Ireland abandoned its sovereign currency when it joined the Euro. Effectively, it became like a US state—think Louisiana—within the EMU. This means it has little domestic policy space to use monetary or fiscal policy to deal with crisis. If we go back to 2005, Ireland's government had the second lowest ratio of debt to GDP (national output or income) in the EU-15, with only Luxemberg having a lower debt ratio. The government paid an interest rate similar to that paid by the French and German governments; it had a strong AAA rating on its debt. In fact, it was running a huge government surplus of 2.5% of GDP (similar to that run by the Clinton administration in the late 1990s in the US).

Then the global financial crisis hit. The Irish banks faced default on their external debts. The UK and the Netherlands came to the rescue of their creditors who were holding uninsured liabilities of Irish banks. The Irish government assumed much of the debt of its banks. And now the English and the Dutch are demanding reimbursement for their bail-outs.

So now the Irish government is facing default. Its government deficit ratio reached about 12.5% of GDP this spring, and it paid 6 percentage points higher to borrow than Germany did (on March 22 the spread on two year bonds hit a record 835 basis points—8.35 percentage points—over the rate on equivalent German debt).

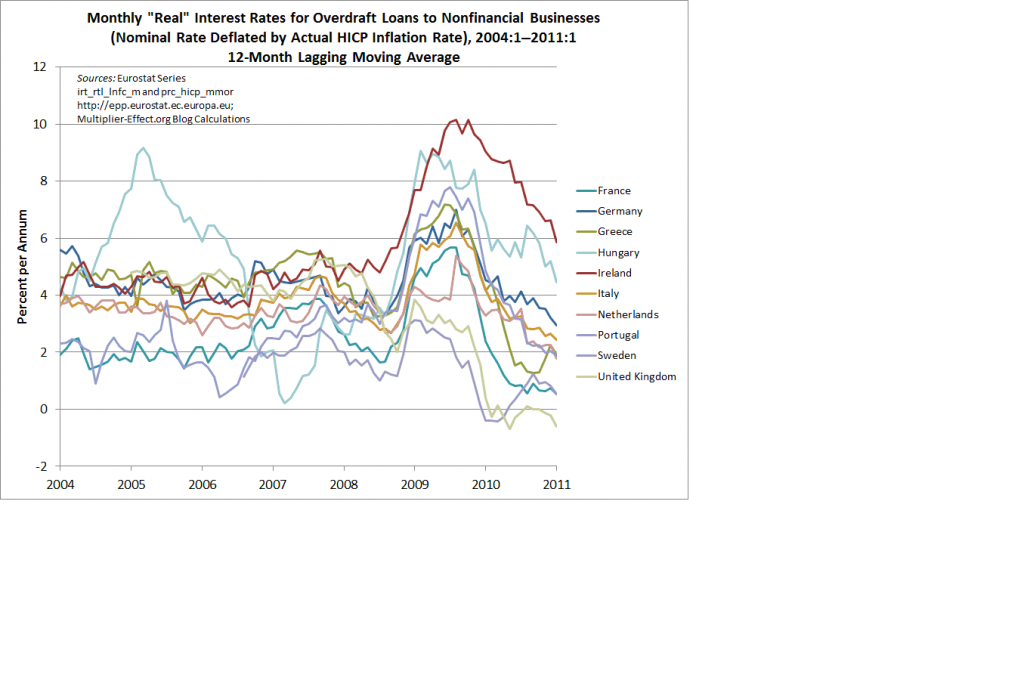

The following graph shows inflation-adjusted interest rates paid on government debt in a number of countries. While I am not a big fan of constructing a “real interest rate” by subtracting inflation from nominal rates, doing so in this particular case does no damage. What is important is the relation between the interest rate and the growth rate—so if we deduct inflation from both we can compare the “real” interest rate against the “real” growth rate. It is fairly obvious that Ireland's current interest rate sets a standard that is far too high—both relative to its neighbors and relative to a growth rate that it can conceivably attain.

(source: http://www.multiplier-effect.org/)

There is a fundamental relation between economic growth and ability to service debt. To be safe, a non-sovereign government should not pay an interest rate that significantly exceeds its growth rate. (A country that pegs its currency, operates a currency board, adopts a dollar standard, or adopts a foreign currency is by my definition “non-sovereign”.) If we compare Ireland today to the situation of Germany, because the Irish government pays almost 6 percentage points more, it needs to grow 6 percentage points faster than Germany does. While this is a rough rule of thumb and there is some leeway, the prospects for Ireland to grow that much faster than Germany approach a zero probability.

Indeed, the conventional way to generate government revenues needed to service debt is to cut government spending and raise taxes—which will only hurt Irish growth. Further, what Ireland needs is to increase the flow of euros in its favour through its foreign balance, i.e. by reducing imports and increasing exports to the EMU. The conventional prescription is slow domestic growth to reduce imports and enhance international competitiveness. This, too, further reduces domestic growth even further below the interest rate paid on government debt.

