Zinger Key Points

- Headline PCE rose to 2.7% YoY, surpassing projections, while core PCE held at 2.8% YoY, defying expectations of a decline.

- Analysts debate the possibility of further rate cuts amid sustained high inflation levels and provide strategies for navigating markets.

- Don't face extreme market conditions unprepared. Get the professional edge with Benzinga Pro's exclusive alerts, news advantage, and volatility tools at 60% off today.

The recent release of the Personal Consumption Expenditure (PCE) price index, a key metric favored by the Federal Reserve for gauging inflation, delivered higher-than-anticipated annual rates last month, suggesting that price pressures are facing significant hurdles to achieving the 2% target.

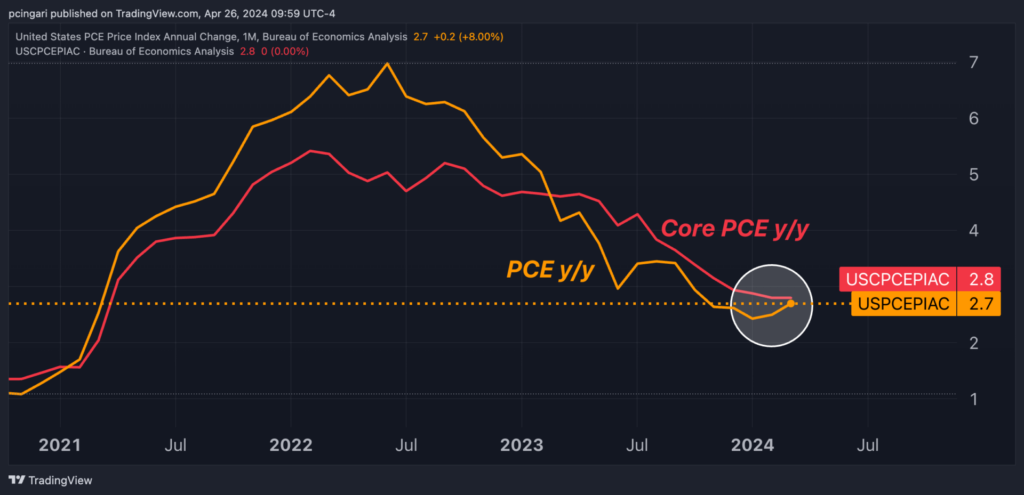

The headline PCE price index saw a jump from 2.5% to 2.7% year-on-year in March, surpassing projections of a more modest increase to 2.6%. The core PCE price index, excluding volatile energy and food items, held steady at 2.8% annually, defying expectations of a decline to 2.6%.

Economists and market experts offered insights into the implications of this latest PCE report, shedding light on potential Federal Reserve policies going forward.

Chart: Is The Disinflationary Trend Already Over?

March PCE Report: Economist Takeaways

Mohamed El-Erian, economic adviser at Allianz, emphasizes that while March’s PCE inflation slightly exceeded consensus forecasts, the miss was smaller than expected, and monthly readings were in line. He highlights the importance of considering the combination of factors, suggesting that while high inflation poses challenges, stagflation would be far worse for the economy and markets.

Chris Zaccarelli suggests that markets should find relief in the PCE data aligning with expectations on a monthly basis. He also advises against expecting multiple Fed rate cuts given the sustained high inflation levels.

“We believe that rate cuts aren't necessary for the bull market to continue. Instead, continued economic expansion and growth in corporate profits – which are already seeing from the largest companies in the market – are what will propel stock prices to new highs,” Zaccarelli states.

The Kobeissi Letter raises a crucial question about the Fed’s potential actions, noting that consecutive months of rising CPI, PPI, and PCE inflation may complicate the possibility of interest rate cuts.

Clark Bellin, president and chief investment officer at Bellwether Wealth, suggests that while Friday’s PCE data doesn’t rule out rate cuts for 2024, any cuts are likely to occur toward the end of the year. He notes that the market’s optimism about the speed and extent of rate cuts may be unjustified given the persistently high inflation levels.

“Investors should continue to be on the lookout for opportunities in the market and consider taking advantage of the stock market’s recent pullback, where many quality stocks went on sale. The overall trend of the market is to the upside, and the declines in recent weeks are part of a broader market correction,” Bellin says.

Bank of America’s economist Michael Gapen underscores that inflation risks remain tilted upwards, with the likelihood of prolonged high inflation. He anticipates the Fed to adopt a wait-and-see approach at the upcoming FOMC meeting, allowing policy more time to take effect. Bank of America currently sees just one rate cut for the remainder of the year, occurring no earlier than December.

Jamie Cox, managing partner for Harris Financial Group, stresses the challenge posed by stubborn inflation and he anticipates the Fed addressing the balance sheet before considering rate cuts, possibly starting with tapering the balance sheet runoff as early as June.

Read now: US Economy Grows 1.6% In Q1, Sharply Below Expectations As Price Pressures Weigh On Spending

Photo: Shutterstock

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.