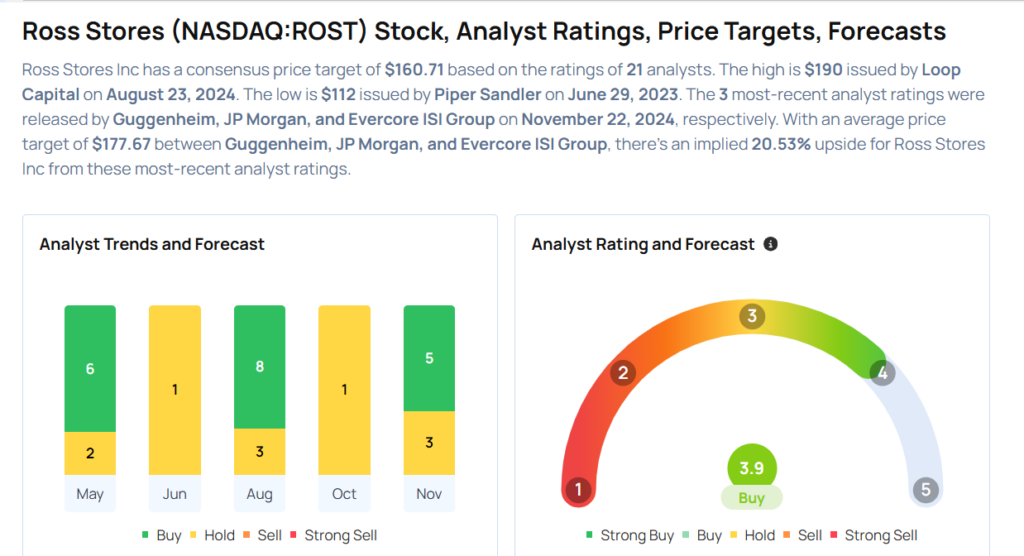

These analysts made changes to their price targets on Ross Stores following earnings announcement.

- Evercore ISI Group analyst Michael Binetti maintained Ross Stores with an Outperform and raised the price target from $170 to $180.

- JP Morgan analyst Matthew Boss maintained the stock with an Overweight rating and boosted the price target from $171 to $173.

- Telsey Advisory Group analyst Dana Telsey maintained Ross Stores with a Market Perform and maintained a $175 price target.

- Guggenheim analyst Robert Drbul reiterated Ross Stores with a Buy and maintained a $180 price target.

Considering buying ROST stock? Here’s what analysts think:

Read This Next:

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

date | ticker | name | Price Target | Upside/Downside | Recommendation | Firm |

|---|

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.