Market Overview (Member Only)

- Stocks continued their bid last week as the Dow closed at its highest weekly level in history. It closed 1.27% higher on the week, while the Nasdaq and S&P 500 rose 1.40% and 1.45%, respectively.

- Fed Chair Powell's Jackson Hole speech all but confirmed rate cuts in September. It looks like the Fed is sacrificing the Dollar on the altar of economic growth.

- Crypto and metals both look strong, but is it time to shift from the latter towards the former? More on this below.

- The Presidential race is set following the conclusion of the Democratic National Convention last week, with just 71 days until Election Day.

Stocks I Like

- Revolve (RVLV) – 38% Return Potential

What's Happening

- Revolve Group (RVLV) is an online fashion retailer targeting younger customers.

- The company brought in $1.07 billion in revenue in 2023 along with $28.15 million in earnings.

- RVLV has a high valuation. Its P/E is at 52.95, its Price-to-Sales is at 1.64, and its EV to EBITDA is at 45.31.

- From a technical standpoint, RVLV just broke out from a broadening wedge formation, which could lead to an acceleration in upside momentum.

Why It's Happening

- Revolve is capable of capturing extra premium from its customers and riding the AI wave. After all, it has always used artificial intelligence (AI) throughout its operations, and its rich trove of data gives it tremendous power to offer merchandise it knows customers want and charge full price for it.

- In the words of co-CEO Mike Karanikolas, "That fueled a strong second quarter, highlighted by a return to top-line growth and a more than doubling of our net income year-over-year. Key contributors to our strong results were significantly improved marketing efficiency and greater efficiency in our logistics costs, helped by the first year-over-year decrease in our return rate in more than three years.”

- Revolve is doing what it does best, building relationships with its loyal customers to generate engagement, and it’s still adding customers. Active customers increased 9% year over year in the fourth quarter, and total orders placed increased 3%. This demonstrates its competitive advantage in establishing strong customer relationships—which generates excess shareholder value in the long run.

- Revenue increased 3% to $282.5 million and beat the consensus at $277.2 million. International sales were also a bright spot with sales up 13% to $57.4 million.

- The company continued to deliver strong gross margins at 54%, showing the resilience of its business model, and Revolve succeeded in lowering operating expenses by cutting marketing expenditures. As a result, operating income more than doubled from $7.4 million to $16.4 million.

- RVLV has a short interest of floated around 88%. I think shorts are toast here.

- Analyst Ratings:

- BTIG: Buy

- Baird: Neutral

- Wedbush: Neutral

My Action Plan (38% Return Potential)

- I am bullish on RVLV above $20.00-21.00. My upside target is $33.00-$34.00.

- Teva Pharmaceuticals (TEVA) – 24% Return Potential

What's Happening

- Teva Pharmaceuticals (TEVA) develops and distributes generic medicines and biopharmaceutical products in the United States.

- The company made $15.85 billion in revenue in 2023, but still lost $559 million on the year.

- In terms of valuation, the company is losing out on the earnings front, but its Price-to-Sales is a solid 1.26 and its EV to EBITDA is at 19.34.

- At a technical level, TEVA is starting to emerge from an ascending triangle formation, which should lead to a continuation of the bull trend.

Why It's Happening

- Earlier this month, Teva reached an agreement with Johnson & Johnson that would allow it to launch its Stelara biosimilar, AVT04, in the U.S. market by Feb. 21, 2025. Stelara is a huge moneymaker for Johnson & Johnson, generating just under $10 billion in revenue for the healthcare giant last year. AVT04 will provide consumers with a lower-priced alternative that could help accelerate Teva’s long-term growth.

- A recent huge positive development for Teva is that it has reached a settlement on its role in the opioid crisis. The company will need to pay out over $4.3 billion in the main agreement, which covers 48 states, but those payments will be spread out over the course of 13 years. The settlement puts to bed a big uncertainty for the drugmaker, which should attract capital inflow with much lower uncertainty now.

