Your Exclusive Benzinga Insider Report

(DO NOT FORWARD)

By analyst Gianni Di Poce

Volume 4.02

Market Overview (Member Only)

- The turbulence in stocks continued last week, with the Nasdaq leading the selloff lower. It finished down 2.34%, while the S&P 500 and Dow Jones Industrial Average followed, finishing 1.94% and 1.86% lower, respectively.

- Energy is trying to make its move as the Fed seems to be losing the plot on inflation. This week's inflation data will be key for the market mood.

- Not all hope is lost for bulls here as semiconductors are holding up well.

- It's the first full calendar week for trading this year, as elements of fear start to creep into the picture. I still see this as a "buy the dip" opportunity.

Stocks I Like

Applied Optoelectronics AAOI (+89% Return Potential)

What's Happening

- Applied Optoelectronics (AAOI) is a leading provider of optical components and solutions, specializing in high-performance products for the broadband, telecommunications, and data center markets.

- In 2023, the company reported revenues of $217.6 million but reported a loss of $56 million.

- Due to its loss, the valuation picture is a bit tricky. Its Price-to-Sales is at 6.34 and its Book Value is 4.29. There are a lot of expectations around this stock.

- From a technical perspective, AAOI is consolidating nicely within a symmetrical triangle pattern. This leaves the door open for another leg higher in this name.

Why It's Happening

- AAOI recently announced 400G and 800G multimode fiber designs in collaboration with Credo Technology Group. These new technologies aim to reduce network power dissipation and cost of ownership while ensuring robust performance. Such innovations could give AAOI a competitive edge in the rapidly evolving fiber optics market.

- AAOI is set to join the broad-market Russell 3000 Index. This inclusion enhances the company’s visibility among institutional investors and could lead to increased demand for AAOI shares, potentially driving up the stock price.

- AAOI has filed a patent infringement lawsuit against Accelight Technologies (ATI). This proactive approach to protecting its intellectual property rights demonstrates the company’s commitment to maintaining its competitive advantage and could potentially lead to monetary damages or licensing agreements.

- Raymond James raised its price target for AAOI from $17.00 to $39.00. This significant increase in price target reflects growing analyst confidence in the company’s prospects. As more analysts recognize AAOI’s potential, it could attract additional investor interest and drive stock appreciation.

- AAOI reported Q3 2024 revenue of $65.2 million, up from $62.5 million in Q3 2023 and $43.3 million in Q2 2024

- The company expects Q4 2024 revenue between $94-104 million, representing a significant 40% quarter-over-quarter growth at the midpoint.

- AAOI has a short interest over 20% – leaving the door open for a squeeze higher.

Analyst Ratings:

- Raymond James: Outperform

- Northland Capital Markets: Outperform

- Rosenblatt: Buy

My Action Plan (89% Return Potential)

- I am bullish on AAOI above $28.50-$29.00. My upside target is $60.00-$65.00.

Xometry XMTR (+100% Return Potential)

What's Happening

- Xometry (XMTR) is a leading online marketplace for custom manufacturing services, connecting customers with a network of suppliers to deliver on-demand, high-quality parts across various industries.

- Over the past year, XMTR brought in $141.7 million in revenue but still lost $10.2 million on the year.

- Xometry is an expensive stock with its Price-to-Sales at 3.89 and its Book Value at just 6.36.

- At a technical level, XMTR is retesting a former-resistance-turned-support zone. If it holds, it will reinforce the bull trend.

Why It's Happening

- Xometry’s international expansion offers significant growth potential5. With operations organized into U.S. and International segments, the company is well-positioned to tap into global markets. As Xometry scales its international presence, it could unlock new revenue streams and diversify its business, potentially leading to stock appreciation.

- The company’s AI-enabled manufacturing platform positions it at the forefront of industry innovation. Xometry’s unique offering caters to a diverse range of clients, including engineers, product designers, and business owners. This technological edge provides a competitive advantage that could drive long-term growth and market leadership.

