For the second straight day, investor attention could zero in on Capitol Hill as Fed Chair Jerome Powell takes the mic to address elected officials on the economy. He delivered a pretty dovish message yesterday, but markets didn’t appear to move too much in response.

Other than the Powell testimony (more below), there doesn’t appear to be a major theme Wednesday as things get started. In geopolitics, President Trump meets with North Korea’s president today, but that arguably hasn’t been a market mover lately. There’s also some tension developing between Pakistan and India, which could inject a bit of anxiety into things. Stocks fell yesterday and began the new day with a weaker tone amid mixed action overseas.

On the earnings front, there was some reassuring news from Best Buy Co Inc BBY this morning. The electronics retailer’s shares were up 10% in pre-market trade after it blew past third-party estimates, raised its dividend and announced a share buyback program. Adjusted earnings were $2.72 per share, well ahead of the Street’s expectations, according to FactSet estimates. Revenue of $14.8 billion was down from a year prior but slightly beat estimates. A traditional retailer that still relies on foot traffic, BBY has been struggling the past year, with shares down about 17% before the earnings release.

Lowe’s Companies Inc LOW shares were also on the rise in pre-market trading despite just missing Wall Street analysts’ sales estimate. The company did beat analyst consensus on earnings per share, however, and stuck to its 2019 outlook. With housing market data generally weak lately, shares of home improvement companies like LOW and Home Depot Inc HD might serve as a barometer for investors. Weak housing market data continued this week as the pace of home price growth hit a four-year low on an annual basis, according to the Case-Shiller Index reading for the last quarter of 2018.

In less impressive earnings news, Weight Watchers International, Inc. WTW shares, once soaring with the backing of celebrity spokespeople, plunged 35% on the heels of its earnings report. The weight loss company was undergoing a revival of sorts, but said it had a “soft start” to 2019 and offered weak guidance. Still, revenue was up 6% to $330 million from a year prior.

Losing Steam?

Major U.S. indices slipped Tuesday, with a late rally attempt failing to hold and the S&P 500 Index (SPX) again finishing below 2800. Some media reports cited weak Home Depot (HD) earnings as the primary instigator, but arguably the real problem was a lack of new positive catalysts, especially on the China trade front.

Actually, there was arguably some good news from overseas Tuesday, but it didn’t seem to get much attention in the markets. Chances of an abrupt and chaotic Brexit receded a bit when Prime Minister Theresa May agreed that Parliament should have the option to seek a delay in Britain’s exit plans, according to a New York Times report. This doesn’t necessarily mean things will go more smoothly, but it could conceivably push Brexit beyond what’s now the March 29 deadline, giving the markets a little more breathing room.

The British pound rose on the news, while the Dollar Index continued to retreat from recent highs and is now back to testing the 96 level.

FAANGs Up Again, But Is Anyone Paying Attention?

For the third-straight day on Tuesday, FAANGs looked shiny as four of the five gained ground. Though gains were mostly light, the five stocks all spent much of the day in the green, building on progress made Friday and Monday. All five had risen Friday, and four rose Monday.

A few months ago, before the Q4 washout, this strength in the FAANGs might have been the leading story of the day. However, with FAANGs mostly trailing the S&P 500 (SPX) year to date, they’ve lost their starring role to some extent. The narrative has changed over the past few months.

Instead, a lot of focus has shifted toward the rally in Industrials, which fell Tuesday but are up 18% since Dec. 31. What’s interesting about this market is the ability of a new group to take leadership. It seems like every time the naysayers start questioning whether the rally can continue, a sector you didn’t count on has stepped in to save the day. Now, there’s no guarantee that will keep happening, but the way industrials replaced FAANGs does arguably speak to the market’s resilience.

Two of the best-performing sectors Tuesday were Info Tech and Communication Services, both of which contain FAANG stocks. The Communication Services sector could be an interesting area for the rest of 2019 and 2020 given all the competition in the streaming space and the entry of companies like Netflix, Inc. NFLX into a major film distribution role. It shouldn’t go unnoticed that Roma, a film that received 10 Academy Award nominations, was distributed by Netflix.

Technical Hurdle

From a technical perspective, Tuesday looked like another disappointing day for the bulls. After bounding through a number of technical resistance points so far this year, the SPX seems to be having trouble with the psychological 2800 mark. Tuesday was the second-straight day where the SPX traded above that level but then closed below it, which technicians might see as a possible sign of weakness and maybe of a rally that’s breathing some thin air.

