Your Exclusive Benzinga Insider Report

Market Overview (Member Only)

- Stocks were down last week but finished well of the lows. The Dow Jones Industrial Average was down the most, as it dropped 0.60%. The S&P 500 and Nasdaq were also lower, finishing down 0.48% and 0.51, respectively.

- The Santa Claus Rally period is over, and stocks struggled save for Friday's strong rally – this could signal a turning point for stocks here.

- I'm still keen on tech, and specifically semiconductors, reemerging as a market leader in the coming weeks and months.

- Markets will be closed on Thursday, January 9 in observance of former President Jimmy Carter's funeral.

Stocks I Like

Urban Outfitters URBN (+36% Return Potential)

What's Happening

- Urban Outfitters (URBN) is a leading global lifestyle retailer, specializing in a range of products including clothing, accessories, home decor, and beauty items. It also owns brands like Anthropologie and Free People.

- In 2023, the company reported revenues of $4.4 billion, with a net profit of $452 million.

- URBN’s valuation reflects its strong presence in the retail and fashion sectors. With solid revenue growth, its Price-to-Sales ratio is 2.1, its P/E ratio is 14.6, and its EV to EBITDA is 10.5.

- From a technical standpoint, URBN flagging within a bull flag pattern after exploding higher in November. This could lead to another leg higher in prices in the coming months.

Why It's Happening

- Urban Outfitters’ apparel rental service, Nuuly, has seen a staggering 51% increase in active subscribers year-over-year. This growth not only enhances URBN’s revenue streams but also taps into the rising trend of sustainable fashion.

- The wholesale segment of URBN also contributed positively with a 3% increase in revenue. This diversification helps stabilize earnings during periods of retail softness and provides additional channels for growth, making URBN a more resilient investment option.

- URBN is committed to long-term growth through strategic expansions and innovations across its brands. Plans for new store openings and enhancements in online shopping experiences are set to capture additional market share and cater to evolving consumer preferences, reinforcing its position as a leader in lifestyle retailing.

- Despite rising SG&A expenses, URBN has managed to improve its gross profit margins through effective cost management strategies. The gross profit rate increased by 106 basis points to 34.4%, driven by higher initial merchandise markups and reduced in-bound transportation costs. This focus on profitability will likely enhance shareholder value moving forward.

- Analysts predict that URBN’s EPS will continue to grow, with estimates suggesting an increase to $0.87 per share in the upcoming quarter—a year-over-year rise of over 26%. Such forecasts indicate strong operational performance and suggest that the company is well-positioned to meet or exceed these expectations.

- Urban Outfitters (URBN) reported a robust 8% increase in total sales for Q1 2025, reaching a record $1.2 billion.

Analyst Ratings:

- Wells Fargo: Equal-Weight

- Morgan Stanley: Equal-Weight

- Barclays: Overweight

My Action Plan (36% Return Potential)

- I am bullish on URBN above $47.00-$48.00. My upside target is $78.00-$80.00.

EQT Corp EQT (+38% Return Potential)

What's Happening

- EQT Corporation (EQT) is a leading natural gas production company, specializing in the exploration, development, and production of unconventional natural gas resources, primarily in the Appalachian Basin, catering to the energy sector’s demand for cleaner fuels.

- In 2023, the company reported revenues of $9.8 billion, with a net profit of $1.7 billion.

- EQT’s valuation reflects its strong position in the energy and natural gas sectors. With consistent revenue growth, its Price-to-Sales ratio is 2.4, its P/E ratio is 9.1, and its EV to EBITDA is 6.3.

- From a technical perspective, EQT just retested former resistance-turned-support of a saucer formation and completed a higher-low. Now we look to see if it can make a new high and reinforce the bull trend.

Why It's Happening

- EQT Corp recently completed the sale of its non-operated natural gas assets in Northeast Pennsylvania for approximately $1.25 billion. This strategic move allows EQT to focus on its core operations in the Appalachian Basin, which is crucial for enhancing operational efficiency and sustainability.

- The proceeds from the asset sale will be used to pay down existing borrowings under EQT’s revolving credit facility. This reduction in debt not only strengthens EQT’s balance sheet but also lowers interest expenses, which can significantly improve future cash flow.

- Following the asset sale, Mizuho upgraded EQT’s stock rating from Neutral to Outperform. This reflects growing confidence in the company’s operational strategy and financial health. Analyst endorsements can drive investor interest and lead to stock price appreciation as market participants react positively to improved outlooks.

- EQT has extended its share repurchase program through 2026, with approximately $1.4 billion remaining in authorization. This commitment to returning capital to shareholders signals management’s confidence in the company’s future prospects and can provide a floor for the stock price as shares are bought back from the market.

- Under CEO Toby Rice’s leadership, EQT is focused on becoming a globally competitive player in the natural gas sector through strategic acquisitions and operational consolidation. This long-term vision not only enhances investor confidence but also sets a foundation for sustained growth and value creation in an evolving energy landscape.

- In its most recent earnings report, EQT posted an EPS of $0.12, exceeding analysts’ expectations of $0.06.

