Long term investors should remain bullish on oil and natural gas investments, regardless of the short-term implications of what's going on in Libya right now.

But that story is grabbing headlines and is the catalyst that most people believe is behind oil's ascent to $100 this spring. I'm not going to spend a bunch of time de-bunking that myth, and proposing all the long-term reasons I believe oil will continue to move higher in coming years. If you've read my articles before, you already know why.

Rather, today and tomorrow I'll discuss two companies with proven track records in the oil and natural gas services sector that are a good value. Without any clear alternative to oil and natural gas for decades to come, services companies should also prosper since they help bring the energy sources to market.

Both of these companies are involved in the production process, and both provide the services necessary when accidents happen.

Today I'll focus on Carbo Ceramics (NYSE: CRR), a company that specializes in the horizontal drilling used to bring oil and gas deposits out of shale.

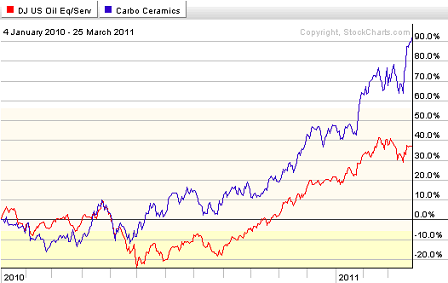

Carbo has handily outperformed the Dow Jones U.S. Oil Equipment & Services Index since the beginning of 2010, rising over 90 percent.

Carbo Ceramics isn't on a lot of traders' radar screens because it's thinly traded, averaging just over 260,000 shares traded daily. That's not a lot for a $3.1 billion market cap company.

Carbo is the world's largest producer of ceramic proppant (a granular material) used in the hydraulic fracturing process. Sales in 2010 were $473 million, an increase of 38 percent year over year. Net income was $78.7 million, an increase of 49 percent. Earnings per share came in at $3.40, compared with $2.27 in 2009.

Proppant helps facilitate hydraulic fracturing of sedimentary rock, making the process of extracting the oil, or gas, more efficient and keeping the wells operating longer and for cheaper. Carbo Ceramics makes its ceramic proppant at three U.S. plants and two more in Russia and China. Over the past decade, sales volume has tripled, keeping its plants operating at capacity.

The company also provides other services, including spill prevention and containment through its Falcon Technologies subsidiary, acquired in 2009.

This year the company's earnings are expected to grow an impressive 27 percent over 2010, and by 62 percent by the end of 2012.

With a forward P/E of 24 and a five-year PEG ratio of 1.25, investors might find Carbo a little pricey. But Carbo Ceramics is growing rapidly, and pays a dividend yielding 0.6 percent. The company has a history of regularly raising this dividend.

As the search for oil and natural gas continues, both onshore and offshore, Carbo Ceramics should continue to be a strong performer.

Further Reading: Small Cap analyst Tyler Laundon is bullish on European natural gas exploration and development companies. In Europe, natural gas prices are more than double those here in the U.S., in large part because of huge dependence on one country's natural gas production. To educate investors on how Europe plans to diversify its natural gas supplies, and how to profit on the move, Tyler and I recently released a research paper covering the opportunity. Find out how Europe plans to cut its addiction to Russian natural gas here.

Disclosure: None

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.