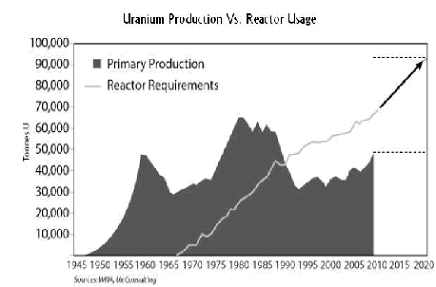

- We use more than we produce

- And prices are on the rise

- How to invest today

Right now, we're using more uranium than we produce.

The result? Prices have already started to

rise:

Right now, we're using more uranium than we produce.

The result? Prices have already started to

rise:  Just a few months ago, uranium sold for $40 a pound. Today, prices

are homing in at $60 a pound. Of course, if you

look at the chart above, you'll see that prices were much, much higher in

2007. I think we'll see higher uranium prices

for years to come. And there's no more obvious way to profit from higher

uranium prices than to buy the world's largest uranium producer.

As I wrote on August 31st:

Just a few months ago, uranium sold for $40 a pound. Today, prices

are homing in at $60 a pound. Of course, if you

look at the chart above, you'll see that prices were much, much higher in

2007. I think we'll see higher uranium prices

for years to come. And there's no more obvious way to profit from higher

uranium prices than to buy the world's largest uranium producer.

As I wrote on August 31st:

“My recommendation is simple. One company currently produces the lion's share of uranium: Cameco Corp. CCJ. They own the world's largest uranium mine which provides about 17% of the world's uranium every year. No other mine even comes close.

I fully expect this company to multiply gains made in the price of uranium. I'd suggest buying this company now, today, and holding it for at least ten years. I firmly believe that there isn't a safer way to get rich from commodities today than to buy this company.”

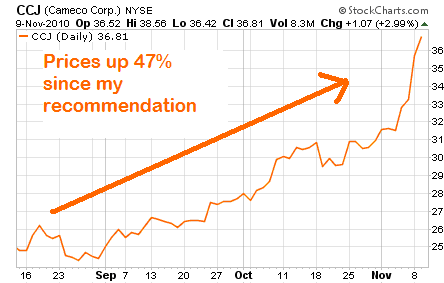

As of my recommendation, the stock is up nearly 50%: Like many commodity based stocks (and stocks in general) CCJ went

on a hell of a run the past few months. To that

end, reader Matt I. wrote in and asked a very good question.

“Hi Kevin. Do you think CCJ is still a buy? Thanks

– Matt”

Like many commodity based stocks (and stocks in general) CCJ went

on a hell of a run the past few months. To that

end, reader Matt I. wrote in and asked a very good question.

“Hi Kevin. Do you think CCJ is still a buy? Thanks

– Matt”

When I recommended buying CCJ, it was selling for about 10 times earnings. Right now, it's closer to 15 times earnings, so it's still not extremely expensive.

I still believe this company is a great buy-and-hold for the next 10 years, and while I'm sure we'll see some sort of correction in the coming months – I still think this company is a great buy.

Despite a weaker third quarter (earnings fell 16% year-over-year) the rising price of uranium has moved this company's stock higher.

There are two easy to understand factors that influence CCJ's profitability:

1. volume of sales

2. price of uranium

So, I'd consider this company a buy as long as the above two trends are expected to rise (they are) AND the company sells for less than 20 times earnings.

If you have any questions about specific uranium companies, please send them my way: editorial@resourceprospector.com.

Good investing,

Kevin McElroy

Editor

Resource Prospector

disclosure: no position in Cameco as of this publication

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.