First, avoid any ETFs below a $100 million market cap. Anything smaller puts you at risk of inadequate liquidity, too large a bid/ask spread and tracking error. Even $100 million can be too low. The bigger the market cap the less trading risk. Same rule applies to How To Find the Best ETFs.

There are plenty of free services that allow you to screen out the smaller ETFs and minimize your trading risk.

The focus of this article, however, is on the underlying investment potential of ETFs. This potential is much more difficult to assess because it requires researching the investment potential of the ETF’s holdings.

Research on holdings is necessary due diligence because an ETF’s performance is only as good as its holdings’ performance. No matter how cheap, if it holds bad stocks, the ETF’s performance will be bad.

PERFORMANCE OF ETF’s HOLDINGs = PERFORMANCE OF ETF

You cannot rely on the ETF label/name to accurately reflect the ETF’s holdings. ETFs with the same label often have radically different holdings. See Barron’s “The Danger Within”.

My ratings on ETFs are based on deep, fundamental analysis of their holdings. I aggregate stock ratingsof their holdings to get the ETF’s rating.

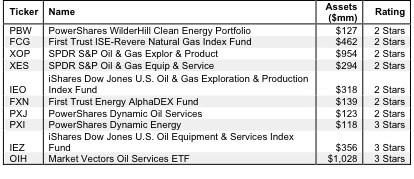

Figure 1 shows my ranking of the worst ten Energy Sector ETFs. Here are my rankings on all 20 US equity energy sector ETFs.

Not a single Energy Sector ETF gets an Attractive or better rating. PowerShares WilderHill Clean Energy Portfolio (NYSE:PBW) is my worst-rated Energy ETF (with assets over $100 million). It allocates 45% of its portfolio to stocks that get a Dangerous or worse rating. Only 5% of its holdings get an Attractive or better rating.

Figure 1: Worst 10 Energy Sector ETFs

My ETF rating also takes into account the total annual costs, which represents the all-in cost of being in the ETF. This analysis is simpler for ETFs than funds because they do not charge front- or back-end loads and transaction costs are incurred directly. There is only the expense ratio, which is normally quite low. However, my ratings penalize those ETFs with abnormally high expense ratios or any other hidden costs.

Honestly, when the ETFs are invested so heavily in bad stocks, the expense ratio is the least of your problems.

Figure 2 shows my ranking of the worst ten large-cap growth ETFs with a market cap over $100 million based on the quality of their holdings. Here are my rankings on all 25 US equity large cap growth ETFs.

Figure 2: Worst 10 Large Cap Growth ETFs

Note that none of the Large Cap Growth ETFs earn my Dangerous or Very Dangerous Rating. All of them get my Neutral (3 Star) rating. Nevertheless, investors should not settle. There are four Large Cap Growth ETFs that get my 4-Star or Attractive Rating.

First Trust Large Cap Growth AlphaDEX Fund FTC is my worst-rated Large Cap Growth ETF with more than $100 million in assets. It earns that rating by allocating nearly 20% of its portfolio to Dangerous-or-worse rated stocks. Another 40% of its portfolio goes to Neutral stocks. In other words, this ETF does not offer a high-quality portfolio of stocks. On the other hand, my top-rated Large Cap Value ETF, Vanguard S&P 500 Growth ETF (NYSE:VOOG), allocates over 62% to stocks that get my Attractive or Very Attractive rating.

My favorite stock that shows up in the top Large Cap Growth ETFs is Apple (NYSE:AAPL). This stock gets my Very Attractive rating. AAPL has a return on invested capital (ROIC) of 334%, which places it in the top quintile of all companies. As I detail in “Apple Bears Have It Wrong”, investors do not fully recognize the bargain price at which APPL is selling given its extraordinarily high ROIC and growth.

My favorite Energy Sector stock is Exxon Mobil (NYSE:XOM). In “Slow and Steady Wins the Race”, I explain how XOM has created enormous value for shareholders over the last quarter century. Buying Exxon Mobil (XOM) now is one of the easiest calls in the market these days. With superior cash flows, a cheap valuation and one of the strongest competitive positions in the business world, it is hard to make a straight-faced argument against owning this stock anywhere below $100. My model shows the stock is worth $140 if one assumes profits never grow from 2011 levels, i.e. the “no-growth” value of the stock.

The takeaway is that investors should buy ETFs that hold high-quality stocks. No reason to pay fees, even the lower ETF fees, to own bad stocks.

Disclosure: I own AAPL and XOM. I receive no compensation to write about any specific stock, sector or theme.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.