However, with the exception of the BRICs (Brazil, Russia, India and China) recent economic data across the globe have not been good. That makes it harder for Ireland to export its way out of debt—which is the least painful path. I do not see alternatives means of earning the needed euros that are without substantial suffering. Yet, many other EU nations are in a similar situation (even if some are less dire)—and will be competing with Ireland's rush to the bottom. This is not a battle Ireland is likely to win.

Unfortunately, slow growth of the economy usually means slow growth of tax revenue. It is fairly easy to imagine a scenario in which domestic austerity actually makes the budget deficit worse, which raises interest rates on government debt. A vicious cycle can be created, with debt service blowing up as growth continues to slow and interest rates rise with credit ratings agencies downgrading government debt.

For a sovereign currency nation the interest rate is a policy variable and has no impact on solvency. Government can keep rates low (it sets the overnight rate directly, and can if it desires issue only short maturity bonds near to that rate) and pays interest through “keystrokes” by crediting bank accounts with interest. It can never run out of keystrokes so will never fail to make interest payments unless it chooses to do so for noneconomic reasons.

For Ireland, however, this is a very serious problem. It does not have a sovereign currency. It cannot control its borrowing rates, which are set in markets. Nominal interest rates should not exceed nominal GDP growth rates. For Ireland to service debt at 10% interest rates, it will need Chinese growth rates. That seems unlikely.

So how should the government deal with its debt? I would encourage the government to unwind its guarantees of bank debt. If this cannot be done, then Ireland must have a bail out and debt relief provided by the ECB or the EMU through some other entity. That is actually in the interest of the EMU since much of the bank debt guaranteed by Ireland's government is held externally by EU banks. The last resort alternative is default on debt and possible expulsion from the EMU. That will be painful but there isn't anything Ireland can be expected to do without support from the EU—except for default.

The Irish government should pursue debt relief on all fronts. Voters should resist austerity programs. If all else fails, they should demand either default or withdrawal from the EMU (in practice these probably amount to the same thing).

L. Randall Wray is a Professor of Economics, University of Missouri—Kansas City. A student of Hyman Minsky, his research focuses on monetary and fiscal policy as well as unemployment and job creation. He writes a weekly column for Benzinga every Tuesday. He also blogs at New Economic Perspectives, and is a BrainTruster at New Deal 2.0. He is a senior scholar at the Levy Economics Institute, and has been a visiting professor at the University of Rome (La Sapienza), UNAM (Mexico City), University of Paris (South), and the University of Bologna (Italy).

(source: http://www.multiplier-effect.org/)

There is a fundamental relation between economic growth and ability to service debt. To be safe, a non-sovereign government should not pay an interest rate that significantly exceeds its growth rate. (A country that pegs its currency, operates a currency board, adopts a dollar standard, or adopts a foreign currency is by my definition “non-sovereign”.) If we compare Ireland today to the situation of Germany, because the Irish government pays almost 6 percentage points more, it needs to grow 6 percentage points faster than Germany does. While this is a rough rule of thumb and there is some leeway, the prospects for Ireland to grow that much faster than Germany approach a zero probability.

Indeed, the conventional way to generate government revenues needed to service debt is to cut government spending and raise taxes—which will only hurt Irish growth. Further, what Ireland needs is to increase the flow of euros in its favour through its foreign balance, i.e. by reducing imports and increasing exports to the EMU. The conventional prescription is slow domestic growth to reduce imports and enhance international competitiveness. This, too, further reduces domestic growth even further below the interest rate paid on government debt.

However, with the exception of the BRICs (Brazil, Russia, India and China) recent economic data across the globe have not been good. That makes it harder for Ireland to export its way out of debt—which is the least painful path. I do not see alternatives means of earning the needed euros that are without substantial suffering. Yet, many other EU nations are in a similar situation (even if some are less dire)—and will be competing with Ireland's rush to the bottom. This is not a battle Ireland is likely to win.

Unfortunately, slow growth of the economy usually means slow growth of tax revenue. It is fairly easy to imagine a scenario in which domestic austerity actually makes the budget deficit worse, which raises interest rates on government debt. A vicious cycle can be created, with debt service blowing up as growth continues to slow and interest rates rise with credit ratings agencies downgrading government debt.

For a sovereign currency nation the interest rate is a policy variable and has no impact on solvency. Government can keep rates low (it sets the overnight rate directly, and can if it desires issue only short maturity bonds near to that rate) and pays interest through “keystrokes” by crediting bank accounts with interest. It can never run out of keystrokes so will never fail to make interest payments unless it chooses to do so for noneconomic reasons.

For Ireland, however, this is a very serious problem. It does not have a sovereign currency. It cannot control its borrowing rates, which are set in markets. Nominal interest rates should not exceed nominal GDP growth rates. For Ireland to service debt at 10% interest rates, it will need Chinese growth rates. That seems unlikely.

