On March 11, JMP Securities released a research note updating:

- American Realty Capital Properties, Inc. ARCP

- Apollo Commercial Real Estate Finance ARI

- Columbia Property Trust CXP

Tale Of The Tape

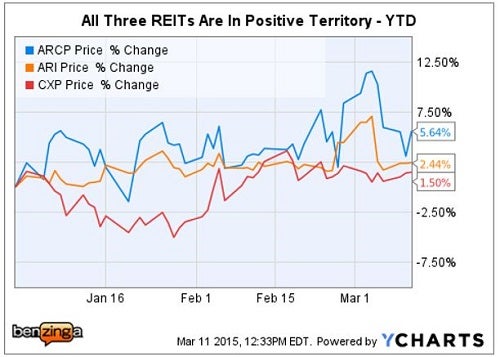

Notably, ARCP shares are down ~34 percent during the past year due to accounting woes, management shake-ups and ongoing SEC and FBI investigations.

JMP - American Realty (ARCP): Maintains Market Perform

- The big news was that ARCP has named Glenn Rufrano as its new CEO. JMP noted the Rufrano had a reputation as a "straightforward executive… with a history of shareholder value creation."

- JMP expects ARCP shares to trade positively on the news.

- However, JMP also noted that the "Non-Executive Chairman seat remains unoccupied" still represents uncertainty regarding direction.

- JMP noted that ARCP's balance sheet needs repair and that "Rufrano has shown previous acumen on the deleveraging front from his previous REIT management tenure."

- The announcement that two of the five ARCP board members "with deep ties to the previous management regime" are stepping down will help shareholders to gain a voice.

- JMP "remains on the sidelines…awaiting clarity on Rufrano's strategic plan," and maintains AFFO estimates for 2014/2015 of $0.92/$0.91, respectively."

JMP - Apollo CRE (ARI): reiterates Market Outperform

- JMP reiterated its "Market Outperform rating on shares of Apollo Commercial Real Estate Finance with an $18.50 price target based on a required 9.5% dividend yield."

- "On March 5, Apollo CRE priced a follow-on equity offering of 10.0M shares at $17.00, raising estimated net proceeds of $168.0M;" a 24.5% increase, which temporarily lowered leverage.

- JMP reduced its "2015 core EPS estimate to $1.85 from $1.90 and [JMP maintains its] 2016 estimate at $1.95."

- JMP believes "ARI shares represent an exceptional value, trading at 1.02x book value with a dividend yield of 10.5% (compared to a peer median yield of 8.1%), and… potential for a next 12-month total return opportunity of ~21%."

JMP - Columbia Property Trust (CXP): maintains Market Outperform, $27 PT

- JMP adjusted its "estimates on shares of Columbia Property Trust following yesterday's announcement that the company had priced $350M of 10-year senior notes."

- JMP pointed out that CXP "stock is cheap at 13.5x 2015 FFO (compared to the sector average of ~18x)."

- JMP's $27 PT is "derived from a blend of [its] NAV estimate ($25.50) and a 15x multiple ($28.80)."

- "The new debt is slightly dilutive to 2015 FFO/share… [JMP's] estimate declines from $1.92 to $1.89, due mostly to the timing of capital deployment, while [JMP's] 2016 FFO/share estimate decreases by a penny to $1.83."

- Columbia's "portfolio quality and location should improve materially following the next tranche of planned asset sales, which concludes the portfolio repositioning strategy."

Image credit: MarshalM20, Wikimedia

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Loading...

date | ticker | name | Price Target | Upside/Downside | Recommendation | Firm |

|---|

Posted In: Analyst ColorREITPrice TargetReiterationAnalyst RatingsGeneralReal EstateGlenn RufranoJMP

Benzinga simplifies the market for smarter investing

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.

Join Now: Free!

Already a member?Sign in

{kind=link}