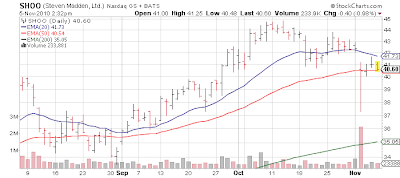

A couple of shoe related companies recently reported - I decided to go with DSW (DSW) due to better chart (and parakeet expertise) but I still like Steve Madden (SHOO) for potential expansion possibilities. [Jul 30, 2010: Steve Madden - Young Women's Shoes Apparently Recession Proof]

How can one like retail stocks in what is a relatively poor economy? Easy - the government is supporting countless Americans via transfer payments at pace never seen in history, and Americans are finding new 'innovative' ways to create cash flow such as not paying their mortgages (1 in 10 mortgage holders in the country now 'rent free'). Plus we're now headed back to an era of cheap financing, as 0% car loans are back en vogue and zero down mortgages are being backstopped by the government. [Sep 10, 2010: Zero Down Mortgages Restarted by Biggest Subprime Lender in Town - Fannie Mae] (We all win - again, except for the taxpayer!) [Jan 5, 2010: WSJ - The Treasury Department's Christmas Eve Masscare of the US Taxpayer] Combine that with the upper 20 to 33% strata who are still doing well in safe, secure jobs or those in federal government and you can make a bull case. Oh yes, don't forget once we pay down our debt... errr, walk away from it, we can start the cycle anew! [Jun 15, 2010: Default, not Thrift Pares U.S. Debt] We've learned a lot from the past 3 years!

Circling back to our national strategic default obsession - as I wrote earlier this year, the longer the foreclosure flushing cycle takes to complete in this country (and it this pace we're talking 5 years more to go) and the longer we kick the can, we actually have a positive for consumption spending - 7 million+ households are not making $1200, $1300, $1400 mortgage payments so that can go into travel, shoes, cars, Apple products, massages, dinners out on the town, whatever they wish to buy while they live rent free. [Jun 2, 2010: (Even More) Anecdotal Benefits of Strategic Default] Frankly I'll get bearish once the cycle is over and all Americans are once again "forced" to pay for a roof over their head. [Apr 13, 2010: One out of Ten US Mortgages is Now Delinquent ... Which is Great for Consumer Spending]

It is all essentially a ponzi based on the federal government's ability to print, borrow, deficit spend, and flush money out to people people who used to be able to support themselves the old fashioned way - i.e. good paying jobs. It is our new American prosperity - no use complaining about it anymore; the Fed is now supporting it full bore with it's plan to effectively fund the majority of next year's deficit. And I assume QE3 will fund the next year's... So we're a country that cannot exist anymore without easy money.... but no worries, money from the heavens is headed our way from every angle - after all we deserve it being the chosen ones. [Jun 3, 2009: A Country that Cannot Function Without Easy Money]

This "bullish" view on part of the US consumer contrasts to my views in 2007 when I hated all aspects of consumer consumption [Apr 14, 2008: Stuff I've Been Negative on Since Fall 2007] because of what I saw as the coming "Big One" as the 2004-2007 house ATM ended and the 70% of Americans who lived paycheck to paycheck would find their new reality. [Dec 3, 2009: Debt to Income Ratio Essentially Doubles for all American Households in Past 2 Decades] My old view?

That was also an era when Americans still thought they had to pay their mortgage .... but we are in a new era - it's morning in Cramerica. [May 4, 2010: Strategic Defaults in Q1 2010 Rise to One Third of All Foreclosures v One Fifth a Year Ago] Now we run up our debt, then walk away from it.... with our hand out to the government along the way.* (remember to blame the banks for forcing you into the debt, pass Go, collect $200 - from the federal government) The old house ATM is replaced by the government ATM plus the house ATM 2.0 (just don't pay and live 18-26 months extra of the good life) Screw the banks who "forced you to take out that mortgage you could not afford, and forced you to cash our refinance 3x to go on the vacations and get the granite countertops and new cars". Hence we have to change our view! That said I do prefer either the high end, [Oct 8, 2010: No Recession in High(er) End Retail] or the low end - the middle, not so much as many are disappearing and joining the low end.. Plus the inflation in 'things we need' pressures the middle the most, as they receive less in government handouts to make up for it.

* yes, not all of us do this - the responsible are punished under this scenario by not 'playing the system'.