Analyst Ratings:

- Mizuho: Outperform

- Citigroup: Buy

- Bernstein: Market Perform

My Action Plan (38% Return Potential)

- I am bullish on EQT above $40.00-$41.00. My upside target is $65.00-$67.00.

Bill.com BILL (+47% Return Potential)

What's Happening

- Bill.com (BILL) is a leading cloud-based software platform that automates accounts payable and accounts receivable processes, serving small to medium-sized businesses across various industries to streamline financial workflows and improve cash flow management.

- In 2023, the company reported revenues of $1.1 billion, with a net loss of $89 million.

- Bill.com’s valuation reflects its strong position in the fintech sector. With rapid revenue growth, its Price-to-Sales ratio is 25.3, its P/E ratio is not applicable due to the company being unprofitable, and its EV to EBITDA is 120.7.

- From a charting standpoint, BILL is forming its flag after recently establishing a bull flag formation. This means more gains could be on the table here.

Why It's Happening

- With nearly 500,000 businesses using BILL’s platform, there’s still significant room for growth in the vast SMB market. As more businesses recognize the need for efficient financial operations, BILL is well-positioned to capture a larger market share, potentially driving substantial stock appreciation.

- BILL continues to invest in innovation, expanding its platform capabilities and enhancing its AI-powered features. This focus on technological advancement could lead to new revenue streams and increased customer retention, ultimately benefiting shareholders.

- The company repurchased approximately 3.7 million shares of common stock for $200 million in Q1. This significant buyback demonstrates management’s confidence in BILL’s long-term prospects and commitment to delivering shareholder value, which could positively impact the stock price.

- BILL recently hired Mary Kay Bowman as Executive Vice President of Payments and Financial Services, and Bobbie Grafeld as the new Chief People Officer. These strategic hires bring valuable industry experience and expertise, potentially driving innovation and growth in key areas of the business.

- BILL reported impressive first-quarter results, with total revenue reaching $358.5 million, an 18% year-over-year increase.

- Core revenue, consisting of subscription and transaction fees, grew by 19% year-over-year to $314.9 million.

Analyst Ratings:

- Keybanc: Overweight

- Mizuho: Neutral

- Baird: Neutral

My Action Plan (47% Return Potential)

- I am bullish on BILL above $72.00-$73.00. My upside target is $130.00-$135.00.

Market-Moving Catalysts for the Week Ahead

Fed, Labor, and Silence

Normally, we would be back to a regular trading schedule this week, but markets will be closed on Thursday, January 9 in observance of former President Jimmy Carter's funeral. So, we won't have our first full week of trading until the week of the 13th, and then the following week, it's another shortened week due to markets being closed for Martin Luther King Jr. Day.

But that doesn't mean there aren't important data reports next week. In fact, I'm watching for the FOMC minutes most closely, which are set to be released on Wednesday. The same day, we have the ADP employment report too.

On Friday, there are the employment reports, which could easily be a market moving event too. Much of the economic resiliency we've seen over the past couple of years has been due to the labor market, although it's worth noting that any deterioration in that department could lead to the Fed becoming more dovish again.

Taking Stock of 2024 – Trends into 2025

2024 was one for the record book as the S&P 500 rallied just over 23% on the year. The top-performing sector was communications, and it's amazing to consider how well the market did with tech not dominating its peers.

The quantum computing sector roared to life and now it looks like artificial intelligence may have a competitor in terms of a theme within tech. I think this will turn out to be very bullish for semiconductors, and I'm looking for this to become a market leader again in 2025.

Tech isn't going anywhere – and it's almost as if the future we were promised decades ago may finally be coming to fruition. I'm not saying there won't be consequences to the future, but all I know is that I want to own equities during this transition period.

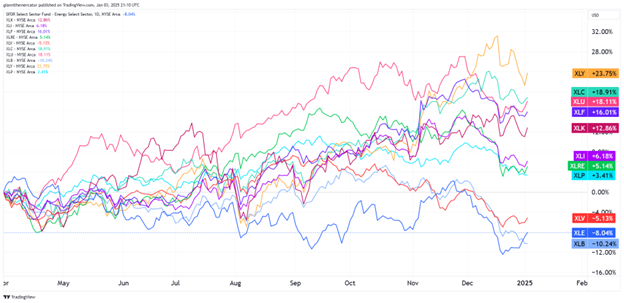

Sector & Industry Strength (Member Only)

It was another bullish week for stocks and it looks like we're coming out of a higher-low too. I'm starting to see another wave of leadership from growth sectors like tech (Ticker: XLK), consumer discretionary (Ticker: XLY), and communications (Ticker: XLC).

If we look back at the leaders from Q2 2024, we continue to see the bullish sectors at the top of the pack. So long as this is the case, there is little-to-no reason to be bearish this market. If that changes, then so will our outlook.

