Currency traders may wonder if they are being punished.

Since late last October trend has vanished from the FX Markets. There seems to be a new law of foreign exchange markets--Every sustained movement will be met by an equal and opposite reversal, (apologies to I. Newton).

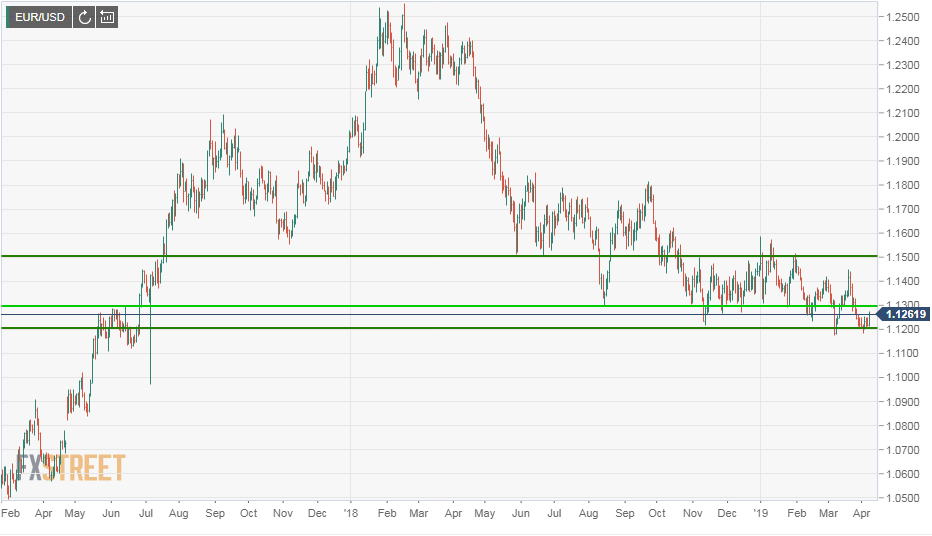

From the end of October to the beginning of March, more than four months, the euro traded in a two figure range against the US dollar, from 1.1500 to 1.1200. Since then the spread has been from 1.1200 to 1.1400. The slight negative euro bias from the start of the period to then end cannot be called a direction.

The yen has been more mobile with a range of 114.00 to 107.00 but the result has been the same. On October 26th the USD/JPY closed at 111.88. As of this writing it is trading at 111.53.

Sterling (GBP/USD) has moved between 1.3300 and 1.2600, trading down to December and higher in the New Year. The result has been yet more of the same. On November 1st the sterling closed at 1.3015. It is at 1.3065 on the afternoon of April 8th.

Dollar/Swiss, (USD/CHF) was at 1.0084 on October 31st. Currently it is 0.9991. The Australian Dollar (AUD/USD) finished November 1st at 0.7206 against the US Dollar. It is now 0.7128. The New Zealand Dollar (NZD/USD) was at 0.6886 on November 1st, April 8th sees it at 0.6746.

Of the majors the Dollar/Canada (USD/CAD) is the closest thing to an exception. On November 1st it finished at 1.3086, it is now at 1.3311.

Despite the absence of a market response the last five months have not been devoid of events or surprises.

The Federal Reserve raised its base rate in December and reversed policy six weeks later. The growth rate of the US economy halved over six months from 4.2% annualized in the second quarter to 2.2% in the fourth while the American job machine continued to churn. Unemployment stayed below 4% and for many groups was at historical lows. Initial jobless claims sank to levels not seen in 50 years. Consumer optimism was buoyant but retail sales plunged in the Christmas shopping season.

In Europe the ECB began an economic support loan program just months after ending its financial crisis bond purchases. Italy entered its third recession of the past decade under a Eurosceptic populist government. Germany skirted a technical recession and saw sentiment in its vaunted manufacturing sector drop to its lowest level since the financial crisis.

France erupted in countrywide riots and protests that demolished the popularity of President Macron but offered little in the way of an alternative political or economic program.

Great Britain continued to tie itself in political and Parliamentarian knots over Brexit. Almost three years after the departure vote on June 24th 2016, there is still no plan for leaving the European Union, for staying, or even for how to decide its future.

China’s industrial output, exports and growth rates sagged to levels not seen since the financial crisis as Beijing poured money into its economy and tried to manage its trade dispute with the United States without terrorizing its own or the global economy.

In less confused times any one or two of these developments would have sent currencies into motion.

Two unusual situations have kept the markets from enacting a new scenario to replace the strong dollar creed of the last two years. The first is in the EU, the second is in China.

Economic growth in the US and the EU has moved out of phase. The US is expanding and has the economic and rate cushion to maintain its pattern regardless of what happens globally. The EU has neither. Its growth is below 1% and with the ECB’s main refinancing rate at zero, it has limited and weak options for avoiding a recession.

In less fraught times the Fed move to a neutral rate policy after three years of tighter money would have taken the supports from under the dollar and sent the euro soaring. But with the ECB signaling its own return to liquidity provisioning at almost the same time as the Fed the two policy changes have negated each other, leaving the currency markets without direction.

China has a problem born of its rapid ascent into the industrialized world. Despite its export prowess, the mainland’s limited success at developing a domestic market has left its return to stronger growth largely dependent exports, that is, on the resolution of its trade negotiations with the United States.

If the US/China trade talks result in an agreement the relief rally in the global economy will power equities and the dollar. But until the deal is clinched there is no reason to take the US currency higher.

Patience is not a market virtue but prudence is.

Image sourced from Pixabay

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.