Stocks ended a largely winning week with choppy action on Friday as investors seek more clarity in coming sessions from a volatile oil market, the interest rate outlook, and the health of Q1 earnings results.

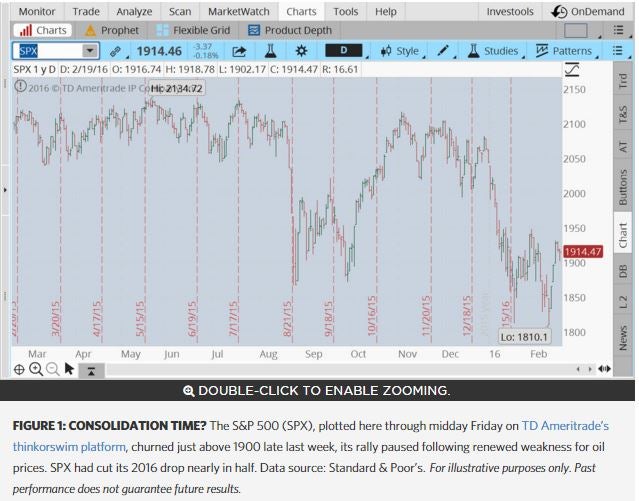

Despite Friday’s push and pull, major stock indexes booked solid weekly gains, boosted by a three-day rally earlier in the week that was their first three-day winning streak this year. The S&P 500 (SPX), in figure 1, staged a recovery from hitting its lowest mark since April 2014. The S&P 500 had cut its 2016 decline nearly in half, though it’s still down more than 10% from a May record and about 6% this year amid signs of weakness in the global economy and falling commodity prices. The tech-heavy NASDAQ Composite had drawn within 1% of tipping into bear-market territory before its rebound.

Still Stuck on Oil. Friday’s oil news reminded market participants that the link between the commodity and the stock market remains tight. Oil fell some 2% at one point after data showed that U.S. oil inventories rose once again and Saudi Arabia ruled out a production cut. Oil is likely to continue to weigh heavily on the stock market’s mood in coming days.

Retail Earnings Hit in Tough Climate: The Home Depot, Inc. HD and Macy’s Inc. M are due to report earnings results pre-open on Tuesday. Lowe’s Companies, Inc. LOW and Target Corporation TGT issue their figures pre-open on Wednesday. The Gap, Inc. GPS reports after the market close on Thursday. JC Penney Company JCP issues its quarterly snapshot before the market open on Friday. Although each report should be scrutinized for company-specific news, there is some sector-wide uncertainty heading into the retail-heavy week after two retail names disappointed with their results. Nordstrom, Inc. JWN reported weaker-than-expected sales after a tough holiday season. Wal-Mart Stores, Inc. WMT reported weak quarterly sales and cut its forecasts for the year. Traditional retailers continue to look for new ways to compete with online e-commerce giant Amazon.com, Inc. AMZN and others.

Fed Watch Continues: Stocks continue to sway to the sound of Fed commentary. Gains last week in large part followed indications from Federal Reserve chief Janet Yellen that the bank panel could slow down its rate-hike campaign given economic volatility around the globe. Yellen also touched on market turbulence. But a speech Friday from voting member, Cleveland Fed President Loretta Mester shows the debate is far from over. Mester said in a speech that she believes the U.S. economy will power though market ripples with the help of consumer spending. “I continue to monitor developments, but until I see further evidence to the contrary, my current expectation is that the U.S. economy will work through this episode of market turbulence and the soft patch of economic data to regain its footing for moderate growth, even as the energy and manufacturing sectors remain challenged,” Mester said, according to financial media covering her speech. A more persistent drop in equity markets could spill over into the broader economy, “but so far we have not seen this,” Mester added. The Fed and financial markets will take in several new snapshots of economic activity this week, starting with consumer attitudes and housing, extending to factory data, and featuring the second round of edits for Q4 GDP

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.