With the S&P SPY moving back to new all-time highs, the debate over valuation levels in the stock market is heating up again. Therefore, this would appear to be a good time to continue our in-depth look at a multitude of valuation indicators.

Much of the attention last week was focused on Robert Shiller's CAPE (Cyclically Adjusted Price to Earnings) Ratio, which we reviewed last Monday. The views on what to make of this indicator vary widely. But, most analysts recognize that the CAPE Ratio is a very, very long-term indicator.

In fact, the key takeaway from the chart of the indicator (which goes back to 1900) was summed up nicely by Professor Shiller himself. Shiller wrote, "...we should recognize that we are in an unusual period, and that it's time to ask some serious questions about it."

In essence, Shiller is saying that the market, according to his view of valuation, is currently in rarefied air and that investors should take note. However, in looking at a variety of other valuation indicators, this message doesn't come through.

So, let's dig into some data...

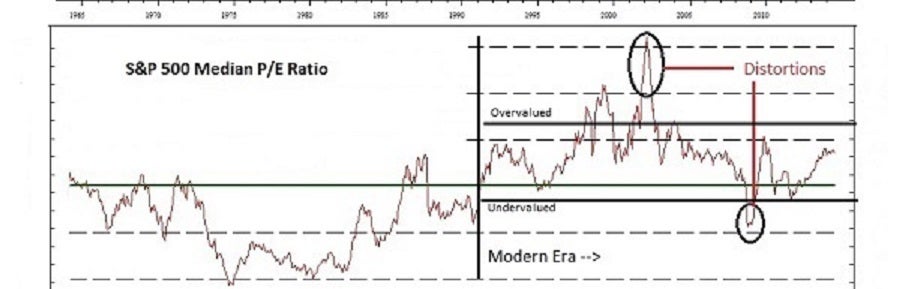

The Median P/E Ratio

The problem with using an average of the Price-to-Earnings ratio over time is that temporary distortions can have a large impact. Therefore, one alternative is to use the median of the actual 12-month trailing earnings (fully diluted for extraordinary items) of the S&P 500.

It is said that a picture is worth a thousand words, so please spend a moment with the chart below. The chart illustrates the Median P/E Ratio for S&P 500 plotted on a monthly basis from April 1, 1964 through July 31, 2014.

There are several points that can be taken away from this chart. The first, and perhaps the most important, is the fact that there are two clearly different "eras" of valuation portrayed here.

The first era took place from 1964 through 1989 - which is the left hand side of the chart. During this period, the high valuation level for the median P/E indicator was seen in 1987, with a reading around 21.

The low valuation level was down in the 6-7 range, a level that was hit in early 1975 and again in 1982. And the average for the period (the middle dashed line on the left side of the chart) looks to be somewhere around 12.

During this period, pension plans and institutions were the primary players in the market. For example, if memory serves, the total assets in ALL equity mutual funds in 1982 was less than $50 billion and total assets in all equity funds didn't exceed $1 trillion until 1989.

During this 'institutional era' the chart shows that the dashed line represented what could be called the "fair value" level for the market while the green line was clearly the danger zone and the lower dashed line suggested that stocks were bargains.

One could also argue that the middle dashed line represented an undervalued level for the S&P 500 during this time - except during the brunt of the secular bear market that occurred in 1974.

Now, if you will turn your attention to the right hand side of the chart, you will see a completely different - and significantly more complex story.

The Modern Era

The right side of the chart shows that the level of valuations from 1990 forward are dramatically different than those seen from 1964 through 1989. And yes, we could easily spend time arguing about when this "new era" for valuations began as anywhere from 1985-1990 would be acceptable. However, the key point is that the right hand side of the chart is very different from the left.

The first question is why is there such a disparity in the two time periods? The answer is likely the fact that instead of pension plans and institutional investors being the primary players in the market, as time went on it was mutual funds and hedge funds that took control of the game.

Remember, back in the day, corporations provided their employees with defined benefit pension plans. Those days are now long gone as the 401(K) plan has replaced the pension plan.

Therefore, individuals are putting more and more money into the market, with most of this cash being allocated to index funds. In short, this has created higher demand for equities over the years as new cash comes in - month after month - that needs to be put to work.

What Was Overvalued Is Now Undervalued

Regardless of your view on the reason for this change, the bottom line is that the green line on the chart - which represented an overvalued level on the S&P 500 from 1964 through 1989 - has represented an undervalued level for the past 20+ years.

Another key takeaway in looking at this or any other valuation indicator is that the really big moves that occur in the market can cause indicators to become distorted. The above chart highlights two such occurrences - in 2002 and again in 2009.

In other words, in order to make valuation indicators useful in today's wacky world, you have to make some adjustments. And in this case, it is probably a good idea to ignore the spike in the median P/E seen in 2002 and the dive of 2009 due to the fact that the readings became distorted by extreme movements in stock prices.

Generally speaking, if we eliminate the "distortions," one can argue that the range of this indicator over the last 23-25 years has been between the dashed line below the green line on the downside and the two dashed lines above the green line on the upside.

We will opine that the dark horizontal lines drawn in on this chart represent a decent range for under and overvaluation.

Where is "Overvalued" and "Undervalued" Now?

Assuming you agree with the approach/analysis presented here so far, the next question becomes, where does the market have to go from here in order to become overvalued or undervalued?

Using the over/undervaluation lines drawn on the chart shown above, we did some basic calculations using the current 12-month trailing earnings on the S&P 500 to came up with the following...

The S&P 500 would become Overvalued at 2185 or +9.4 percent from Friday's close (and would become "very overvalued" - ala 1999 - at the 2207 level).

The S&P 500 would become Undervalued at 1672 or -15.9 percent from Friday's close

It is important to recognize that if earnings continue to improve, the overvaluation levels listed above would need to adjusted higher as well. And this is why the valuation levels are a constantly moving target.

The Takeaway

While Professor Shiller contends that the stock market is currently in "rarefied air" based on analysis of data going back to 1900, our view is that one can't use valuation metrics in a vacuum.

In short, since participation in the stock market has become more mainstream and the market moves have become more extreme over the last 25 years, one needs to make some adjustments to valuation measures in order for them to be useful.

This is NOT to say that Shiller's point is invalid. There ARE other measures (there is more to come on this topic) that suggest stocks are overvalued to some degree. However, based on adjusted, median P/Es, stocks do NOT appear to be in the "danger zone" at this time.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.