Zinger Key Points

- Broader economic fears have cut down Salesforce’s market value, presenting a contrarian opportunity.

- Unusual options activity suggests that the smart money is moving into CRM stock.

- Pelosi’s latest AI pick skyrocketed 169% in just one month. Click here to discover the next stock our government trade tracker is spotlighting—before it takes off.

Thanks to rising recession fears exacerbated by multiple trade wars. Investors have turned to alternative avenues to protect their wealth, from purchasing gold to bidding up real estate investment trusts (REITs). However, the smart money has an even bolder idea: rotate back into heavily deflated technology firms such as cloud-based software giant Salesforce Inc CRM.

To be completely upfront, the idea of betting on Salesforce’s stock is a contrarian and therefore risky one. Aside from the tariffs that could impose macroeconomic pressures against Salesforce's primary revenue drivers, the company didn't do itself any favors when it released its fourth-quarter earnings results late last month.

Headline figures came in mixed, with the highlight being earnings of $2.78 per share, beating the consensus estimate of $2.61. Unfortunately, revenue in the quarter landed at $9.99 billion, missing the consensus view of $10.03 billion (though it was an improvement of nearly $9.3 billion from the same quarter last year).

See Also: US Home Sales Jump In February, Median Price Nears $400,000

Still, the real story at the time was management's guidance for fiscal year 2026 revenue, which ranges from $40.5 billion to $40.9 billion. In contrast, analysts were expecting revenue to reach $41.375 billion. Subsequently, Salesforce suffered conspicuous volatility.

Recently, though, a floor appears to have developed around the $270 level — and the show support may have fundamental justification. Last week, Salesforce committed to invest $1 billion in Singapore's artificial intelligence sector, an effort to promote the adoption of the company's AI product Agentforce.

Further, analysts are generally optimistic about Salesforce stock, rating the equity a consensus Buy. Wedbush analyst Daniel Ives in particular remarked that while the "geopolitical poker" game has caused some anxieties, the expert isn't hitting the panic button. Specifically, Ives named Salesforce as one of the potential winners of the so-called AI Revolution.

Smart Money Senses An Opportunity

Participating in the equities market can be a humbling experience, in large part because the influence of opinions is grossly uneven. While retail investors may think a certain way, ultimately, money talks. Therefore, when institutional players — the entities that actually matter — dig into a particular enterprise or asset, it's always worth paying attention.

During the midweek session, Benzinga's options scanner identified generally bullish activity. In terms of dollar volume, the most optimistic transaction was for sold (or written) $240 puts with an expiration date of Oct. 17, 2025. Essentially, the trader(s) underwrote the risk that Salesforce share prices won't drop materially below $240 by expiration. For the risk, they are receiving the premium (bid) of $11.40 or $1,140 per every 100 shares represented by one option contract.

Nevertheless, from a swing trader's perspective, the most intriguing transaction could be the long $260 calls expiring April 17. At the time, the ask on these calls stood at $25.15. Adding this figure to the strike price results in a breakeven threshold of $285.15. With a little less than a month to expiration, CRM stock is within striking distance of this target.

Of course, Wall Street players aren't in the business merely to break even. No, the smart money anticipates that there are profits to be made, which implies that CRM stock could move much higher. Determining the magnitude of a possible upswing is where the statistical data comes into view.

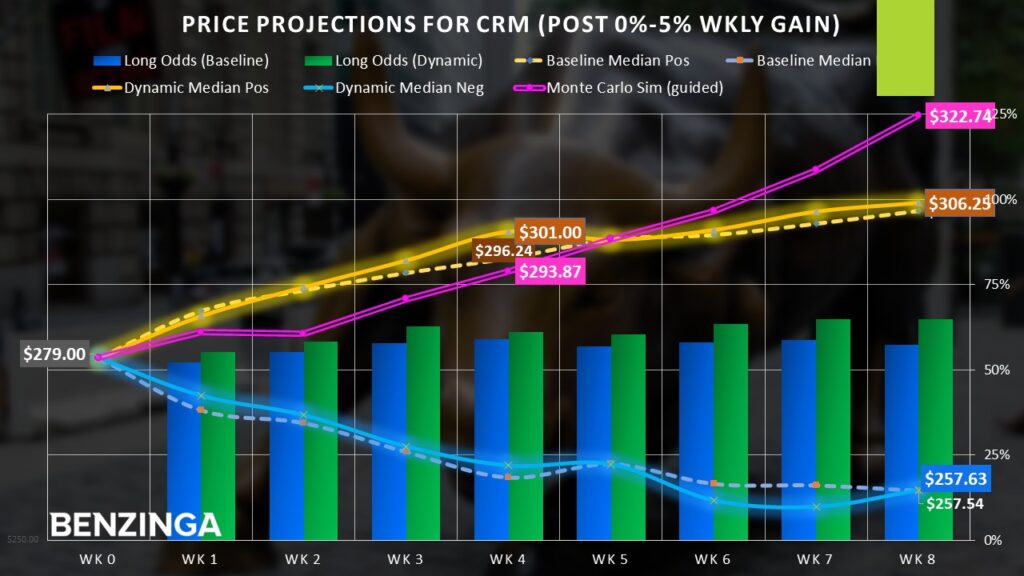

Using pricing information from January 2019, a long position held for any given eight-week period has a 57.41% chance of being profitable, a clear upward bias.

Right now, Salesforce’s stock is enjoying modest momentum, with shares up roughly 2% in the trailing five sessions. Under similar circumstances, a subsequent eight-week-long position has a nearly 65% chance of being profitable.

Throughout the eight weeks and assuming the positive scenario, traders may assume a median return between 9.24% to 9.77%.

Setting Up a Strategic Play on Salesforce Options

With the market intelligence above, aggressive traders can front-run an anticipated recovery with a multi-leg options strategy called the bull call spread. This particular approach is appealing because it effectively discounts a net long position.

For the previously mentioned April 17 expiration date, a tempting idea is the 280/290 bull spread. This transaction involves buying the $280 call (at a time-of-writing ask of $940) and simultaneously selling the $290 call (at a $480 bid). The proceeds from the short call partially offset the debit paid for the long call, resulting in a net debit paid of $460.

Should Salesforce’s stock hit the $290 short strike price at expiration, the trader collects the difference between the strike prices (multiplied by 100 shares per option contract) and the net debit paid, or a maximum reward of $540 per each spread. This translates to a max payout of over 117% on what is approximately a 4% move in the open market.

To be clear, if CRM stock doesn't cooperate, the trader is at risk of losing the entire net debit paid since the long call is currently out the money (OTM). However, it's impossible to realize such massive rewards in a large-capitalization enterprise like Salesforce unless there's significant volume involved. That's the power of leverage, which makes options trading risky but incredibly tempting.

Now Read:

Image: Shutterstock

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.