• Societe Generale’s Albert Edwards believes that the U.S. could soon set negative interest rates for the first time

• Edwards argues that the U.S. is currently in a worse economic position than Japan was prior to its lost decade

• He presents data that China’s slumping GDP numbers are actually much worse than they look

A new report by Societe Generale analyst Albert Edwards has the financial world buzzing, and not in a good way. Edwards argues that the U.S. is much closer to its next recession than most investors believe and the current near-zero interest rate environment has laid the groundwork for a negative Fed funds rate for the first time in history.

The zero lower bound

Most investors operate under the assumption that zero is the lower bound for interest rates and that the current near-zero rates in the U.S. indicate that the economy is still near the low point in its current cycle. However, Edwards points out that, in reality, while below-zero rates may be unprecedented in the U.S., they are certainly not unprecedented globally.

In fact, Sweden currently has a -0.35 percent policy rate in place. Even with interest rates at zero, Sweden had been unable to stimulate any significant inflation since the end of 2012, so it reduced rates to -0.25 percent in early 2015 and further to -0.35 percnt this summer.

Edwards believes that Sweden’s measures demonstrate that the zero rate bound is not a true limit on rates. “If -0.35% is possible, why not -3.5% or less?” he asks in his report.

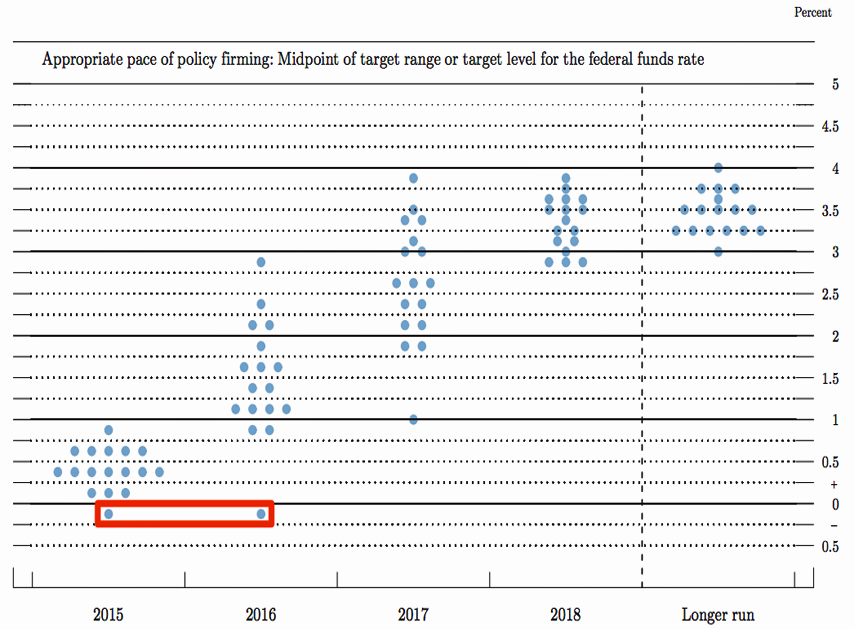

The negative dots

If Edwards’ scenario seems far-fetched, look no further than the Federal Reserve’s latest interest rate dot plot for confirmation of the possibility.

Clearly, the possibility of negative interest rates is a reality for one policymaker.

As if that idea wasn’t scary enough, the day after the dot plot was released, the Bank of England’s chief economist Andrew Haldane discussed the possibility of a ban on cash to eliminate the possibility of hoarding in a negative interest rate environment.

Edwards admits that even he hadn’t taken the scenario to that much of an extreme, but he does believe it could be messy. “The last seven years of exploding central bank balance sheets will seem like Bundesbank monetary austerity compared to what is to come,” he writes.

A lost U.S. decade?

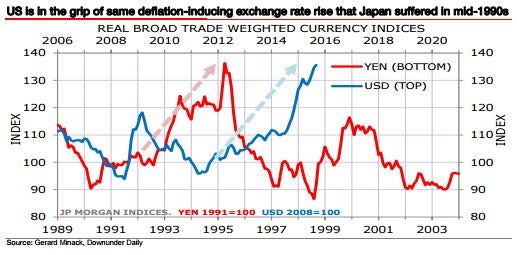

Japan was unwilling to breach the zero lower bound when it was suffering from deflation during its lost decade, so a potential U.S. journey into negative territory would be the first of its kind for a global economic powerhouse. Edwards points out that Japan’s lost decade was preceded by a rapid exchange rate rise similar to the one that the U.S. has recently been experiencing.

