Debt happens to many people, but some face a debt situation unlike the "average" graduate who carries loan debts and has a plan for paying them off, or the homeowner who has a mortgage payment and a car loan.

Seemingly insurmountable debt, however, is a different beast.

This debt is the debt that leaves the indebted choking for air at the end of the month, wondering where the next decent meal will come from and anxiously avoiding unknown callers out of fear the voice on the other end will be a debt collector.

Various reasons have led to this situation, from poor choices to terrible circumstances. These individuals may have found themselves having previously filed bankruptcy, but back in the same situation and unable to file again for a few years. Others facing this type of suffocating financial hardship have experienced loss or oppressive medical expenses.

However, there is hope.

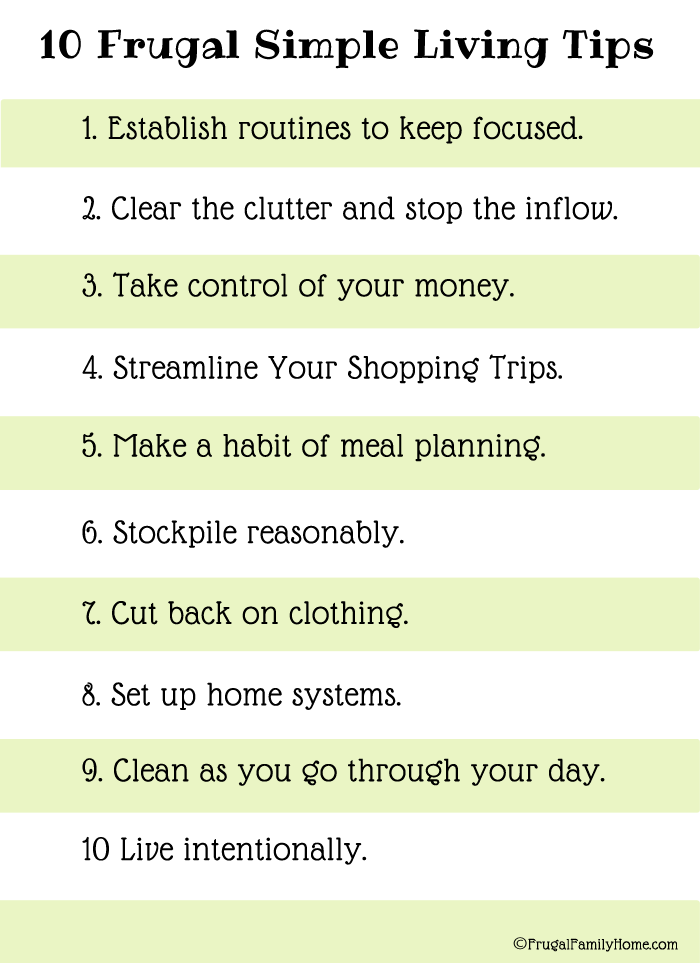

Make A Plan

Realistically assess how much debt you have and where the debt originated. Decide which sources of your crippling debt deserve immediate attention and focus on eliminating those first. Look at overall cost, interest rates and penalties when deciding which to prioritize.

Make sure that your monthly payments are covering more than the monthly interest rates. It's possible, and actually quite a common occurrence, that the minimum monthly payments will not even cover the incurred monthly interest rates — that's right; each month, even if you pay on time, your bill just keeps growing.

Look At Needs Vs. Wants And Stop Feeling Entitled

Remember, you do not deserve luxuries. Life does not owe you anything. Keep your chin up, your nose down and stop comparing your way to stability with others' financially stable lifestyles.

Don't feel sorry for yourself. Do something about your situation. Inaction won't change anything. It's only through action that different results can arise.

Bring In More Money

Live Minimally. Clear out your home and get rid of things you don't use or need. Have a garage sale. Sell back to a second-hand store, thrift store or antique store. List items on Craigslist or in the classified ads or other neighborhood sites. Sell on eBay or Amazon. Have two TVs? Sell one. Have an extra freezer taking up space and using electricity? Sell it. An extra bedroom set that's just taking up space? Get rid of it. DVDs? Books? CDs? Records? Video games? You know what to do. Absolutely gut the unnecessary items and use the funds from selling them to go toward your debt and only toward your debt. Don't use even $10 to "treat" yourself for a job well done. Your sole purpose is to reduce that debt.

Other Ideas:

Other Ideas:

- Cash in rebates.

- Collect cans, metal scraps and bottles.