- Aside from expanding its pipeline capacity, management is anticipating that improvements to the supply chain will help to shore up Teva’s gross margin of 43% over the next few quarters. That will be key to help the company return to profitability. If that materializes, prepare to see a face-ripping rally in its stock price.

- With the company projecting up to $2.1 billion in free cash flow for 2023, it could have plenty of room to pay down more debt this year, essentially reducing its debt load and invest more into its R&D pipeline.

- Teva Pharmaceutical is trading at a significant discount with a forward earnings multiple of 3x – making it potentially one of the best bargains in the healthcare industry right now.

- TEVA has $6 million in free quarterly cash flow.

- Analyst Ratings:

- Barclays: Overweight

- UBS: Buy

- Jeffries: Buy

My Action Plan (24% Return Potential)

- I am bullish on TEVAabove $15.50-$16.00. My upside target is $23.00-$24.00.

- Sea Ltd (SE) – 56% Return Potential

What's Happening

- Sea Limited (SE) is a digital entertainment, e-commerce, and digital financial service business based out of Singapore.

- The company produced $13.06 billion in revenue in 2023 along with $150.73 million in earnings.

- SE has a high valuation. Its Price-to-Sales is at 3.38, its EV to EBITDA is at 361.08, and its Book Value is 11.95.

- From a charting standpoint, SE is starting to breakout above resistance of an ascending triangle pattern. This could lead to higher prices in the coming weeks and months.

Why It's Happening

- After the company decided in the third quarter last year to restart growth investments, they appear to be paying off. The bottom line in e-commerce might have caused the headline earnings miss, but management also increased Shopee’s forecast for gross merchandise volume for the year to mid-20% growth, up from its initial target of the high teens. So with the gaming division showing stronger signs of recovery and Shopee’s investments yielding results in expected growth, those were really the two important things investors wanted to see.

- Sea Limited forecast double-digit revenue growth to continue for 2024. The company added that the prediction did not count a possible relaunch of Free Fire in India, a factor that bodes well for Garena given its recent struggles.

- That division has suffered since early 2022, but over the last couple of quarters, Free Fire’s numbers have stabilized and turned upward again. After daily active users bottomed out in the fourth quarter of 2023 at 528.7 million, they have grown each quarter since to reach 648 million in the second quarter, up 19% year over year.

- Overall revenue surged 23% to $3.81 billion, beating analyst estimates, while earnings per share of $0.14 under generally accepted accounting principles slightly missed estimates of $0.19. But while overall profits missed, it appears the dynamics within each division were enough to satisfy investors.

- It traded at its cheapest price-to-sales (P/S) valuation ever in January. In short, expectations were historically low, setting Sea stock up for outperformance with even just slightly encouraging news.

- Analyst Ratings:

- Barclays: Overweight

- Wedbush: Outperform

- TD Cowen: Hold

My Action Plan (56% Return Potential)

- I am bullish on SEabove $67.00-$68.00. My upside target is $130.00-$135.00.

Market-Moving Catalysts for the Week Ahead

Price and Time Are All That Matter

There was some big news on the labor market front last week, and it's very disappointing. As it turns out, the idea that the labor market was robust and creating jobs left and right was a total mirage.

The Bureau of Labor Statistics revised payroll numbers lower by over 800,000 in the past year. This means that all of the jobs gains that were posted didn't actually happen, but the markets sure behaved in that manner.

The ramifications of this are significant, especially if you're a central banker. Keep in mind that the Fed uses this data, and if it turns out to be fake, then it renders them unable to make good policy decisions. I'm not excusing what they do—I think they're behind the curve most of the time—but it does vindicate the importance of following price and time only.

What's the Central Bank to Do?

Now that it's come out that the federal government has been doing the Fed dirty on the data front, what's next for the central bank? Last week's FOMC minutes revealed that rate cuts are all but assured at the September meeting.

My concern, once again, is that the fabrication of labor data means the Fed should have been cutting months ago. Remember, we came into this year with expectations of rate cuts as soon as March, but the strength of the labor market kept pushing it back.

