Your Exclusive Benzinga Insider Report

(DO NOT FORWARD)

By analyst Gianni Di Poce

Volume 3.37

Market Overview (Member Only)

- Stocks surged off a higher-low, with the Nasdaq and tech leading the way. The index closed up 5.95%, while the S&P rose 4.02%, and the Dow Jones Industrial Average was up 2.60%.

- The Dollar looks like it's being sacrificed on the altar of global growth, as the ECB just cut rates and the Fed is set to cut this week.

- Gold hit a new all-time high, and crypto looks to be coming back to life.

- I think real estate is set to continue its major comeback going into next year.

Stocks I Like

- Telephone & Data Systems (TDS) – 27% Return Potential

What's Happening

- Telephone and Data Systems (TDS) is a telecom company based in the United States.

- The company made $5.16 billion in revenue in 2023, but still lost $500 million on the year.

- TDS has a reasonable valuation. Its Price-to-Sales is just 0.50 and its EV to EBITDA is at 11.46. Its Book Value is 35.77 too—lower than its share price.

- At a technical level, TDS is retesting former-resistance-turned-support of a saucer formation. If this holds, it could turn into a higher-low and reinforce the bull trend.

Why It's Happening

- TDS deployed 28,000 marketable fiber addresses in the first quarter of 2024. It expanded its total service addresses by 12% year-over-year, reaching a total service address of 1.7 million. The ongoing expansion will consolidate the market power of TDS in the telco industry, which is conducive to its future growth.

- TDS’s CEO Leroy Carlson remains optimistic of the company’s revenue growth: "TDS Telecom reported another quarter of notable growth in revenue and profitability as a result of its broadband investments."

- In Q2, TDS remained focused on balancing subscriber growth with financial discipline and reported solid ARPU growth, good expense discipline, and improved profitability—all combining to generate higher free cash flow.

- Operating income of TDS rose to $51 million from $26 million in the year-ago quarter.

- Total operating expenses stood at $1.2 billion, down 6% from the prior-year quarter's levels. This underscores management’s continued effort to cut costs and raise net margins.

- TDS has a free quarterly cash flow of $182 million.

- Analyst Ratings:

- JP Morgan: Overweight

- Morgan Stanley: Equal-weight

- Citi: Buy

My Action Plan (27% Return Potential)

- I am bullish on TDS above $19.00-$20.00. My upside target is $30.00-$31.00.

- WK Kellogg (KLG) – 25% Return Potential

What's Happening

- WK Kellogg (KLG) is a food production company with operations around the world.

- The company brought in $2.76 billion in revenue during 2023, along with $110 million in earnings.

- In terms of valuation, KLG is on-sale. Its P/E is at 12.8, its Price-to-Sales is at 0.57, and its EV to EBITDA is at 7.67.

- From a technical standpoint, KLG is attempting a breakout from resistance of a rounding bottom pattern. If successful, it could go on to retest its former highs.

Why It's Happening

- The cereal business is taking the Kellogg legacy to greater heights, with a new sustainable business strategy designed to address the broader systemic challenges in the global food system. Called Feeding Happiness, the new business strategy provides a framework for WK Kellogg Co to measure its impact on both people and the planet.

- Full-year guidance from the company suggests a mid-single-digit EBITDA increase in 2024, despite roughly zero projected sales growth.

- Standalone Adjusted EBITDA increased 50% compared to the previous year as the company continued to recover from a 2021 fire at its plant in Memphis and a labor strike the same year.

- The cereal maker flipped to a net profit of $15 million against a steep $152 million loss one year prior. This shows that the company is well on track on its return to profitability, making a nice turnaround story for the start of a mega bullish trend.

- WK Kellogg's ability to deliver strong results despite price challenges is reflective not just of its strong brands and winning culture but its focus on sustainability and purpose.

- Shares currently trade at nearly 14x this year's expected adjusted earnings per share. That's a multiple that still suggests a discount to larger, more diversified companies like General Mills and Campbells. This is an attractive valuation to start accumulating Kellogg’s stocks.