However, things could get much worse for the U.S. than they did for Japan during the 1990s. Despite its internal issues, Japan could rely on exports to other rapidly-expanding global economies throughout the lost decade. The U.S. will not be afforded the same luxury.

The numbers

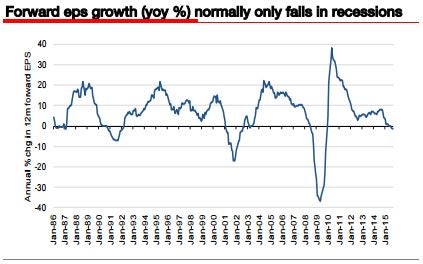

In his report, Edwards presents compelling evidence that a U.S. recession could be imminent. First, he points out that forward U.S. earnings growth has been on the decline, a phenomenon that usually precedes a recession.

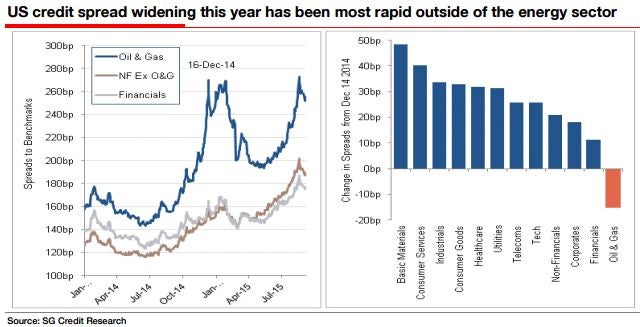

Market bulls argue that these numbers are skewed because of the extreme weakness in the energy sector, but Edwards points to rapid credit spread expansion in other sectors as well.

“Rising spreads are not just contained in the energy sector like they weren’t just contained in sub-prime,” he explains, drawing comparisons to the U.S. housing bubble.

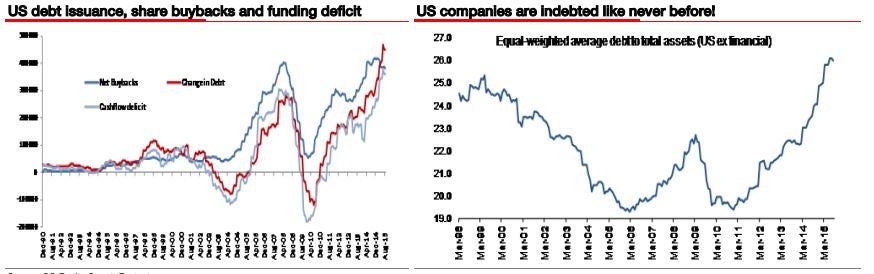

U.S. corporate debt levels have never been higher, but Edwards highlights how little of that debt has been spent on business expansion. The majority of that debt has been spent on equity buybacks.

China

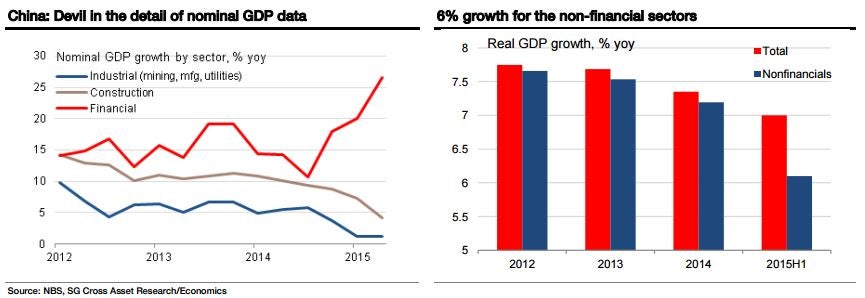

Edwards concludes his discussion with an overview of one of the main global market drivers in recent weeks: China. While China has been reporting 7.0 percent GDP growth throughout the first half of 2015, Edwards points out a troubling trend in the type of growth China is experiencing. GDP growth in China’s financial sector has exploded, while growth in construction has fallen off and growth in the industrial sector has fallen to nearly zero.

Takeaway

Edwards’ contrarian view of U.S. economic health is certainly a troubling one for investors and paints a very bleak picture of the potential for investment returns in coming years. If Edwards is correct, not only will there be no FOMC rate hike before the end of 2015, interest rates could soon be breaching the zero lower bound and begin heading into uncharted negative territory.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.