I've been a proponent of the auto industry for a good part of 2010 (although I missed the boat in latter 2009 and early 2010) once sales rebounded north of the 11.25M+ annual levels. As I've said many times analysts and normal folk simply did not realize how much cost (read: jobs, lower benefits, wage concessions, plant closings) have been taken out of the system. I'm starting to see recognition of this only in the past 2 months.

General Motors (GM) and Chrysler are their own specific situations as they had huge debt restructurings (major bonus go forward), and apparently the government (which was supposed to be in a position of power when negotiating) gave GM the Christmas gift of $45-$50 BILLION of profits tax free go forward. Boggling. Ford (F) does not have that benefit but has the advantage of a proven management team, and the current superstar in the space in management Alan Mulally. But this trend is bigger than any one man - the cost structure in both the U.S. majors and the supplier base has been completely overhauled to make the entire auto industry profitable at 11-12M annual sales in the U.S. versus 15M+. There are risks go forward in material costs (commodities) and at some point in the future the labor base is going to be in unrest seeing huge gains in the 'stockholder' and 'management' class largely due to their givebacks (which actually is a great parallel to much of the U.S. economy - especially in the public multinational corporations) but we remain in a window of good times. [Jul 27, 2010: NYT - Industries Find Surging Profits in Deeper Cuts] [Oct 20, 2009: WSJ - Slump Prods Firms to to Seek New Compact with Workers]

U.S. sales are running a bit higher than 12M+ right now in the U.S.; with any form of recovery combined with constant government handouts (on both the tax and expenditure) sides this might get to 13M+ in 2011; where profits would see another leg up - assuming commodity costs don't explode higher. Of course I am only commenting on the domestic side of business; many of these firms have exposure to the hottest economies on Earth in emerging markets as well.

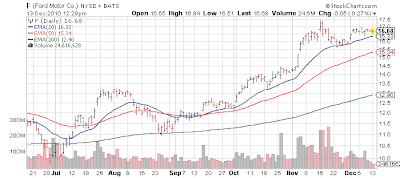

Merrill Lynch was out with a note late last week offering why Ford (F) will be headed to $24... a near 50% gain from here. They appear to think the U.S. economy is *really* back with a call for 15M in sales in 2011. Wow. If the industry does 15M, I think $24 would be conservative.... and frankly you could throw a dart at any stock in the sector and make mad money.

Via Notable Calls:

- Ford F target is raised to a new Street high of $24 (prev. $20)

As Ford F has been the recent poster boy of the Auto industry, here are the details:

Solid results should continue

Balance sheet getting stronger each quarter

Product sweet spot and common platform leverage ahead

Solid leadership at the top

[Jun 16, 2010: What to Expect from a General Motors IPO]

No position

Market News and Data brought to you by Benzinga APIsGeneral Motors (GM) and Chrysler are their own specific situations as they had huge debt restructurings (major bonus go forward), and apparently the government (which was supposed to be in a position of power when negotiating) gave GM the Christmas gift of $45-$50 BILLION of profits tax free go forward. Boggling. Ford (F) does not have that benefit but has the advantage of a proven management team, and the current superstar in the space in management Alan Mulally. But this trend is bigger than any one man - the cost structure in both the U.S. majors and the supplier base has been completely overhauled to make the entire auto industry profitable at 11-12M annual sales in the U.S. versus 15M+. There are risks go forward in material costs (commodities) and at some point in the future the labor base is going to be in unrest seeing huge gains in the 'stockholder' and 'management' class largely due to their givebacks (which actually is a great parallel to much of the U.S. economy - especially in the public multinational corporations) but we remain in a window of good times. [Jul 27, 2010: NYT - Industries Find Surging Profits in Deeper Cuts] [Oct 20, 2009: WSJ - Slump Prods Firms to to Seek New Compact with Workers]

U.S. sales are running a bit higher than 12M+ right now in the U.S.; with any form of recovery combined with constant government handouts (on both the tax and expenditure) sides this might get to 13M+ in 2011; where profits would see another leg up - assuming commodity costs don't explode higher. Of course I am only commenting on the domestic side of business; many of these firms have exposure to the hottest economies on Earth in emerging markets as well.

Merrill Lynch was out with a note late last week offering why Ford (F) will be headed to $24... a near 50% gain from here. They appear to think the U.S. economy is *really* back with a call for 15M in sales in 2011. Wow. If the industry does 15M, I think $24 would be conservative.... and frankly you could throw a dart at any stock in the sector and make mad money.

Via Notable Calls:

- Ford F target is raised to a new Street high of $24 (prev. $20)

- Sales are recovering, now with two consecutive months of a SAAR of 12.3mm, a run-rate 1mm units above the Jan-Sep '10 SAAR of 11.3mm. Merrill believes this recent acceleration in the sales pace is supportive of their above-consensus 2011 US sales forecast of 15mm units as light vehicle demand continues to recover.

- Meanwhile, inventory remains lean, and there appears to be price discipline among the OEMs, as industry average incentives are about $175 less per vehicle than peak 2009 levels. While the industry has been slowly recovering in volume and pricing, auto companies have been posting near record margins with volume levels that are still only just up from the trough. Therefore the firm is confident that further operating leverage can be achieved during the recovery in the cycle and that most stocks in the auto value chain remain undervalued by the market.

As Ford F has been the recent poster boy of the Auto industry, here are the details:

- Merrill is raising their Ford EPS estimates in 4Q10e from $0.45 to $0.48, in 2011 from $2.25 to $2.40, and in 2012 from $2.40 to $2.55. They are also increasing their price objective from $20 to $24, which is based on a P/E of 10X our 2011e. In their view, Ford's stock should continue to outperform for a number of reasons, including, strong management, solid operating results, a consistently improving balance sheet, industry-leading product, and recovery in the U.S. sales cycle.

Solid results should continue

- Ford's financial performance over the past year has been impressive, with LTM EPS of $2.05 and automotive cash flow generation of ~$6.5bn. Merrill expects the company to continue generating solid pre-tax profits in North America and in Ford Motor Credit, and stable/improving international performances to bolster results.

Balance sheet getting stronger each quarter

- Ford has made meaningful progress in shoring up its balance sheet, and they expect further improvement ahead. Merrill's current estimates imply that Ford will be comfortably net cash positive in 2011 and FMCC remains significantly over capitalized, which should drive higher value for shareholders.

Product sweet spot and common platform leverage ahead

- Merrill believes Ford is entering the sweet spot of its product cadence in MY11-MY14 (please see Car Wars 2011-2014 for further detail). They are forecasting an annual U.S. replacement rate of ~30% for Ford during this timeframe, and expect greater use of common platforms/parts to drive significantly lower engineering costs.

Solid leadership at the top

- It is difficult to measure the short-term success of a management team in the automotive industry, as so much is dependant upon the economic cycle. However, we believe Alan Mulally has led Ford through what is likely the worst of the downturn, and has positioned the company for success as volumes recover.

[Jun 16, 2010: What to Expect from a General Motors IPO]

No position

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Loading...

Benzinga simplifies the market for smarter investing

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.

Join Now: Free!

Already a member?Sign in