- Analyst Ratings:

- JP Morgan: Neutral

- Stifel: Hold

- Barclays: Underweight

My Action Plan (25% Return Potential)

- I am bullish on KLGabove $15.50-$16.00. My upside target is $23.00-$24.00.

- Philip Morris (PM) – 36% Return Potential

What's Happening

- Philip Morris (PM) is a blue-chip tobacco company.

- The company collected $35.17 billion in revenue in 2023, along with $7.81 billion in earnings.

- PM's valuation is solid. Its P/E is at 22.56, its Price-to-Sales is at 5.43, and its EV to EBITDA is at 16.41.

- From a charting perspective, PM continues to rise within the ascending channel, which is bullish. It looks good as long as it stays there.

Why It's Happening

- Philip Morris stock has been surging as the company has been more successful at pivoting to smoke-free products than peers like Altria and British American Tobacco. In fact, roughly 40% of Philip Morris’ revenue now comes from next-gen products like Zyn nicotine pouches and Iqos heat-not-burn devices.

- There are a couple of notable takeaways from the earnings release, including Zyn’s 50% growth in the U.S. market, 50% growth outside the U.S. market, and the fact that Zyn is entering new markets, which will help spur longer-term growth. This is a key product that appears to be increasingly in demand—to the point where Philip Morris International had trouble supplying all the demand it was seeing in the United States.

- Stan Druckenmiller’s hedge fund, Duquesne Capital, bought nearly 900,000 shares in Philip Morris, worth roughly $110 million. It also bought call options in the stock, indicating even more bullishness on the tobacco asset.

- PM trades at a dividend yield of 4.4%, which is well above the S&P 500 average dividend yield of 1.3%. Poised for strong EPS growth, Philip Morris should be able to grow its dividend payouts at a consistent rate over the next five to 10 years and outperform the market.

- Growth from its smoke-free categories was impressive as organic revenue rose 18% and gross profit was up 22%. As smoke-free products make up more of the business, it should drive increased revenue growth in the next few years.

- PM has a free quarterly cash flow of $4.26 billion.

- Analyst Ratings:

- UBS: Sell

- Barclays: Overweight

- Stifel: Buy

My Action Plan (36% Return Potential)

- I am bullish on PMabove $110.00-$111.00. My upside target is $172.00-$174.00.

Market-Moving Catalysts for the Week Ahead

Buckle Up for the Rate Cuts

Well, it's finally here. The Fed is set to start easing and begin its rate cuts this week. Following last week's tame inflation report, the probability of a 50-basis point rate cut dropped notably, and now traders are favoring a 25-basis point rate cut only.

I'm glad to see this. Admittedly, I was concerned that a 50-basis point rate cut would be construed as a panicky move on behalf of the central bank. In fact, when the Fed began easing in the past by slashing rates half a percent, it typically led to notable market slides. Ideally, we avoid a similar fate this time around.

The FOMC rate decision will be followed by a press conference from Fed Chair Powell. The concern now from a narrative standpoint has shifted from inflation over to economic growth. I would argue the Fed probably could have started cutting a couple meetings ago, but clearly, the economy has been able to handle higher rates.

Bulled Up on Real Estate

One sector that I think will continue to greatly benefit from rate cuts is real estate. The sector was in the doldrums for much of the year, but it staged a very impressive comeback over the past couple months.

Once again, the performance of various REITs (real estate investment trusts) shows how the market tends to discount future events. Mortgage rates have fallen to their lows of the year, and I expect this trend to continue going into 2025 as well.

In fact, this will probably turn into a major tailwind for residential real estate transactions, and even provide some much-needed relief on the commercial real estate front too. I'll be watching housing starts and permitting data this week, but I think the data will lag what's actually happening in the sector for quite some time.

What More Liquidity means

When it comes to rate cuts, many people get caught up in the money-printing portion of it. Yes, the Fed will be adding back to the M2 money supply, but there's another key component to monetary easing that must be considered: liquidity.