So how should the government deal with its debt? I would encourage the government to unwind its guarantees of bank debt. If this cannot be done, then Ireland must have a bail out and debt relief provided by the ECB or the EMU through some other entity. That is actually in the interest of the EMU since much of the bank debt guaranteed by Ireland's government is held externally by EU banks. The last resort alternative is default on debt and possible expulsion from the EMU. That will be painful but there isn't anything Ireland can be expected to do without support from the EU—except for default.

The Irish government should pursue debt relief on all fronts. Voters should resist austerity programs. If all else fails, they should demand either default or withdrawal from the EMU (in practice these probably amount to the same thing).

L. Randall Wray is a Professor of Economics, University of Missouri—Kansas City. A student of Hyman Minsky, his research focuses on monetary and fiscal policy as well as unemployment and job creation. He writes a weekly column for Benzinga every Tuesday. He also blogs at New Economic Perspectives, and is a BrainTruster at New Deal 2.0. He is a senior scholar at the Levy Economics Institute, and has been a visiting professor at the University of Rome (La Sapienza), UNAM (Mexico City), University of Paris (South), and the University of Bologna (Italy).

Market News and Data brought to you by Benzinga APIs

(source: http://www.multiplier-effect.org/)

There is a fundamental relation between economic growth and ability to service debt. To be safe, a non-sovereign government should not pay an interest rate that significantly exceeds its growth rate. (A country that pegs its currency, operates a currency board, adopts a dollar standard, or adopts a foreign currency is by my definition “non-sovereign”.) If we compare Ireland today to the situation of Germany, because the Irish government pays almost 6 percentage points more, it needs to grow 6 percentage points faster than Germany does. While this is a rough rule of thumb and there is some leeway, the prospects for Ireland to grow that much faster than Germany approach a zero probability.

Indeed, the conventional way to generate government revenues needed to service debt is to cut government spending and raise taxes—which will only hurt Irish growth. Further, what Ireland needs is to increase the flow of euros in its favour through its foreign balance, i.e. by reducing imports and increasing exports to the EMU. The conventional prescription is slow domestic growth to reduce imports and enhance international competitiveness. This, too, further reduces domestic growth even further below the interest rate paid on government debt.

However, with the exception of the BRICs (Brazil, Russia, India and China) recent economic data across the globe have not been good. That makes it harder for Ireland to export its way out of debt—which is the least painful path. I do not see alternatives means of earning the needed euros that are without substantial suffering. Yet, many other EU nations are in a similar situation (even if some are less dire)—and will be competing with Ireland's rush to the bottom. This is not a battle Ireland is likely to win.

Unfortunately, slow growth of the economy usually means slow growth of tax revenue. It is fairly easy to imagine a scenario in which domestic austerity actually makes the budget deficit worse, which raises interest rates on government debt. A vicious cycle can be created, with debt service blowing up as growth continues to slow and interest rates rise with credit ratings agencies downgrading government debt.

For a sovereign currency nation the interest rate is a policy variable and has no impact on solvency. Government can keep rates low (it sets the overnight rate directly, and can if it desires issue only short maturity bonds near to that rate) and pays interest through “keystrokes” by crediting bank accounts with interest. It can never run out of keystrokes so will never fail to make interest payments unless it chooses to do so for noneconomic reasons.

For Ireland, however, this is a very serious problem. It does not have a sovereign currency. It cannot control its borrowing rates, which are set in markets. Nominal interest rates should not exceed nominal GDP growth rates. For Ireland to service debt at 10% interest rates, it will need Chinese growth rates. That seems unlikely.

So how should the government deal with its debt? I would encourage the government to unwind its guarantees of bank debt. If this cannot be done, then Ireland must have a bail out and debt relief provided by the ECB or the EMU through some other entity. That is actually in the interest of the EMU since much of the bank debt guaranteed by Ireland's government is held externally by EU banks. The last resort alternative is default on debt and possible expulsion from the EMU. That will be painful but there isn't anything Ireland can be expected to do without support from the EU—except for default.

The Irish government should pursue debt relief on all fronts. Voters should resist austerity programs. If all else fails, they should demand either default or withdrawal from the EMU (in practice these probably amount to the same thing).

L. Randall Wray is a Professor of Economics, University of Missouri—Kansas City. A student of Hyman Minsky, his research focuses on monetary and fiscal policy as well as unemployment and job creation. He writes a weekly column for Benzinga every Tuesday. He also blogs at New Economic Perspectives, and is a BrainTruster at New Deal 2.0. He is a senior scholar at the Levy Economics Institute, and has been a visiting professor at the University of Rome (La Sapienza), UNAM (Mexico City), University of Paris (South), and the University of Bologna (Italy).© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Benzinga simplifies the market for smarter investing

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.

Join Now: Free!

Already a member?Sign in