- Xometry’s focus on high-growth sectors like CNC Machining, Injection Molding, and 3D Printing positions it well for future demand. These manufacturing processes are critical in industries ranging from aerospace to medical devices. As demand for advanced manufacturing solutions grows, Xometry’s specialized offerings could drive increased market share and revenue growth, potentially boosting its stock performance.

- The company’s gross margin is projected to improve significantly, reaching 34.1% by 2026. This margin expansion indicates increasing operational efficiency and pricing power. As Xometry optimizes its business model and achieves economies of scale, the improved profitability could lead to higher valuations and stock price growth.

- RBC Capital raised Xometry’s price target to $40 from $27. This significant increase reflects growing confidence in the company’s potential. As part of RBC’s 2025 outlook for the software sector, this upgrade suggests Xometry is well-positioned to benefit from multiple catalysts in the coming year, including stabilized spending trends and opportunities driven by generative AI.

- Xometry’s revenue growth rate of 19.15% over the last 3 months outperforms its peers in the Industrials sector.

- XMTR has a short interest around 19%, making it a solid candidate for an additional squeeze higher.

Analyst Ratings:

- RBC Capital: Sector Perform

- JP Morgan: Overweight

- JMP Securities: Market Outperform

My Action Plan (100% Return Potential)

- I am bullish on XMTR above $34.00-$35.00. My upside target is $68.00-$70.00.

Sanmina SANM (+29% Return Potential)

What's Happening

- Sanmina (SANM) is a global leader in providing integrated manufacturing solutions, specializing in the design, development, and production of complex electronics and other advanced products for a wide range of industries, including communications, healthcare, and industrial sectors.

- Over the past year, SANM had $2.02 billion in revenue along with $61.38 million in earnings.

- For a tech stock, SANM has a solid valuation. Its P/E is at 19.67, its Price-to-Sales is at 0.57, and its EV to EBITDA is at 8.18.

- From a charting viewpoint, SANM is digesting its gains within a descending triangle. It would look very strong if it cleared the upper trendline of the formation.

Why It's Happening

- Sanmina operates in various sectors, including industrial, medical, defense, automotive, communications networks, and cloud. This diversification helps mitigate risks associated with any single industry and positions the company to capitalize on growth opportunities across multiple markets, potentially leading to more stable and consistent financial performance.

- Sanmina holds a 49.9% interest in Sanmina SCI India Private Limited, a joint venture with Reliance Strategic Business Ventures Limited. This partnership could provide access to the fast-growing Indian market and potentially drive future revenue growth and market expansion.

- Sanmina’s involvement in key industries such as medical, defense, and cloud computing positions the company to benefit from long-term growth trends in these sectors. As these industries continue to expand, Sanmina’s stock could see significant appreciation.

- Recent SEC filings show multiple insider transactions, including share sales by company insiders. While share sales can sometimes be viewed negatively, they can also indicate that insiders believe the stock is fairly valued, potentially signaling a good entry point for new investors.

- Sanmina provided an optimistic outlook for Q1 2025, projecting revenue between $1.925 billion and $2.025 billion, with non-GAAP EPS ranging from $1.30 to $1.40.

- The company reported an EPS of $1.43, surpassing analyst estimates of $1.37.

Analyst Ratings:

- Craig-Hallum: Hold

- Sidoti & Co: Buy

My Action Plan (29% Return Potential)

- I am bullish on SANM above $67.00-$68.00. My upside target is $100.00-$102.00.

Market-Moving Catalysts for the Week Ahead

First It Was Jobs, Now It's Inflation

Last week's jobs report was the last thing that Fed doves wanted to see. It was a classic case of "good news is bad new" when it comes to the prospect of further rate cuts. Remember, the point of easing is to stimulate the economy, but if the jobs market is stronger than expected, why cut?

The unemployment rate is now sitting at 4.1%, which is pretty strong. More jobs were created than expected in December too. Now this week, the market's attention turns towards inflation data. Doves are absolutely banking on a lower-than-expected reading this week after rate cut timing has been pushed back even further than before.