- Pick up change found on the ground.

- Save on stamps by hand-delivering bill payments or paying online (see "Keep Cutting" section regarding Internet usage).

- Pick up odd jobs or a part-time job. Even if it's just one day a month, a few extra dollars — when allocated responsibly — can add up over the course of months, years and decades.

Keep Cutting

1. Cutting Your Bills- Call each of your billers and ask about reducing the costs.

- Ask yourself how each can be minimized throughout the month and make a commitment to seeing that number decrease from previous levels.

- Switch name brands to store brands, cut coupons, combine coupons with weekly sales/store loyalty programs.

- Make sure to research and write a list before you leave your house. Look at using natural cleaners (vinegar, lemon, baking soda, etc.) for your basic cleaning needs. These options are much cheaper than purchasing a bottle of kitchen counter cleaner and a bottle of shower cleaners and a bottle of tile cleaner, etc. Even better, the previous generations' concoctions work just as well (if not better!), and they just cost pennies to the dollar.

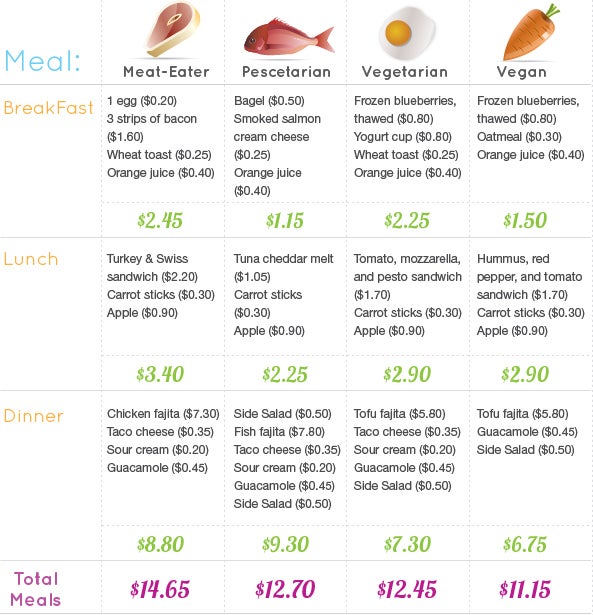

- Plan all of your meals and only purchase what you will need. Remember that meat is expensive and so are junk foods and unhealthy beverages. Clean eating will help keep your body lean as you learn to love living on the skinny.

- Use GasBuddy to find the cheapest gas in your area. If you've cut internet/smartphones, go to your neighborhood's library to check up on gas prices and plan where you'll fill up.

- Cut utility costs around the home by unplugging when not in use. Adjust your thermostat and use fans in the summer and wear an extra layer in the winter. Even a few degrees' difference can make a difference.

- You have to be meticulous. Assign a purpose to every dollar at the beginning of the month. Keep up with every quarter that is spent. Account for everything. Learn how to budget. Don't just go through the tips and tricks and think going through the motions monotonously will get you out of debt and keep you out of debt. Living a life of frugality is an active pursuit, not a passive hobby.

Get Help

No, your options aren't limited to expensive financial aids or personal assistants. Check with local government agencies to get utility bills reduced, apply for food stamps, locate food pantries, etc. Sometimes pride gets in the way, but it's better to seek and accept help than keep increasing your debt. Remember that asking for help and graciously, humbly accepting it does not mean you lack financial responsibility.

You have to ask the hard questions: Can I afford my living situation? Do I need to downsize?

Can I afford to not make these sacrifices?

If you aren't willing to make the hard, but necessary choices, you don't want it enough. Stop the cycle of self-pity and accept your current situation.

You can't say you're on the brink of poverty with no way to escape if you are watching cable on your flat screen after driving home in your vehicle that still has a note on it as you order delivery for dinner. Climbing out of sub-terrain debt is no easy feat; it's near impossible. Yet, treating it as such will not lead to a different set of circumstances. But, with unprecedented dedication, you can succeed.

You cannot take an apathetic stance or passively ignorant attitude toward deep debt. If you truly want to escape the yo-yo debt cycle, your conviction must be centered on absolute change and indomitable reserve. Face each difficult decision with a tenacity you've never embraced before and stubbornly prove statistics wrong. Make an obstinate choice toward lasting financial independence.

It's not glamorous to get your life together, but a few years of really cutting back on any/all luxuries can set you up for success later on down the road and keep you off the street/out of shelters.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.