This past Tuesday night news hit that BATS Global Markets was in the process of settling with the SEC on the claim that Direct Edge provided unfair perks to certain high frequency traders (HFT), a development that might set a pivotal precedent in the market structure debate. News of the possible settlement was preceded by the departure of William O’Brien who ran Direct Edge with its twin exchanges before selling it to BATS in early 2014, becoming the second-in-command of the combined entity.

In an effort to challenge Brad Katsuyama of the Flash Boys fame live on TV, O’Brien stated that his exchange’s matching engine (used to match buy and sell orders) used direct feeds provided by other exchanges. However Direct Edge’s matching system used staler data from the SIP (securities information processor) - not the direct feeds - for several important housekeeping tasks. In a spectacular public relations failure, the NY Attorney General forced BATS to publicly correct O’Brien’s statements.

One person in the mix who may have not been remembered is Haim Bodek. After coming out publicly in Scott Patterson’s Dark Pools as a critic of exchanges that cater to HFT, Haim was on a one-man crusade to save his reputation by making a convincing case against the HFT industry. In the end, he wound up triggering SEC investigations that (so far) led to an exchange head being forced to step down. For those unaware, Haim was also the real star of the VPRO film Wall Street Code. In the film Haim used the example of skipping in line while buying Metallica concert tickets:

In a phone conversation with Benzinga, Haim noted this (yet to be announced) settlement would set precedent for future concerns about abuses taking place on securities exchanges. Direct Edge wasn’t the only exchange nor the first exchange to do what it did, which was the creation of symbiotic relationships between exchanges and HFTs.

|

Month |

Year |

Event |

|---|---|---|

|

August 1 |

2012 |

Knight Capital $440M loss |

|

August |

2012 |

Goldman $100M options trading glitch with trades eventually busted |

|

August 22 |

2012 |

Nasdaq goes dark for 3 hours (NASDARK) |

|

September |

2012 |

Hold Brothers Brokerage fined for "spoofing" |

|

September |

2012 |

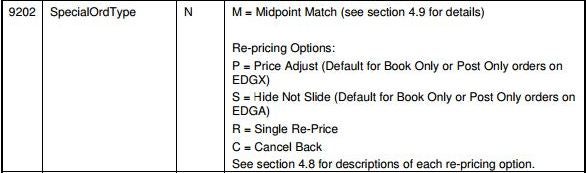

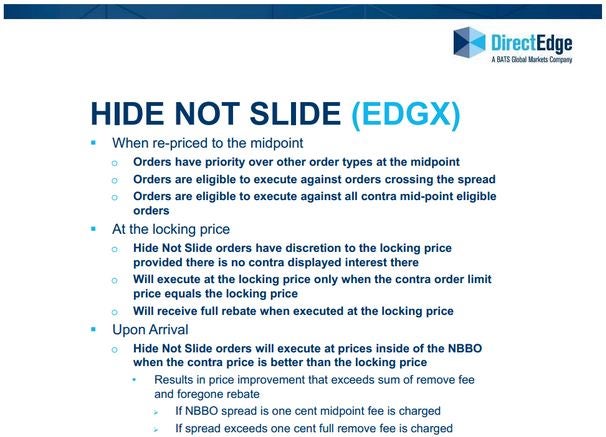

The Wall Street Journal runs an in-depth article on Hide-Not-Slide order type |

|

September |

2012 |

NYSE sued $5M for seller faster data access to special clients |

|

January |

2013 |

The Problem Of HFT is released by Haim Bodek highlighting "special order types" and exchange abuses |

|

August |

2013 |

BATS & Direct Edge merger talks surface - Deal takes place so quickly it finishes ahead of schedule |

|

October |

2013 |

Direct Edge publishes its "Order Type Guide" |

|

November |

2013 |

Wall Street Code is released |

|

February |

2013 |

O'Brien misinforms the public about what Direct Edge uses to match orders |

|

July |

2014 |

O'Brien steps down as President of BATS Global Markets |

|

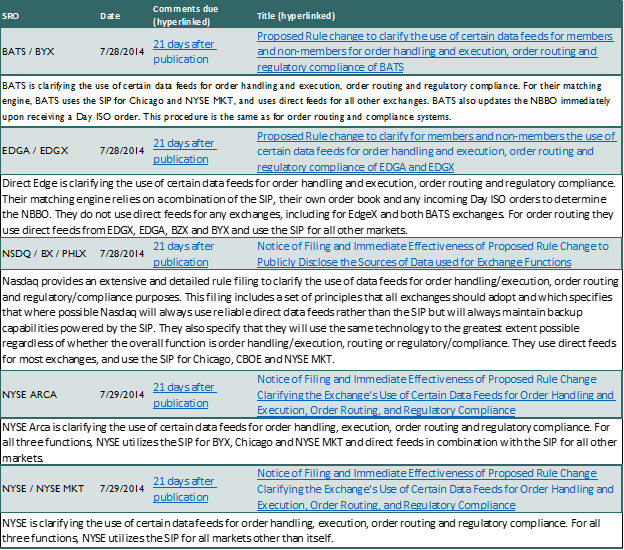

July 28-29 |

2014 |

All US equity exchanges adopt rules on the usage of SIP and direct feeds |

|

August 1 |

2014 |

Euronext CEO steps down |

|

August 5 |

2014 |

Information about a possible settlement with BATS relating to special order types is reported |

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.