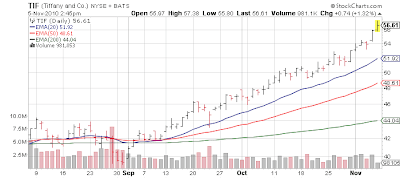

For example.... here is the perfect high end name, with the additional benefit of foreigners coming into the U.S. and able to use their superior currencies to buy product priced in U.S. dollars on the cheap. Aside from that group of buyers, the flagship NYC store caters to the financial oligarchy which has now become backbone of U.S. society. (must be protected at all costs, using taxpayers as funding and backstop) So you have the perfect company for a society catering to financiers, whose central banker's sole goal is supportingthat niche of financial innovators all the good people of America, and devaluing the currency. [Mar 31, 2010: Ben Bernanke Content to Sacrifice American Savors to Recapitalize Banks and Benefit Debtors]

So you want me to make a bear case for retailers in this economic ponzi nirvana? No way Jose! If you take away the Fed & government support for all aspects of American consumption and combine that with Americans returning to the belief they actually have to pay down their debts, I'll reconsider. But that is so 1996.

------------------------------

But I digress. Specific to shoes - look, I'm male and I don't understand the fetish but for a woman it appears to be something akin to beer, sports, video games, and Maxim magazine, all combined into 1 product. So women will find room in their budget for this niche, along with those handbags.

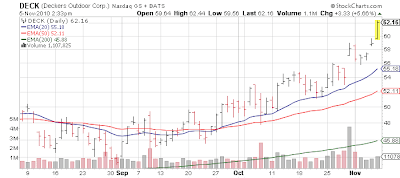

The "momo" name in this group the past few years is Deckers (DECK) which is the Netflix of shoes... apparently those Uggs never do go out of style.

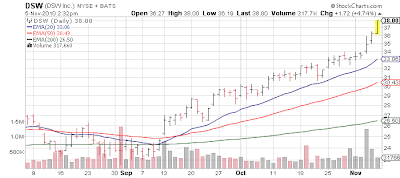

But for today, I'll focus on the 2 names at the top of the piece. First the one we bought yesterday AM... DSW which is a pure play retailer (i.e. a reseller of products others make).

DSW Inc. is a leading branded footwear specialty retailer that offers a wide selection of brand name and designer dress, casual and athletic footwear for women and men. As of November 3, 2010, DSW operated 313 stores in 39 states and operated an e-commerce site, www.dsw.com. DSW also supplied footwear to 351 leased locations in the United States

Estimates were for 47 cents; they came in with a solid beat at 52 cents. Same store sales rose 10%. Analysts are in for $2.00ish for the year end (Jan 2011), but DSW just raised it to $2.20 - $2.30. I still find that pricey around 17-18x forward PE but valuation is just a state of mind in the new paradigm Fed backstopped market. Zoom zoom zoom....

Recent report here

Via Reuters:

Steve Madden designs, sources and markets fashion-forward footwear and accessories for women, men and children. In addition to marketing products under its owned brands including Steve Madden, Steven by Steve Madden, Madden Girl, Betsey Johnson, Betseyville and Big Buddha, the Company is the licensee of various brands, including Olsenboye for footwear, handbags and belts, Elizabeth and James, l.e.i. and GLO for footwear and Daisy Fuentes for handbags.

Market News and Data brought to you by Benzinga APIsHow can one like retail stocks in what is a relatively poor economy? Easy - the government is supporting countless Americans via transfer payments at pace never seen in history, and Americans are finding new 'innovative' ways to create cash flow such as not paying their mortgages (1 in 10 mortgage holders in the country now 'rent free'). Plus we're now headed back to an era of cheap financing, as 0% car loans are back en vogue and zero down mortgages are being backstopped by the government. [Sep 10, 2010: Zero Down Mortgages Restarted by Biggest Subprime Lender in Town - Fannie Mae] (We all win - again, except for the taxpayer!) [Jan 5, 2010: WSJ - The Treasury Department's Christmas Eve Masscare of the US Taxpayer] Combine that with the upper 20 to 33% strata who are still doing well in safe, secure jobs or those in federal government and you can make a bull case. Oh yes, don't forget once we pay down our debt... errr, walk away from it, we can start the cycle anew! [Jun 15, 2010: Default, not Thrift Pares U.S. Debt] We've learned a lot from the past 3 years!