We track liquidity periodically in this report by looking at credit spreads. Interestingly, we've seen spreads narrow ever since the market's bottom in October 2022. And now, we're heading back into rate cut season, so I expect them to narrow even further.

This drastically reduces the probability of a market crash. The market only collapses when credit spreads blow out and liquidity evaporates. It's how you get those "no bid" or gap down types of days. So, if the market does encounter any selling in this falling rate environment, I would look for it to be very slow and drawn out—so long as credit spreads remain narrow.

Eyes on Commodities

Commodities have been the gift that keeps on giving for the central bank. After soaring into the early part of 2022, many commodity markets like grains, and most importantly, crude oil, have been in bearish trends.

However, I suspect that those days are coming to an end. There are still significant geopolitical tensions, and the Fed did their job by raising rates to combat inflation. The question now is how commodities will react once the money printers turn back on.

Crude oil is especially the key—everything is basically downstream from this commodity. It's more than what dictates what you pay when you fill up your gas tank. Crude oil is used in medicine, fertilizers, plastics, apparel, and more. It really is the ultimate driver of inflation expectations. I'm looking for a low of significance in crude oil in the coming months.

Sector & Industry Strength (Member Only)

Big improvements in the sector performance rankings las week, with technology (XLK) seeing a major rebound, and climbing three spots back into fourth place. This was a critical development that markets needed to help the bulls regain some momentum near-term.

The big concern is still that utilities (XLU) are the top-performer year-to-date. This is not a risk-on signal, although it is probably being driven by the prospect of lower rates on the horizon. It's also not a bad sign to see energy (XLE) as the worst sector.

Real estate (XLRE) continues to improve, and the spread between consumer discretionary (XLY) and consumer staples (XLP) continues to narrow. At some point, I would want to see XLY overtake XLP in the rankings.

| 1 week | 3 Weeks | 13 Weeks | 26 Weeks |

| Technology | Real Estate | Real Estate | Utilities |

Editor's Note:

Seeing technology return as the one-week leader gives some hope for bulls.

Stock-Bond Ratio Update (Sector ETF: SPY/TLT)

Time to check back in on the market's classical "risk-on" versus "risk-off" indicator—the ratio between stocks (SPY) and long-term Treasuries (TLT). As a quick reminder, when SPY outperforms TLT, it's risk-on, but when TLT outperforms SPY, it's risk-off.

Over the past few years, this ratio has been in a very clean uptrend in favor of stocks over bonds. For all of 2023, and most of this year, the ratio rose within an ascending channel, but it just recently broke below the lower trendline.

This signals that the rate of ascent in this ratio is no longer in effect. This comes at a time where the Fed is about to be cutting rates too. Recession concerns are rising, so if TLT accelerates in its outperformance against SPY, it could signal some major woes ahead for the market and broader economy.

Opportunity in Telecom? (Sector ETF: XTL/SPY)

I've been digging around and looking for a new sector story, and I think there's a compelling one developing in the telecom department (XTL). It's been a sector down in the doldrums in recent years, but I think it could be part of the next chapter in the artificial intelligence saga.

For the past couple years, much of what we've heard about artificial intelligence was related to semiconductor chips. But there's another layer to it—the data centers, and how to connect them you need fiber optic cables, which fall under the domain of telecom companies.

The chart below shows the ratio between telecom (XTL) and the S&P 500 (SPY). It's been in a clear downtrend, but I'm seeing a broadening bottom formation here. If it clears resistance, we could see a new period of outperformance by telecom over the indices. Lower interest rates should help this sector too.

