Japan's nuclear disaster probably set back the world's push toward nuclear-powered electric generation by years. Instead of huge nuclear energy expansion, which had been planned, we're likely going to see more nations stick with tried-and-true coal-fired electric plants, along with further expansion into natural gas.

Today we'll look at one of the largest U.S. coal producers, a company whose stock offers investors a tremendous value play. Despite its size, you've probably never heard of this company.

The U.S. is not alone in its sudden change of direction on energy. Germany's taking a hard look at its nuclear plants. Both of these developed nations will need alternative (to nuclear, that is) power generation methods. Outside of Japan, other countries in Asia, as well as India, want more of our coal as their economies expand.

To meet this demand from Pacific Rim nations, our nation's third-largest coal producer is ready to step up production - without putting a dent in supplying domestic needs. That company is Cloud Peak Energy CLD.

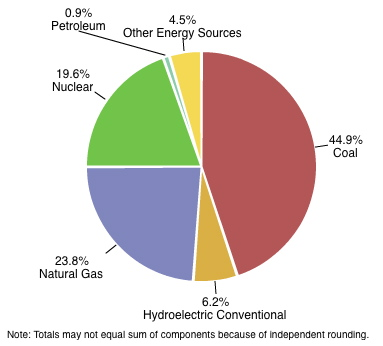

***America is essentially the Saudi Arabia of coal production, and we're sitting on reserves that will last centuries. As this Department of Energy graph shows, nearly half of our electricity came from coal-powered plants last year.

Coal power is what Cloud Peak Energy provides. The company is the only pure coal play in the Powder River Basin, and it's one of the largest producers in the region. It produces coal from just three mines in Wyoming and Montana.

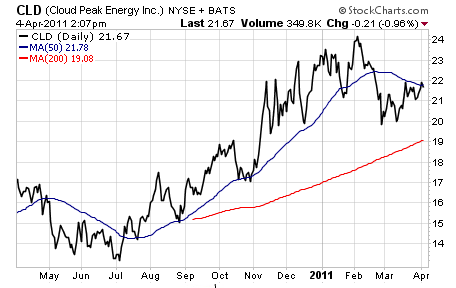

Cloud Peak's share price rose 60 percent in 2010, but after reporting higher-than-expected fourth-quarter expenses, and issuing a conservative outlook for 2011 because of production costs, the stock is down nearly 9 percent year to date.

For anyone interested in a top-quality U.S. coal stock, this sell-off in shares presents a buying opportunity.

Since its spinoff from mining giant Rio Tinto plc RIO in late 2009, Wyoming-based Cloud Peak Energy has been profitable. This company, with a market cap of $1.3 billion, just reported full-year earnings per diluted share of $0.98, compared with $6.49 in 2009. The 2010 profit was cut by charges, while 2009 was inflated by one-time adjustments.

This variability is unlikely to continue as Cloud Peak becomes a more established independent company.

Revenue was down about 2 percent in 2010, to $1.37 billion, when the company reported production of 93.8 million tons of coal. This is expected to increase slightly in 2011 - but that amount is largely sold already.

Cloud Peak, which has a current capacity of 100 million tons per year, has contracts to sell 70 million tons in 2012.The company controls 970 million tons of proven and probable Powder River reserves. Theoretically it could run out in 10 years, but the company is likely to expand its holdings in this most prolific coal-producing region to meet rising demand. That means investors should look for expanding production capacity as a catalyst for the stock's price.

***A key metric in coal mining is gross margins per ton and for 2010 Cloud Peak Energy reported a much improved gross margin of $3.75, compared with $2.96 the year before, and $1.89 in 2009.

The stock is undervalued based on some measures. It is trading below its 50-day moving average of $21.76, and carries a forward P/E of just 8.8. It has a return on equity of 24 percent.

Also, the 12-month price target of $26.30 from Thomson Reuters analysts suggest greater than 20 percent upside potential from current levels.

***Unlike the coal coming out of the Appalachian region and many mines east of the Mississippi River, Powder River Basin coal has desirable low sulfur content. This is important in an age of global warming. The coal is also more accessible through surface mining of deep beds, and production costs in the region are low - hence the attractive gross margins.

Before the Japan crisis, Pacific Rim demand for thermal, or steam, coal used for power generation was expected to increase dramatically over the next decade. That's exactly the kind produced by Cloud Peak Energy. After the earthquake, I expect demand will be even stronger.

While shipping costs are high the nuclear recoil puts coal (and natural gas) back in the picture. Cloud Peak's mines are on key rail lines to reach West Coast export terminals. Spring Creek, the company's Montana mine that's closest to the coast, draws a premium price from export markets. Most notable is demand from South Korea for high-BTU coal.

With the global energy picture muddled by the Japan disaster, the old standby sources of coal and natural gas are likely to remain key energy sources for years to come. Cloud Peak Energy is one of coal's leaders, and should be on your radar screen.

Further Reading: Small Cap analyst Tyler Laundon is bullish on European natural gas exploration and development companies. In Europe, natural gas prices are more than double those hear in the U.S., in large part because of huge dependence on one country's natural gas production. To educate investors on how Europe plans to diversify its natural gas supplies, and how to profit on the move, Tyler and I recently released a research paper covering the opportunity. Find out how Europe plans to cut its addiction to Russian natural gas here.

Disclosure: None

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.