Another level to consider watching is the region around 2814, which the SPX neared this week and which is near an intraday high it posted in early November. While not every investor watches technical levels, it doesn’t take too much understanding of support and resistance to see what it might mean if an index keeps bouncing off of one but fails to pierce it. Yes, individual equities are important to watch, but sometimes it’s equally important to glance up at the overall macro picture, because it can influence those individual stocks as well.

Data-wise, Tuesday was another day the housing market might rather forget. December housing starts fell more than 11% month-over-month, and were well below analysts’ consensus projections. Homebuilding company stocks, which have generally been moving higher this year, took a step back Tuesday. However, some analysts pointed out that winter can be a slow and choppy time for the industry, so perhaps it’s worth waiting for spring to get a better picture.

Consumers, Powell Both Sound Confident

Looking for a more positive data story? It came right after housing starts when consumer confidence for February surprised to the upside. This might have partially reflected consumers’ relief at the end of the government shutdown and strength in the labor market, Briefing.com said. It also might give some investors reason to hope for yet another bullish payrolls report at the end of next week. It’s not universal, but people who have jobs often tend to have more confidence about spending.

Fed Chairman Jerome Powell’s testimony to Congress is scheduled to continue today after Powell didn’t really make any big waves at the Capitol on Tuesday (see more below). In a nutshell, Powell basically said he continues to see strength in the labor market and didn’t sound all that worried about inflation. He is concerned about U.S. debt levels, but investors knew that based on his past remarks. The market chopped around during Powell’s testimony but didn’t experience any steep drops. The yield on the 10-year U.S. Treasury note slipped back under 2.64%, near the bottom of its recent range.

Meanwhile, the VIX continued to climb from recent four-month lows Tuesday, rising back above 15 after falling below 14 last week. This, combined with the stock market’s struggles to climb above resistance and continued strength in Treasuries, might spell possible caution gathering after weeks of nearly constant rallies across the major stock indices.