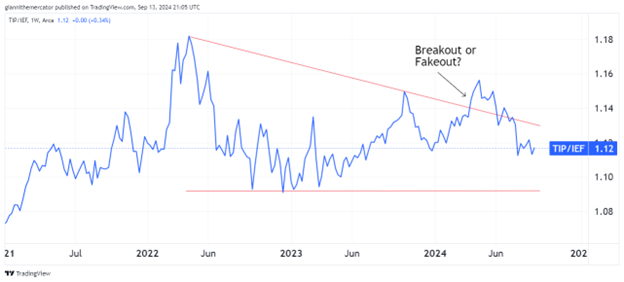

Don't Sleep on Inflation Just Yet (Sector ETF: TIP/IEF)

After last week's latest economic reports, the consensus surrounding inflation is that the Fed has won—the concern has shifted over to the growth front. However, if we look at what the bond market is signaling, I think that this declaration of victory is premature.

This chart looks at the ratio between Treasury Inflation Protected Securities (TIP) and 7-10 Year Treasuries (IEF). The logic behind this relationship is straightforward—when TIP outperforms IEF, inflationary concerns are rising, but when IEF outperforms TIP, inflationary concerns are under control.

Despite the data signaling that inflation is temporarily tamed, I see this ratio as having built a massive descending triangle base within a new uptrend. That is, I think the victory over inflation is only temporary, and with money printing around the corner again, we could be singing a much different tune by this time next year.

Editor's Take:

The secular macroeconomic trend of deflation is over. Markets had to grapple with this force for over twenty years. Between 2000 and 2010, when stocks barely did anything, there were two stock market crashes in this time. And between 2010 and 2020, commodities were in a bear market.

But the Covid crash of 2020 changed something psychologically amongst the public. It's as if people expect prices to rise into the future. And even though prices aren't rising as much as they were a couple years ago, they're not coming down. Wages have a lot of catching up to do.

With money printing around the corner, and M2 already starting to rise, I think the Fed is playing a very dangerous game cutting interest rates before seeing annual inflation rates below their 2% annual "price stability" objective. It may threaten their independence down the line.

Some interesting price action transpired in the crypto space over the past couple of weeks. Whenever I share charts here, it's in the cash market, but both Bitcoin and Ethereum have futures markets too, which gives them a level of institutionalization that other cryptocurrencies don't have.

On Friday, September 6, Ethereum's futures market took out its August 5 low. But we didn't see this unfold in Ethereum's cash market, Bitcoin's cash market, or even Bitcoin's futures market. We saw some positive price action in Bitcoin after its secondary higher-low too, which is the first step in the reestablishment of a bull trend.

When it comes to Bitcoin, there's key technical resistance in the $63,000-$65,000 zone. If that clears to the upside, momentum could start accelerating notably. Historically, Bitcoin has done well in weak Dollar, low rate, and improving liquidity environments. We have all of that right now.

Legal Disclosures:

This communication is provided for information purposes only.

This communication has been prepared based upon information, including market prices, data and other information, from sources believed to be reliable, but Benzinga does not warrant its completeness or accuracy except with respect to any disclosures relative to Benzinga and/or its affiliates and an analyst’s involvement with any company (or security, other financial product or other asset class) that may be the subject of this communication. Any opinions and estimates constitute our judgment as of the date of this material and are subject to change without notice. Past performance is not indicative of future results. This communication is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Benzinga does not provide individually tailored investment advice. Any opinions and recommendations herein do not take into account individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. You must make your own independent decisions regarding any securities, financial instruments or strategies mentioned or related to the information herein. Periodic updates may be provided on companies, issuers or industries based on specific developments or announcements, market conditions or any other publicly available information. However, Benzinga may be restricted from updating information contained in this communication for regulatory or other reasons. Clients should contact analysts and execute transactions through a Benzinga subsidiary or affiliate in their home jurisdiction unless governing law permits otherwise.

This communication may not be redistributed or retransmitted, in whole or in part, or in any form or manner, without the express written consent of Benzinga. Any unauthorized use or disclosure is prohibited. Receipt and review of this information constitutes your agreement not to redistribute or retransmit the contents and information contained in this communication without first obtaining express permission from an authorized officer of Benzinga. Copyright 2022 Benzinga. All rights reserved.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.