A lot of inflation going forward depends on crude oil, which is pressing up on resistance. Don't forget that earnings season kicks off this week as well, and if anything is going to place momentum back in the camp of the bulls, it could be stronger than expected results on that front.

Stocks Need Help from Bonds

Given enough time, rising bond yields can cause challenges for stocks. When bond yields increase, bond investments may eventually grow to become more attractive compared to stocks. Keep in mind that bonds are considered lower-risk that stocks, and such a shift could lead investors to reallocate their portfolios from equities to bonds en masse, reducing demand for stocks and potentially driving down stock prices. To be clear – I don't think we're close to this moment just yet.

Bigger picture, higher yields mean increased borrowing costs for companies, which can squeeze corporate profit margins, particularly for those with significant debt. This can lead to reduced earnings forecasts and troublesome stock valuations.

Inflation remains the conundrum here. The data suggests it's contained and crude oil prices aren't ripping higher – so, what gives? It would seem the culprit is rising risk premium. Where is the risk coming from? Probably the federal budget situation in Washington. But of course, financial markets think ahead. If we grow our way out of this fiscal debacle, it means higher inflation down the line.

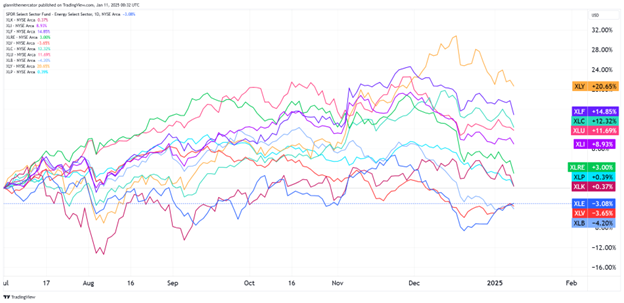

Sector & Industry Strength (Member Only)

As we saw another round of stock market volatility this past week, I deemed it appropriate to tighten up the time horizon we've been using to compare the sector performance rankings to see if bears have any real ground to stand on.

Even with the shorter time horizon, we still see the risk-off sectors like consumer staples (Ticker: XLP), healthcare (Ticker: XLV), and energy (Ticker: XLE) closer to the bottom of the list. The only defensive sector doing well is utilities (Ticker: XLU).

On the contrary, I'm seeing a lot of evidence that most of the flows within the stock market are bullish. Yes, energy has been the top-performing sector in the past month, but that is often late cycle behavior. Bulls need to see tech (Ticker: XLK) wake up here, and if it does, look out above.

| 1 week | 3 Weeks | 13 Weeks | 26 Weeks |

| Energy | Energy | Consumer Discretionary | Consumer Discretionary |

Editor's Note: Energy creeping up into the sector leadership rankings – this could mean a low in stocks is near.

The Battle Between Bonds and Commodities – Sector ETF: DBC TLT

There seems to be a lot of confusion right now surrounding the inflation narrative, which is why I've taken care over the past couple of weeks to dive deep into some key intermarket ratios. This week, we're looking at commodities (DBC) against long-term Treasuries (TLT).

This ratio bottomed back in early-September, just before the Fed began rate cuts. Remember, when the Fed is lowering rates, they're printing money. Since then, money started flowing into hard assets at the expense of bonds.

But I'm not ruling out the possibility that this multi-month trend won't last much longer. In fact, I'm still eyeing the rounding top formation on this ratio, and if it breaks below support, we could see an epic rebound in bond prices. If it doesn't unfold, we could have some issues with inflation sooner than later again.

Finally – The Bullish Signal I Needed – Sector ETF: SMH QQQ

Frequent readers of the Insider Report know that this is not a doom and gloom publication, but it's also not a perma-bull publication either. A few weeks ago, I warned that the ratio between semiconductors (SMH) and the Nasdaq 100 (QQQ) was flashing warning signs. Let's take an updated look at this key ratio.

