Tuesday, January 19

Wednesday, January 20

Thursday, January 21

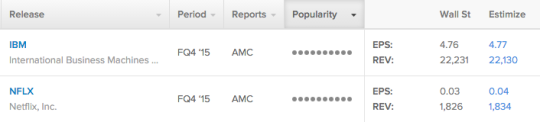

Netflix (NFLX)

Consumer Discretionary - Internet Retail | Reports January 19, after the close.

The Estimize consensus calls for EPS of $0.04, just a penny higher than Wall Street and two cents higher than company issued guidance. The Estimize community is looking for sales of $1.83B, just slightly above the Street's estimate.

What to watch: Coming into the new year, the FANG stocks (Facebook, Amazon, Netflix, Google), as they are called, seemingly had the most promise for 2016. Those names were up an average of 83% in 2015 as compared to the S&P 500 which was down around 1%. Netflix alone was up a resounding 130%, but that was then and this is now. Since Jan 4, the stock has fallen 5%, and expectations for fourth quarter earnings results which report after tomorrow's closing bell have been sliding as well. One main worry is domestic subscription growth which saw a surprising slowdown in Q4 2015 as competitors, Amazon Instant Video and Hulu began to establish their foothold in video streaming. Another area of concern is costs around international expansion. Netflix recently announced their intention to enter 130 international markets throughout 2016. By broadening their global reach, Netflix creates a new market with the opportunity to generate new subscriptions and bolster revenue growth. That being said, Netflix has already established itself in most of the lucrative markets around the world. Hence, its success elsewhere, while not guaranteed, will come with increasing content acquisition costs and lower operating margins than they have been accustomed to.

International Business Machines (IBM)

Information Technology - IT Services | Reports January 19, after the close.

The Estimize consensus calls for EPS of $4.77, just one penny above Wall Street. Revenue estimates from Estimize are actually below the sell-side at $22.13B vs. $22.23B.

What to watch: In 2015, share prices of IBM fell 16% as the IT company transitions away from traditional segments to high growth markets. IBM's struggles come due to a strong U.S. dollar, slower growth in emerging markets, and a societal shift away from software to cloud computing. Many of IBM's strategic initiatives in the past year, whether they were acquisitions or new patents, have been aimed at enhancing their position in cloud computing, Big Data or Internet of Things (IoT). Considering the enormous growth in this space, IBM has taken an aggressive stance towards growing this segment, not only to create a competitive edge, but also provide a much needed stable source of revenue. Despite a rapidly growing technology sector, IBM will face intense competition as they expand their new initiatives. IBM will find it difficult to carve out its niche in cloud computing as long as Amazon Web Services remains the preeminent cloud platform. Furthermore, the company's strategic investments come at a substantial cost. A rising debt burden should have a major impact on the operational efficiency of the company as a large portion of the company's earnings would be diverted towards servicing debt. IBM's lackluster growth in the past few quarters is unfortunately expected to continue after Q4 2015 earnings are reported and through 2016.

Goldman Sachs (GS)

Financials - Capital Markets | Reports January 20, before the open.

The Estimize consensus calls for EPS of $4.42, well above the Wall Street consensus of $3.79. Revenues of $7.57B are also higher than the Street's $7.27B.

What to watch: Three down, three to go. Big banks started out the earnings season respectably last week. Those that reported, JPMorgan Chase, Wells Fargo and Citigroup, all missed the Estimize consensus on the bottom-line, but were able to beat the expectations of Wall Street analysts. JPMorgan and Chase impressively beat both the Estimize and Wall Street consensus on the top-line, a sizable feat in this environment of low revenue growth. Like we've seen in many of the reports thus far, Goldman Sachs is likely to have several bright spots, but some headwinds to contend with as well. Fixed income has struggled due to low interest rates and consequently more institutional investors have shifted asset allocations to equities. On the other hand, M&A continues to be one of the strongest performers for Goldman Sachs followed by equity and debt underwriting. However, JPMorgan's report from Wednesday could suggest that debt underwriting will not be as robust for GS as previously thought. While JPMorgan reported one of the best quarters for its M&A advisory segment since the recession, they did struggle with low levels of activity in global debt capital markets, a problem since debt underwriting makes up a large chunk of the bank's investment banking fees. In 2016, growth areas for Goldman Sachs are expected to come from lower risk investments, investment banking and fixed income following interest rate hikes.

Southwest Airlines (LUV)

Industrials - Airlines | Reports January 21, before the open.

The Estimize consensus calls for EPS of $0.92, two cents above the Wall Street consensus. Revenues of $5.05B are slightly above the Street's expectation for $5.02B.

What to watch: Southwest's Q4 report comes on the heels of an industry wide fare hike. On January 5, five major airlines including American, Delta, JetBlue, Southwest and United all announced they were raising one-way U.S. domestic flight prices by $3. The news came at an uncertain time for the industry which is currently under investigation by the US Justice Department for potentially conspiring to keep fares artificially inflated by limiting the volume of flights. The latest price hike also comes amidst deteriorating oil prices. Airlines have been posting tremendous growth for the past several quarters in part due to fuel savings. It was initially believed that these savings would be passed onto the consumer, but instead flight prices have only increased. The S&P 500 airline industry (contains Delta, United, Southwest and American) is expected to post year-over-year earnings growth of 63% in Q4, compared to the overall S&P 500 which is anticipated to see profits decline by 2.2%. However, Southwest Airlines is the only one on the list expecting revenue growth, bucking the trend of languishing sales. It's also the only discount airline out of the bunch. We continue to see a disparity in expectations for discount airlines vs. larger carriers. Discount domestic airlines such as Southwest that fly to very few, if any, international destinations, do not have to contend with the strong dollar impact. Currency headwinds have been such a drag on multinational airlines, that several large carriers have decreased certain international routes.

Starbucks (SBUX)

Consumer Discretionary - Hotels, Restaurants and Leisure | Reports January 21, after the close.

The Estimize consensus calls for EPS of $0.46, only one cent above the Wall Street consensus. Revenues expectations are roughly in line at $5.38B.

What to watch: Starbucks had an impressive ride in 2015, with share prices increasing a resounding 47%. The biggest contributor to Starbuck's success has been their rapid growth in Pacific Asia and China, with CEO Howard Schultz recently announcing an aggressive expansion plan for China in 2016. Currently, Starbucks has 21,000 stores in over 65 countries and plans to open over 500 new stores in China alone this year. Both Asian and American stores have performed well posting strong same store sales growth, improving average ticket orders and increasing traffic. Best known for their coffee, the Seattle based company has also been focused on expanding higher margin food offerings, including ready made lunches and baked goods. That being said, coffee is still Starbuck's primary source of business and as of late, prices of the commodity have begun to fall. Financially, this has helped lower the company's cost of goods sold and improve margins. Outside of their in-store offerings, Starbucks has made strides to expand its digital and marketing initiatives. The coffee retailer now offers mobile ordering and delivery services, a popular loyalty program, and Starbucks Reserve coffee subscription in hopes of driving business. Starbucks, like many other multinationals, faces the risks posed by a relatively strong U.S. dollar. This however should not factor into what should be a strong 2016 for the coffee retailer, domestically and abroad.

Have a different opinion on how these companies will report? Share your estimate with us!

(Photo Credit: James Warwick)

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.