Circling back to our national strategic default obsession - as I wrote earlier this year, the longer the foreclosure flushing cycle takes to complete in this country (and it this pace we're talking 5 years more to go) and the longer we kick the can, we actually have a positive for consumption spending - 7 million+ households are not making $1200, $1300, $1400 mortgage payments so that can go into travel, shoes, cars, Apple products, massages, dinners out on the town, whatever they wish to buy while they live rent free. [Jun 2, 2010: (Even More) Anecdotal Benefits of Strategic Default] Frankly I'll get bearish once the cycle is over and all Americans are once again "forced" to pay for a roof over their head. [Apr 13, 2010: One out of Ten US Mortgages is Now Delinquent ... Which is Great for Consumer Spending]

It is all essentially a ponzi based on the federal government's ability to print, borrow, deficit spend, and flush money out to people people who used to be able to support themselves the old fashioned way - i.e. good paying jobs. It is our new American prosperity - no use complaining about it anymore; the Fed is now supporting it full bore with it's plan to effectively fund the majority of next year's deficit. And I assume QE3 will fund the next year's... So we're a country that cannot exist anymore without easy money.... but no worries, money from the heavens is headed our way from every angle - after all we deserve it being the chosen ones. [Jun 3, 2009: A Country that Cannot Function Without Easy Money]

This "bullish" view on part of the US consumer contrasts to my views in 2007 when I hated all aspects of consumer consumption [Apr 14, 2008: Stuff I've Been Negative on Since Fall 2007] because of what I saw as the coming "Big One" as the 2004-2007 house ATM ended and the 70% of Americans who lived paycheck to paycheck would find their new reality. [Dec 3, 2009: Debt to Income Ratio Essentially Doubles for all American Households in Past 2 Decades] My old view?

I cannot continue to stress enough how wrong analysts are on 2008 estimates and any company with focus on the US consumer is simply going to be blown apart in due time - if not this earnings season - then in the future. We are told daily how "cheap" these stocks are; this is based on the fictional body of work called "analysts 2008 estimates". Don't believe the hype. The subprime nation (us) is in trouble. Consumers make 70% of GDP. Its a consumption culture where the consumer is being drowned in negative wealth effect from housing, inflation from the Federal Reserve/global forces, and underemployment if not outright unemployment.

People were asking me for individual names for shorts - I continue to stress the same themes I've stated since last summer - anything consumer related or based on American conspicuous consumption. We're heading into a long, drawn out recession. consumption - it will all go. .. I've said it since last summer and as each month/week/quarter passes more denial will turn into acceptance and more earning cuts will have to happen across the board. The people in denial rely on government reports, which are for the most part another pile of fiction work.

That was also an era when Americans still thought they had to pay their mortgage .... but we are in a new era - it's morning in Cramerica. [May 4, 2010: Strategic Defaults in Q1 2010 Rise to One Third of All Foreclosures v One Fifth a Year Ago] Now we run up our debt, then walk away from it.... with our hand out to the government along the way.* (remember to blame the banks for forcing you into the debt, pass Go, collect $200 - from the federal government) The old house ATM is replaced by the government ATM plus the house ATM 2.0 (just don't pay and live 18-26 months extra of the good life) Screw the banks who "forced you to take out that mortgage you could not afford, and forced you to cash our refinance 3x to go on the vacations and get the granite countertops and new cars". Hence we have to change our view! That said I do prefer either the high end, [Oct 8, 2010: No Recession in High(er) End Retail] or the low end - the middle, not so much as many are disappearing and joining the low end.. Plus the inflation in 'things we need' pressures the middle the most, as they receive less in government handouts to make up for it.

* yes, not all of us do this - the responsible are punished under this scenario by not 'playing the system'.

For example.... here is the perfect high end name, with the additional benefit of foreigners coming into the U.S. and able to use their superior currencies to buy product priced in U.S. dollars on the cheap. Aside from that group of buyers, the flagship NYC store caters to the financial oligarchy which has now become backbone of U.S. society. (must be protected at all costs, using taxpayers as funding and backstop) So you have the perfect company for a society catering to financiers, whose central banker's sole goal is supporting

So you want me to make a bear case for retailers in this economic ponzi nirvana? No way Jose! If you take away the Fed & government support for all aspects of American consumption and combine that with Americans returning to the belief they actually have to pay down their debts, I'll reconsider. But that is so 1996.

------------------------------

But I digress. Specific to shoes - look, I'm male and I don't understand the fetish but for a woman it appears to be something akin to beer, sports, video games, and Maxim magazine, all combined into 1 product. So women will find room in their budget for this niche, along with those handbags.

The "momo" name in this group the past few years is Deckers (DECK) which is the Netflix of shoes... apparently those Uggs never do go out of style.

But for today, I'll focus on the 2 names at the top of the piece. First the one we bought yesterday AM... DSW which is a pure play retailer (i.e. a reseller of products others make).

DSW Inc. is a leading branded footwear specialty retailer that offers a wide selection of brand name and designer dress, casual and athletic footwear for women and men. As of November 3, 2010, DSW operated 313 stores in 39 states and operated an e-commerce site, www.dsw.com. DSW also supplied footwear to 351 leased locations in the United States

Estimates were for 47 cents; they came in with a solid beat at 52 cents. Same store sales rose 10%. Analysts are in for $2.00ish for the year end (Jan 2011), but DSW just raised it to $2.20 - $2.30. I still find that pricey around 17-18x forward PE but valuation is just a state of mind in the new paradigm Fed backstopped market. Zoom zoom zoom....