The thinking here is pretty straightforward – chips are critical infrastructure for so many tech companies. If they're not outperforming relative to tech, it warns that demand from tech is weak and is a risk-off signal.

It looks like we had a false-breakdown from the rounding top formation on this ratio, and as the saying goes, "From false moves, come fast moves." In terms of the trend, it's a higher-low too, which means another run for chips is in the works. In fact, the bull market is banking on it.

Tracking Money Flows in Bonds – Sector ETF: BIL TLT

The bond market environment we've seen since the Fed started cutting rates back in September has been anything but ordinary. Typically, when the central banks cut rates, we see longer-term yields following shorter-term yields lower.

This time, the opposite has happened. In fact, it's been one of the worst-performing periods for long-term bonds after the Fed has started to cut rates in history. We're seeing this play out clearly in the ratio between short-term T-Bills (BIL) and long-term Treasury Bonds (TLT).

The ratio here has been rising since just before the Fed began cutting rates in mid-September 2024. In other words, we've seen losses in long-term bonds pile up, while there have been solid gains on the short-end of the bond market.

Editor's Take:

From a technical standpoint, the situation in this ratio is very compelling right now. First and foremost – we address the trend, which is upward. We know that we've all traded and invested through a historic bond market crash over the past few years, even though there's been some relief since October 2023.

But with money flowing into short-term bonds at the expense of long-term bonds, we need to be careful about this ratio hitting a new high. It broke out from the symmetrical triangle formation, which implies that a continuation of the uptrend is underway.

So, bond bulls still need to play defense in the long-term Treasury market. This highlights the issues I raised before with rate cuts – higher inflation expectations in the long-run, which is a real headwind for bond prices.

Cryptocurrency

Looking at Solana this week, the price action is presenting a compelling technical setup that suggests further upside potential. The recent strong bounce off the crucial support level around $182.55 has reinforced this zone’s significance as a key floor for SOL prices.

The bullish uptrend remains firmly intact, as evidenced by the series of higher lows and higher highs within the channel. More importantly, the recent pullback found eager buyers at the lower trendline of this formation, demonstrating that bulls are still in control of the broader trend.

Looking ahead, if this momentum continues, we could see SOL challenge the recent swing highs around the $220-230 zone.

The measured move from the current ascending channel projects potential targets even higher, possibly extending toward the $250 area. However, traders should keep a close eye on that critical $182.55 support – any decisive break below this level would warrant a reassessment of the bullish thesis. For now, though, the technical structure favors the upside, especially with the strong bounce off important support and the intact bullish channel formation.

Legal Disclosures:

This communication is provided for information purposes only.

This communication has been prepared based upon information, including market prices, data and other information, from sources believed to be reliable, but Benzinga does not warrant its completeness or accuracy except with respect to any disclosures relative to Benzinga and/or its affiliates and an analyst’s involvement with any company (or security, other financial product or other asset class) that may be the subject of this communication. Any opinions and estimates constitute our judgment as of the date of this material and are subject to change without notice. Past performance is not indicative of future results. This communication is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Benzinga does not provide individually tailored investment advice. Any opinions and recommendations herein do not take into account individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. You must make your own independent decisions regarding any securities, financial instruments or strategies mentioned or related to the information herein. Periodic updates may be provided on companies, issuers or industries based on specific developments or announcements, market conditions or any other publicly available information. However, Benzinga may be restricted from updating information contained in this communication for regulatory or other reasons. Clients should contact analysts and execute transactions through a Benzinga subsidiary or affiliate in their home jurisdiction unless governing law permits otherwise.

This communication may not be redistributed or retransmitted, in whole or in part, or in any form or manner, without the express written consent of Benzinga. Any unauthorized use or disclosure is prohibited. Receipt and review of this information constitutes your agreement not to redistribute or retransmit the contents and information contained in this communication without first obtaining express permission from an authorized officer of Benzinga. Copyright 2022 Benzinga. All rights reserved.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.