Zinger Key Points

- AMD named top 2025 pick for CPU/GPU momentum, AI edge growth.

- Micron praised for HBM dominance, driving AI and memory cycles.

- Get 5 stock picks identified before their biggest breakouts, identified by the same system that spotted Insmed, Sprouts, and Uber before their 20%+ gains.

Rosenblatt polled its analysts, including Steve Frankel, gathering their top picks for the first half of 2025. The stocks reflect key themes across its research universe, including the Age of Artificial Intelligence and the build-out of next-generation broadband.

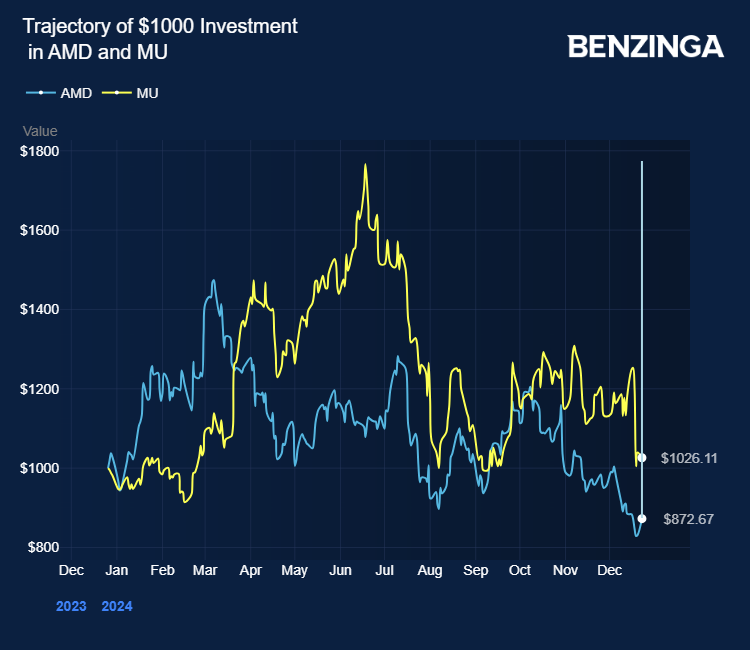

Steve Frankel maintained a Buy rating on Advanced Micro Devices, Inc AMD with a price target of $250.

Also Read: Nvidia Secures EU Approval For Run:ai Deal, US Probes China Export Breach

AMD is one of Rosenblatt’s top picks for the first half of 2025 on momentum in CPU and GPU share gains into 2025 and a broader non-AI recovery exiting 2025.

The difference entering 2025 is that the Street acknowledges this dynamic, which has legs for double-digit market share in GPU compute and AI inference at the edge, being a secular opportunity on Xilinx incumbency and chiplet prowess.

AMD’s EPYC processors will likely continue increasing the company’s revenue share in server and Data Center CPUs as the business proposition is significant, the analyst said.

AMD’s MI350 in 2025 and MI400 in 2026 GPUs will drive additional revenues and increased market share on hyperscale adoption, chiplet scale, and AI moving to the edge, he added.

The price target reflects a 25-times P/E multiple to Frankel’s $10.00 fiscal 2026 adjusted EPS. This multiple is in line with the analyst’s AI compute group average of 25 times.

Frankel reiterated a Buy rating on Micron Technology, Inc MU with a price target of $250.

Micron is one of Rosenblatt’s top picks for the first half of 2025, as he liked the big opportunity for DRAM content deployment in AI platforms going forward.

In particular, the analyst liked Micron’s HBM opportunity, where the trade ratios are 3-to-1 to DDR5 and moving to 4-to-1 with the move to HBM4, a structural shift Frankel did not witness in any other memory cycle.

Industry HBM supply continues to be an issue to watch as supply does not catch up to demand well into calendar 2025.

For Micron, Frankel’s viewpoint on HBM is more related to the overall implications of DRAM bit supply, with HBM3E garnering a 3-to-1 trade ratio and HBM4 a 4-to-1 trade ratio, creating a favorable supply and demand dynamic.

Frankel noted Micron as an HBM share gainer in HBM3E and HBM4 varietals and as the segment moves from 8-Hi to 12-Hi and 16-Hi configurations, where power efficiency (a Micron structural advantage) becomes increasingly important.

Frankel found using P/E to value Micron reasonable, given its proven consistent profitability through cross-memory cycles, aggressive share buybacks, and a cycle driven by AI workload dynamics correlating to DRAM content. The price target reflects a mid-teens P/E multiple on the analyst’s $18 fiscal 2026 adjusted EPS.

Price Actions: At last check on Monday, AMD stock was up 4.70% at $124.82. MU is down 0.78%.

Also Read:

Photo via Shutterstock

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

date | ticker | name | Price Target | Upside/Downside | Recommendation | Firm |

|---|

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.