It's important to keep this in mind once the economy inevitably slows down again. The government loves to deflect blame over to the central bank since they're an easy target. Even so, we had a recession in 2022, so that means we're only two years removed from the last economic contraction. We should be okay for the next year or so.

More Econ Data

Fed Chair Jerome Powell all but confirmed that rate cuts are coming at the September FOMC meeting. As I've said before, I think the Fed listens to what the market wants a lot more than people give them credit for.

This week, we have more inflation data with the PCE report on Friday. I don't expect any upside surprises with commodity prices remaining as contained as they have over the past several months. In fact, we continue to see bear markets in many like grains and oil short-term.

There's also going to be a Q2 GDP revision this week on Thursday. The previous reading was 2.8%, and if it comes in lower than the previous report, it only increases the chance of a 50 basis point cut in September.

The Political Stage is Set

Now that the Democratic National Convention is over, we have our matchup for November: Donald Trump versus Kamala Harris. From an economic standpoint, one must consider an inevitable outcome: more government spending regardless of who wins.

Markets historically perform best with a split chamber in Congress and under Democrat presidents. However, some have argued that it takes time for pro-growth policies often enacted under Republican presidents to take effect, and there is some merit there too.

Currently, the Dollar is getting crushed. To me, this signals that the world doesn't have much confidence in the outcome of the election, regardless of what it may be. Remember, if stocks are bidding while the Dollar falls, it simply means that it's a function of currency depreciation. There's not a strong appetite for Dollar-denominated assets right now.

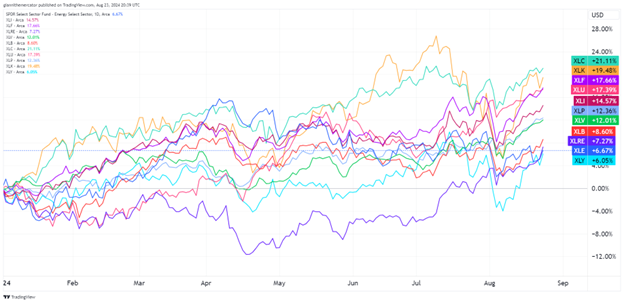

Sector & Industry Strength (Member Only)

On the sector performance front, there's not much to update over the past week. The rankings are largely the same, except for real estate (XLRE) and basic materials (XLB) overtaking energy (XLE). This should be considered as a bullish signal near-term, as XLRE was the worst-performer for much of the year.

The good news is that communications (XLC) and technology (XLK) are the top-performing sectors year-to-date. Utilities (XLU) are in third place, suggesting some caution on the economic growth front.

The spread between consumer staples (XLP) and consumer discretionary (XLY) is another concern. With XLY being the worst-performer year-to-date, there are some concerns on the consumption front, but time will tell whether rate cuts assuage this going forward.

| 1 week | 3 Weeks | 13 Weeks | 26 Weeks |

| Real Estate | Technology | Real Estate | Utilities |

Editor's Note:

Tech capturing 3-week and real estate capturing 1-week leadership is not a bearish sign.

Can Digital Rocks Make a Comeback? (Sector ETF: BTC/GLD)

A growing number of market participants have grown frustrated with the range-bound price action of cryptocurrency over the past several months. This is especially the case when you compare Bitcoin (BTC) to gold (GLD), the latter of which exhibits the strongest bull trend in markets right now.

As I periodically like to say, "When in doubt, zoom out." The longer-term ratio between BTC and GLD tells the bigger story. It broke out from the rounding bottom formation towards the end of 2023 and reestablished its bull trend.

Even with the latest correction that's been in effect year-to-date with gold outperforming Bitcoin, the trend remains upward. It looks like it's trying to bottom here, so keep an eye on this ratio because if it starts to turn up again, Bitcoin could finally come back into the picture.

