Can big banks swoop in to change the conversation on Wall Street? Earnings announced early Thursday by three of the biggest financial stalwarts appeared good for the most part, but whether that can soothe nerves frayed by geopolitical and fiscal policy concerns is unclear.

Looking at the three big banks that reported this morning, it’s a pretty decent set of numbers for two of them — JPMorgan Chase & Co. JPM and Citigroup Inc C. JPM reported first-quarter earnings of $1.65 a share on revenue of $25.59 billion, beating analysts' expectations by 13 cents on the bottom line and easily surpassing top-line estimates with a 17% rise in net income. Shares rose almost 1% in premarket trading.

Citigroup (C) posted a 17% rise in net income and beat analysts’ consensus estimate by 11 cents on the bottom line. Shares rose a little in pre-market trading as well.

Both JPM and C beat expectations for fixed income trading revenue, which isn’t too surprising. But they also beat on estimates for equity market revenue, which could be a good sign for the markets — evidence that people are participating. JPM also had good results on lending margin.

Another thing to watch is what’s going on in Washington, D.C. President Trump said on Wednesday that the U.S. dollar is too strong, according to media reports. That appeared to unsettle the market, and some of that concern seems like it might have carried over into Thursday morning. The dollar gave up a little vs. the euro and yen, and the 10-year U.S. Treasury yield fell under 2.25%. It’s a big deal when the president talks about the dollar this way, and it’s something that investors might want to keep their eyes on. If big banks hadn’t reported this morning, the dollar might be the biggest story out there.

Volatility remains elevated. VIX climbed above 16 early Thursday to new four-month highs, and that might reflect frustration with the slow pace of fiscal policy as well as the geopolitical situation and Trump’s dollar comment. Even as volatility waxed, volume stayed on the low side, perhaps reflecting caution among investors toward extending positions ahead of the long weekend, as the markets are closed Friday.

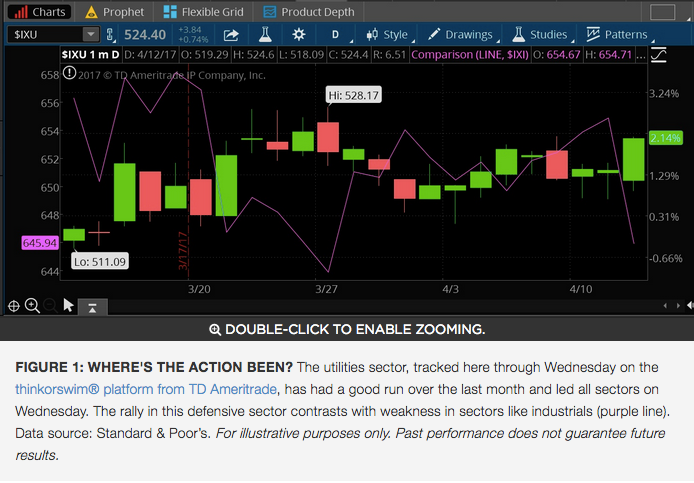

Another possible sign of continued caution: Defensive sectors like utilities, consumer staples, telecom, and health care outperformed traditional growth sectors like industrials, materials, and financials on Wednesday. Let’s see if that trend continues in the wake of these mostly strong big bank earnings.

Holiday Data

The markets may be closed tomorrow for the holiday, but the government doesn’t shut down. That’s why we have the somewhat odd occurrence of getting key economic data on a day it can’t be traded. Both the consumer price index (CPI) and retail sales come out at their usual 8:30 a.m. ET times Friday, but neither is expected to be all that exciting in terms of numbers. Wall Street analysts expect retail sales to tick down by 0.1% in March and CPI to be flat, according to Briefing.com. That compares with a 0.1% rise for both the previous month. Core retail sales could rise 0.2% in March and core CPI could also climb 0.2%, according to analysts’ consensus estimates. Both of those estimates would be equal to the previous month, as well.

Will Core Inflation Stay in Long-Term Range?

One number investors might want to keep watching is year-over-year core inflation, which sat at 2.2% last month. Core CPI year-over-year has been between 2.1% and 2.3% for 15 consecutive months, Briefing.com points out. Any change from these levels might have investors wondering about the Fed’s possible reaction.

Keeping Jobs Data in Perspective

The March Non-farm payrolls report last week may have been disappointing in terms of job growth, but it’s important to keep the bigger picture in mind. Even with just 98,000 jobs added in March, average monthly job growth so far in 2017 remains at nearly 180,000 — not really booming, but not too tepid, either. Let’s see what the April report brings, and whether that weak March figure turns out to be a one timer, as they might say in hockey.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.