Zinger Key Points

- Nvidia had guided third quarter revenue to $16 billion, plus or minus 2%.

- Analysts are upbeat about continued outperformance of Nvidia's Data Center segment, thanks to strong uptake of its AI accelerators.

- Markets are swinging wildly, but for Matt Maley, it's just another opportunity to trade. His clear, simple trade alerts have helped members lock in gains as high as 100% and 450%. Now, you can get his next trade signal—completely free.

AI stalwart Nvidia Corp. NVDA set a high bar for itself when it reported breathtaking results for its June quarter. The Santa Clara, California-based company now has the tall task of outperforming itself when it delivers its third-quarter report after the market closes on Tuesday.

What Wall Street Is Bracing For: Analysts, on average, expect Nvidia to report earnings per share of $3.36 on revenue of $16.12 billion, according to Benzinga Pro data. The Street forecasts suggest the company’s earnings per share will likely grow about 480% year-over-year and 24.44% sequentially. The consensus revenue estimate factors in year-over-year and quarter-over-quarter growth of 172% and 22.6%, respectively.

Here’s how the company fared in the preceding quarter and the year-ago quarter:

| Q2’24 | Y-o-Y Growth | Q-o-Q Growth | Q3’23 | Y-o-Y Growth | Q-o-Q Growth | |

| EPS (non-GAAP) | $2.70 | +429% | +148% | 58 cents | (-50%) | +14% |

| Revenue | $13.51B | +101% | +88% | $5.93B | (-17%) | (-12%) |

When Nvidia reported its June quarter results in late August, it guided third-quarter revenue to $16 billion, plus or minus 2%.

The company guided non-GAAP gross margin to 72.5%, plus or minus 50 basis points. This would mean an improvement from the second quarter’s 71.2% and the year-ago quarter’s 56.1%. Nvidia’s CFO, Colette Kress, attributed the second-quarter margin improvement to higher data center growth.

Raymond James analyst Srini Pajjuri said he expects another strong quarter from Nvidia, with a likely 5%-10% revenue beat.

See Also: Best Tech Stocks Right Now

Expectations For Nvidia’s Key Segments: Nvidia’s key business segments are Data Center, Gaming, Professional Visualization, and Auto. The Data Center Segment was the standout performer in the second quarter, thanks to robust sales of high-performance chips to cloud service providers and large consumer internet companies. The strong demand came on the back of the development of large language models and generative AI.

Oppenheimer analyst Rick Schafer models 22% sequential growth in Data Centers in the third quarter, aided by strong demand for Nvidia accelerators.

The Gaming segment has seen an upward revenue trajectory after bottoming at $1.57 billion in the third quarter of 2023.

| Q2’24 | Y-o-Y Growth | Q-o-Q Growth | Q3’23 | Y-o-Y Growth | Q-o-Q Growth | |

| Data Center | $10.32B | +171% | +141% | $3.83B | +31% | +1% |

| Gaming | $2.49B | +22% | +11% | $1.57B | (-51%) | (-23%) |

| Prof. Viz | $379M | (-24%) | +28% | $200M | (-65%) | (-60%) |

| Auto | $253M | +15% | (-15%) | $251M | +86% | +14% |

Forward Outlook: RayJay’s Pajjuri sees Nvidia weathering the mixed Cloud capex trends seen in the third quarter and the China export controls. He sees GPU demand outpacing supply through 2024 as AI adoption broadens across industries.

Despite competition, Nvidia will likely maintain more than 85% share in generative AI accelerators in 2024, Pajjuri said. The analyst expects the company to benefit from the mix shift from the A100 to H100 and the expected volume ramp-up of the H200, which will likely have about a 3% average selling price premium over H100.

“While a potential pause in customer spending ahead of new architecture ("Blackwell" likely coming in 2H24) presents some risk, we are not overly concerned given the significant amount of unmet demand for current "Hopper" products,” he added.

KeyBanc’s John Vinh sees upside in the second half, thanks to the ramp of L40S, its powerful data center GPU, and the incremental supply for CoWoS, an advanced packaging technology Nvidia sources from Amkor Technology, Inc. AMKR and Taiwan Semiconductor Manufacturing Co. Ltd. TSM for its high-performance processors.

Analysts do not see the China export restrictions as a handicap to Nvidia. Vinh sees Nvidia being able to backfill with the rest-of-the-world backlog, given extended lead times on H100, and also develop China-compliant chips.

Read Also: How To Buy Nvidia (NVDA) Stock

Nvidia Stock: Nvidia shares have gained some momentum since bottoming in late October as risk appetite, especially toward big techs, improved amid positive economic cues. The stock broke above the $500 psychological barrier on Monday and ended at a record high of $504.09, up 2.25%, according to Benzinga Pro data.

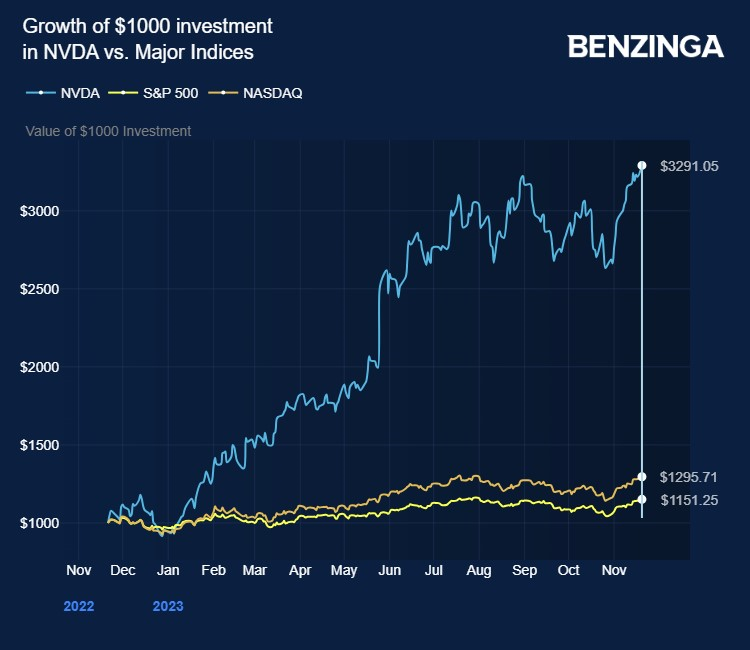

The stock has vastly outperformed the S&P 500 Index and the tech-focused Nasdaq Composite Index.

Chart Courtesy of Benzinga

The stock’s year-to-date gain of 245% makes it the best-performing S&P 500 stock of the year. Although the valuation could instill caution among investors, analysts are optimistic about further upside from current levels. The average analysts’ price target for the stock is $644.07, according to data compiled by TipRanks. This suggests a scope for about a 28% upside from current levels.

More importantly, as the market has inflected higher after the lackluster phase seen in the August-October period, strong results from Nvidia could add momentum to the market’s rally.

Read Next: NVIDIA, Best Buy And 3 Stocks To Watch Heading Into Tuesday

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.