Commodity-Bond Ratio Update (Sector ETF: DBC/TLT)

I'm watching the ratio between commodities (DBC) and long-term Treasuries (TLT) very closely right now. For the longest time, I had a rectangle formation drawn on the chart, which would have implied a continuation of the bull trend higher, but now, things could be changing.

Instead, I think we could be grappling with a potential rounding top pattern. This could be a very profound macroeconomic development, because it would signal a further collapse in commodity prices. It would also mean that Treasuries outperform by a wider margin.

If this ratio breaks support, look out below. I'm not entirely sure that it will because the Fed's about to turn on the money printers again in September. If anything, look for support of this formation to be tested.

Tracking Junk and Quality (Sector ETF: HYG/LQD)

Over the past couple of weeks, we've seen bears get served a cold dish after an initial triumph coming into the month of August. But throughout the selloff, I noted how credit spreads largely remained stable, but I think I found an exception.

This chart looks at the ratio between junk bonds (HYG) and investment-grade corporate debt (LQD). In a risk-on environment, you want to see this ratio rising and HYG outperforming LQD. If conditions begin deteriorating, then the inverse happens and the ratio drops.

The ratio is pressing down on this trendline now. A break below here would signal some deterioration of market conditions on behalf of capital markets, but it doesn't necessarily mean a downtrend would be established.

Editor's Take:

Liquidity in the bond market translates directly over to stock markets. After all, the bond market is where the "smart money" is most engaged, and it's a significantly larger market than the stock market. Only the currency market is bigger than bonds.

Junk bonds tend to trade more like stocks with respect to volatility, but their main appeal is the higher rate of return. Don't let the word "junk" fool you—these securities are still higher up on the totem pole compared to stocks in terms of redemption in a bankruptcy.

If this ratio continues to drop over the next few weeks, look for it to find a low once the Fed starts easing again. If it continues to drop after the easing begins, then look for the Fed to become even more aggressive in their rate cuts.

The crypto market continues to teeter off the edge of a cliff. This week, we're back to looking at Ethereum, which remains at a pivotal point technically. Simply put, if bulls don't show up in the next couple of weeks, we could be heading into a brutal fall period. I think they will, however.

Prices continue to trade in a neutral zone between $2,600-$2,900. Unless prices can start closing back above this zone, there are going to be issues in terms of restoring the bull trend. Since March, prices have been making lower-lows and lower-highs, which means a technical downtrend.

Bulls need to rely on the possibility of a false-breakdown from the descending price channel, which is a continuation pattern. Prices are hanging around the lower trendline of the formation, and if it gets back in the pattern, leaves the door open for an eventually resolution higher. But first thing's first—let's see if it can reclaim $2,900.

Legal Disclosures:

This communication is provided for information purposes only.

This communication has been prepared based upon information, including market prices, data and other information, from sources believed to be reliable, but Benzinga does not warrant its completeness or accuracy except with respect to any disclosures relative to Benzinga and/or its affiliates and an analyst’s involvement with any company (or security, other financial product or other asset class) that may be the subject of this communication. Any opinions and estimates constitute our judgment as of the date of this material and are subject to change without notice. Past performance is not indicative of future results. This communication is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Benzinga does not provide individually tailored investment advice. Any opinions and recommendations herein do not take into account individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. You must make your own independent decisions regarding any securities, financial instruments or strategies mentioned or related to the information herein. Periodic updates may be provided on companies, issuers or industries based on specific developments or announcements, market conditions or any other publicly available information. However, Benzinga may be restricted from updating information contained in this communication for regulatory or other reasons. Clients should contact analysts and execute transactions through a Benzinga subsidiary or affiliate in their home jurisdiction unless governing law permits otherwise.

This communication may not be redistributed or retransmitted, in whole or in part, or in any form or manner, without the express written consent of Benzinga. Any unauthorized use or disclosure is prohibited. Receipt and review of this information constitutes your agreement not to redistribute or retransmit the contents and information contained in this communication without first obtaining express permission from an authorized officer of Benzinga. Copyright 2022 Benzinga. All rights reserved.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.