Here are some replacement names for some of the long exposure I cut.

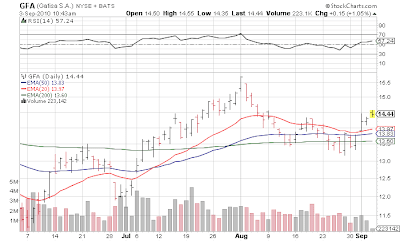

First, a name we've held many times the past 3 years Brazilian homebuilder Gafisa (GFA) [thanks to the reader who reminded me of it this morning]. Gafisa has been under pressure but Brazil's sizzling economy has put pressure on the central bank to increase interest rates (the exact opposite situation as the U.S. is facing), and higher rates always hurt homebuilders. If the global slowdown causes the central bank to pause this should help the name. Either way it's back over support and not overbought like much of what we own in the portfolio. I'll begin a 2.1% stake in the $14.40s. The stock held mid $13s quite well during the recent selloff, so we have an easy area to identify as a potential stop loss in the future.

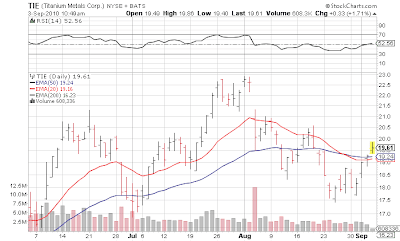

Titanium Metals (TIE) is an incredibly volatile name, very tied to the aerospace industry but generally runs when "risk is on". Unfortunately Boeing has delayed its new jet about 82,000 times so each time it hits this stock. That said it just regained some areas of support AND if you draw a trend line of its highs in August, it just broke over that level as well. So a move to S&P 1130 if/when, should help a name like this 'catch up'. This is not an "investing" stock - but a trading stock... I plan to be out completely if it makes a good run. If the S&P 500 begins to reverse and break down this will be the first name punted since its never in 'strong hands'. I don't think it has been in the portfolio since 2007. 2.2% exposure in $19.60 area.

Last but not least is a name I've never owned before, Power-One (PWER) - I noted yesterday that Chinese solar stocks (at least some of them) had made some big moves of late and were amongst the top performers. This is not Chinese and not a traditional solar player but its main growth driver, inverters are a backdoor solar play. While not a high margin business (almost nothing in solar is) the revenue growth is substantial. The company had a great quarter in late July....

For the quarter, the company reported revenue of $215 million and profits of 17 cents a share, ahead of the Street consensus at $185.7 million in revenue and profits of 10 cents a share. For the third quarter, PWER sees revenue of $250 million to $270 million, well above the old Street consensus forecast of $199. 6 million.

... where it gapped up from low $10s to mid $12s, topping out at $13 a few weeks later. Showing in this bipolar market how you need to take your trades and lock in gains (or lose them), it then "filled the gap" and gave back the entire move. But now it is in a more solid technical position so we'll take a stab here with a 2.2% stake around $11.40.

EPS estimates have gone up from mid .30s to mid .70s during the past 90 days (for 2010) and from 50 cents to just over a dollar (for 2011) so you can see how analysts have misjudged the name.

Since this company is new and I'm not doing the full in depth piece I normally do with new ideas, I'll offer a few links

Long names mentioned in fund; no personal position

Market News and Data brought to you by Benzinga APIsFirst, a name we've held many times the past 3 years Brazilian homebuilder Gafisa (GFA) [thanks to the reader who reminded me of it this morning]. Gafisa has been under pressure but Brazil's sizzling economy has put pressure on the central bank to increase interest rates (the exact opposite situation as the U.S. is facing), and higher rates always hurt homebuilders. If the global slowdown causes the central bank to pause this should help the name. Either way it's back over support and not overbought like much of what we own in the portfolio. I'll begin a 2.1% stake in the $14.40s. The stock held mid $13s quite well during the recent selloff, so we have an easy area to identify as a potential stop loss in the future.

Titanium Metals (TIE) is an incredibly volatile name, very tied to the aerospace industry but generally runs when "risk is on". Unfortunately Boeing has delayed its new jet about 82,000 times so each time it hits this stock. That said it just regained some areas of support AND if you draw a trend line of its highs in August, it just broke over that level as well. So a move to S&P 1130 if/when, should help a name like this 'catch up'. This is not an "investing" stock - but a trading stock... I plan to be out completely if it makes a good run. If the S&P 500 begins to reverse and break down this will be the first name punted since its never in 'strong hands'. I don't think it has been in the portfolio since 2007. 2.2% exposure in $19.60 area.

Last but not least is a name I've never owned before, Power-One (PWER) - I noted yesterday that Chinese solar stocks (at least some of them) had made some big moves of late and were amongst the top performers. This is not Chinese and not a traditional solar player but its main growth driver, inverters are a backdoor solar play. While not a high margin business (almost nothing in solar is) the revenue growth is substantial. The company had a great quarter in late July....

For the quarter, the company reported revenue of $215 million and profits of 17 cents a share, ahead of the Street consensus at $185.7 million in revenue and profits of 10 cents a share. For the third quarter, PWER sees revenue of $250 million to $270 million, well above the old Street consensus forecast of $199. 6 million.

... where it gapped up from low $10s to mid $12s, topping out at $13 a few weeks later. Showing in this bipolar market how you need to take your trades and lock in gains (or lose them), it then "filled the gap" and gave back the entire move. But now it is in a more solid technical position so we'll take a stab here with a 2.2% stake around $11.40.

EPS estimates have gone up from mid .30s to mid .70s during the past 90 days (for 2010) and from 50 cents to just over a dollar (for 2011) so you can see how analysts have misjudged the name.

Since this company is new and I'm not doing the full in depth piece I normally do with new ideas, I'll offer a few links

Long names mentioned in fund; no personal position

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Loading...

Posted In: Consumer DiscretionaryDiversified Metals & MiningElectrical Components & EquipmentHomebuildingIndustrialsMaterials

Benzinga simplifies the market for smarter investing

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.

Join Now: Free!

Already a member?Sign in