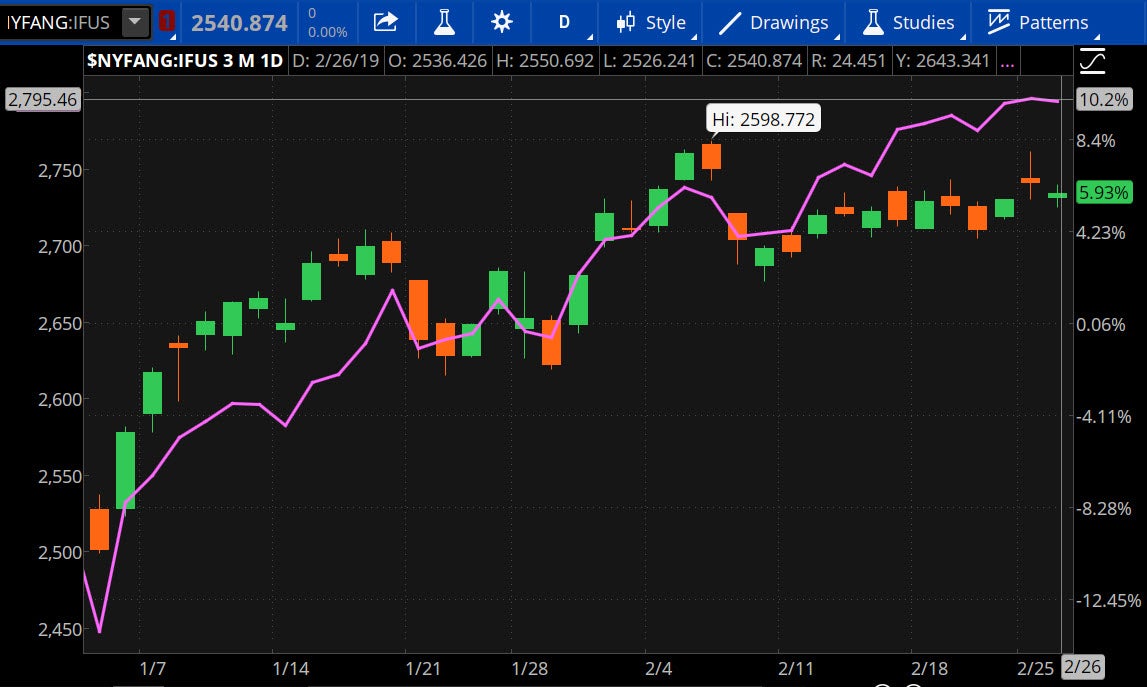

Figure 1: SPX Outpacing FAANGs: The NYSE FANG+ Index ($NYFANG:IFUS - candlestick) has had a strong start to the new year. However, it's been outpaced by the S&P 500 Index (SPX). Data Source: ICE, S&P Dow Jones Indices. Chart source: The thinkorswim® platform from TD Ameritrade. For illustrative purposes only. Past performance does not guarantee future results.

Figure 1: SPX Outpacing FAANGs: The NYSE FANG+ Index ($NYFANG:IFUS - candlestick) has had a strong start to the new year. However, it's been outpaced by the S&P 500 Index (SPX). Data Source: ICE, S&P Dow Jones Indices. Chart source: The thinkorswim® platform from TD Ameritrade. For illustrative purposes only. Past performance does not guarantee future results.

Presidential POV: Someone once called the presidency the “bully pulpit,” meaning it gives one person’s voice a lot of influence. The reasoning behind that grew pretty evident this week for investors as two tweets by President Trump arguably had a big impact on the stock and commodities markets. The first was his weekend tweet about delaying a tariff raise on Chinese products thanks to trade negotiations going well. The Shanghai Composite rose more than 5% in one day after that announcement.

The presidential effect occurred for a second time on Monday morning when Trump tweeted that oil prices were getting too high and warned OPEC to consider its policy. Crude subsequently fell 3% and didn’t gain back much of that Tuesday. While this isn’t a political column, the tweets might be a reminder that more than ever (thanks partly to social media), it’s important to keep one ear turned toward Washington to see if anything potentially market-moving might be going viral.

Soft Touch?: Just over a year ago, U.S. stocks got crushed after a monthly payrolls report showed year-over-year wage growth near 3%, unleashing investor fears of inflation. What a difference a year makes, as Fed Chair Jerome Powell told senators yesterday he’s not too concerned about any inflationary impact as wages continue to rise 3% month after month. In his question-and-answer session, Powell painted the wage growth as a good thing, especially with wages growing faster than inflation. The Fed, he said, plans to remain patient about policy changes and still expects inflation to be near its 2% goal.

Listening to Powell, it seems that maybe the Fed has realized it can take a different approach after watching inflation stay pretty stable near or even below 2% over the last year despite rising wages. Or maybe the Fed’s four rate hikes last year did what it took to keep a lid on price growth even as the economy added jobs at a furious rate and the labor force started to expand a little. There’s a phrase some economists might use to describe an improving jobs picture accompanied by manageable inflation: “Soft landing.” One wild card, however, is that energy prices retreated dramatically late last year, removing a huge potential source of inflation pressure. Crude is up more than 20% from its December lows, so the Fed is likely to keep an eye on that for signs of a broader price impact.

Mind the Gap: Last year, we also heard a lot of concern from economists about the narrowing yield curve, which measures the gap between shorter-and-longer-term U.S. Treasury note yields. The gap between 10-year and 2-year yields often gets the most attention, and it narrowed to single digits as the economy and stock market weakened in Q4. Some economists worry that a narrowing gap can point toward possible recession, and the faltering curve can also weigh on Financial sector profits. So far this year, however, the yield curve has retreated from investor consciousness, at least a bit, and that’s in part because it’s been so stable. As of midday Tuesday, the gap stood at around 16 basis points, not far off of where it's been for some time. While that’s historically low, it’s up from the narrowest times last year. Still, some economists would probably like to see it get wider so that the risk of inversion—which often accompanies recessions—lessens. The Fed’s pause on rate hikes might be helping keep shorter-term yields from gaining on longer-term ones. Over the last month, the 2-year yield is down 12 basis points while the 10-year has fallen 11 basis points.

Information from TDA is not intended to be investment advice or construed as a recommendation or endorsement of any particular investment or investment strategy, and is for illustrative purposes only. Be sure to understand all risks involved with each strategy, including commission costs, before attempting to place any trade.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.