Recent report here

Via Reuters:

- DSW Inc's (DSW) quarterly sales trumped market expectations as the shoe retailer continued to lure bargain-hungry customers in a weak spending climate and it raised its 2010 earnings outlook for the third time this year.

- DSW, which sells branded footwear for men and women at discounted prices, raised its 2010 earnings outlook to $2.20-$2.30 a share, from its prior view of $1.80-$1.95 a share.

- Analysts on average were expecting earnings of $1.98 a share for the year, according to Thomson Reuters I/B/E/S.

- The Columbus, Ohio-based company also expects a rise in its annual comparable store sales of about 11 percent, up from its prior view of about an increase of 7-9 percent.

- Sales rose 10 percent to $489.3 millionfor the quarter ended Oct. 30, while comparable store sales also rose about the same during the period.

-----------------------

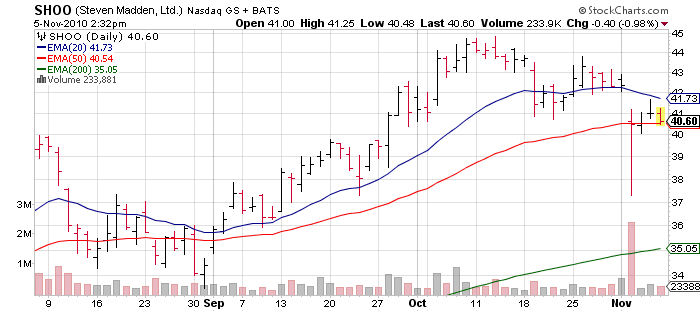

Steve Madden (SHOO) also had nice results, but due to some margin pressure the stock has been hit. This is potentially a far more interesting company than DSW as it is not a pure play retail outlet (82 stores), but a wholesaler and designer - however that carries more risk.

Estimates were for 77 cents, and the company did 81. The company also raised guidance but the gross margin issue has hit the stock. (but operating margin stayed flat at 20.3%) Full year is at $2.60 so the stock is actually priced nicely around $40 for this solid level of growth at 15x forward. Same store sales in their own outlets was 15.7%.

Right now is hit or miss in terms of next steps on the chart - right at support. This market is all about chasing momentum, so the algos are running into DSW despite the superior growth characteristics AND cheaper valuation in SHOO. That said, as it expands its branding to new products, the Street is probably wary.

Recent report here.

Via Reuters:

- Shoemaker Steven Madden (SHOO) reported weak gross margin in the third quarter, hurt by higher markdowns and a shift in its wholesale mix towards lower-margin products, sending its shares down 11 percent.Gross margin in the quarter fell to 42.1 percent from 44 percent in the year-ago quarter. Apart from the shift in product mix, margins were also affected by an increase in off-price sales of underperforming products in its wholesale segment.

- "Though the results beat the Street's expectations, the gross margins were lower than the Street expected. The shares might be down because of low gross margins," Capstone Investments analyst Claire Gallacher said.

- However, strong sales helped the company's third-quarter results beat analysts' estimates, and it raised its profit outlook for the year.

- For the July-September quarter, the company, which primarily sells to 12-to-25-year-old girls, earned $22.9 million, or 81 cents a share, compared with $17.8 million, or 64 cents a share, a year ago. Sales rose 31 percent to $184.1 million.

- Analysts on an average were expecting earnings of 77 cents a share, on revenue of $170.8 million.

Specific to the gross margin issue:

- Gross margin was 42.1% in the third quarter as compared to 44.0% in the comparable period of 2009, reflecting a decline in the wholesale segment gross margin partially offset by margin improvement in the retail segment.

- Gross margin in the wholesale business decreased to 38.8% in the third quarter from 41.2% in the prior year's third quarter driven by (i) mix shifts, including the growth of the international business and the inclusion of the results of the Company's footwear business with one its mass merchant customers in the sales line and (ii) an increase in off-price sales.

- Retail gross margin increased to 58.1% for the third quarter from 55.2% in the comparable period of the prior year as a result of strong full-price selling and reduced discounting.

Bit of a bump in guidance:

- For fiscal 2010, the Company now expects net sales will increase 24% – 25% compared to fiscal 2009. Diluted EPS is expected to be in the range of $2.57 – $2.62. This compares to previous guidance of diluted EPS in the range of $2.45 – $2.55.

Long the American consumer ex-the responsible ones, long DSW in fund; no personal position

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Loading...

Benzinga simplifies the market for smarter investing

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.

Join Now: Free!

Already a member?Sign in