Energy (Ticker: XLE) is still the worst performer going back to Q2 2024, but with the recent rise in crude oil, it will be interesting to see if this continues. Inflation doesn't seem to be a real threat at the moment, based on the current sector leadership rankings.

| 1 week | 3 Weeks | 13 Weeks | 26 Weeks |

| Energy | Utilities | Consumer Discretionary | Consumer Discretionary |

Editor's Note: Energy gathering momentum – can it last?

Are Bonds Due for a Surprise in 2025? – Sector ETF SPY TLT

It was another tough year for bond market investors as the reality of inflation becoming a secular problem is understood. The performance of bonds relative to stocks has especially been dismal, and it's hurt the traditional 60/40 stock-bond allocation.

So, as we begin 2025, let's check in on the market's classical risk-on/risk-off indicator – the relationship between stocks (SPY) and long-term Treasuries (TLT). As a quick reminder, when SPY outperforms TLT (ratio rises), it's risk-on. When TLT outperforms SPY (ratio falls), it's risk-off.

We still see this ratio rising within the ascending channel, but don't be surprised if we see it go sideways or even correct at some point throughout the year. The Fed is still lowering rates and if we see any equity market volatility, look for this ratio to start dropping beforehand.

Tech's Posturing for 2025 – Sector ETF XLK SPY

Now that we have the final sector scorecard of 2024, it's interesting to note how the tech sector (XLK), which is the largest and most important for the equity market overall, finished right in the middle of the pack compared to its peers.

That's right – much of what was accomplished in the stock market last year was not a direct result of tech stocks outperforming by a wide margin like we've seen in past bull markets. It's one of the big reasons why I have optimism for stocks this year.

The ascending triangle formation on the ratio between XLK and SPY portends to a continuation of the secular bull trend of technology dominating the stock market. We still need to close above the upper horizontal trendline of the pattern, but as long as this ratio isn't breaking down this year, I'm still a bull.

Liquidity Treading Water – Sector ETF LQD IEI

It's a new year, which means it's high-time to revisit why a ratio from the bond market is always included in these reports. While stocks have a tendency to capture all of the headlines, it's imperative to remember that bonds are a much larger market where institutions tend to play.

If we assume that institutions are a bit more in the "know" about what's going on economically, then it makes sense to pay close attention to what's happening in the bond market. So, we're starting off this year looking at credit spreads between investment grade corporate debt (LQD) and 3-7 Year Treasuries (IEI).

Simply put, when liquidity conditions are strong, or LQD is outperforming IEI and the ratio is rising, the odds of a market crash are slim. But when IEI outperforms LQD and the ratio is dropping, downside risks are elevated.

Editor's Take:

At the last Fed meeting, Fed Chair Powell came out as much more hawkish than the market expected. He dialed back expectations for rate cuts in 2025, which has left the market on edge as of late.

You better believe that the Fed is watching these credit spreads closely. I'm keen on a bottom forming here and eventually, the ratio breaking out from the rounding bottom formation and climbing to new highs.

But a couple things need to happen for that to materialize. First, the Fed needs to cut more than expected now. This leads to the second point – I think it's important we see energy prices come down to increase that probability. I'm still not ruling that out in 2025.

Cryptocurrency

Bitcoin’s technical indicators still favor the bulls, with prices consolidating nicely within the rectangle formation. These are continuation patterns that imply that the underlying bull trend can continue.

This pattern suggests Bitcoin could hit between $125,000 and $130,000. This consolidation now serves to quell some of the previous concerns surrounding the rapid pace of the rally. Typically, a market that surges quickly can also plummet rapidly, so it's good that bulls can catch their breath here.

As long as Bitcoin holds above the key support levels of $78,000 to $80,000, there’s no immediate need for the rally to pause. It looks like a higher-low is complete here, and remember, the longer this consolidation goes on, the higher prices can go.

Legal Disclosures:

This communication is provided for information purposes only.

This communication has been prepared based upon information, including market prices, data and other information, from sources believed to be reliable, but Benzinga does not warrant its completeness or accuracy except with respect to any disclosures relative to Benzinga and/or its affiliates and an analyst’s involvement with any company (or security, other financial product or other asset class) that may be the subject of this communication. Any opinions and estimates constitute our judgment as of the date of this material and are subject to change without notice. Past performance is not indicative of future results. This communication is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Benzinga does not provide individually tailored investment advice. Any opinions and recommendations herein do not take into account individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. You must make your own independent decisions regarding any securities, financial instruments or strategies mentioned or related to the information herein. Periodic updates may be provided on companies, issuers or industries based on specific developments or announcements, market conditions or any other publicly available information. However, Benzinga may be restricted from updating information contained in this communication for regulatory or other reasons. Clients should contact analysts and execute transactions through a Benzinga subsidiary or affiliate in their home jurisdiction unless governing law permits otherwise.

This communication may not be redistributed or retransmitted, in whole or in part, or in any form or manner, without the express written consent of Benzinga. Any unauthorized use or disclosure is prohibited. Receipt and review of this information constitutes your agreement not to redistribute or retransmit the contents and information contained in this communication without first obtaining express permission from an authorized officer of Benzinga. Copyright 2022 Benzinga. All rights reserved.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.